Coal-based power is vital for meeting the country’s energy needs, given that it accounts for 60 per cent of the total installed capacity base and 80 per cent of the total generation. A significant amount of coal reserves, cheap generation costs, and technological maturity have been driving the growth of coal-based power in India. In recent years, the private sector has played a major role in capacity addition in the segment. As of end-December 2015, coal-based capacity stood at 173 GW, with the private and state sectors accounting for shares of 36 per cent and 35 per cent respectively. The central sector contributed the remaining (29 per cent).

Power Line presents an account of the key trends, developments and outlook for the coal-based power segment…

Capacity addition

Between 2010-11 and 2014-15, the installed coal-based capacity increased at a compound annual growth rate of 15 per cent to reach around 165 GW. During 2014-15, around 19.3 GW was added compared to 15.1 GW in 2013-14.

In 2015-16, over 10,000 MW of coal-based units were commissioned between April and December 2015. The key projects include NTPC’s 500 MW Vindhyachal unit-13, Damodar Valley Corporation’s 600 MW Raghunathpur unit-2, Hinduja National Power’s 520 MW Vizag unit-1, GMR’s 660 Talwandi Sabo unit-2, JP Power’s 660 MW Prayagraj (Bara) unit-1, and MB Power’s 600 MW Lalitpur unit-2.

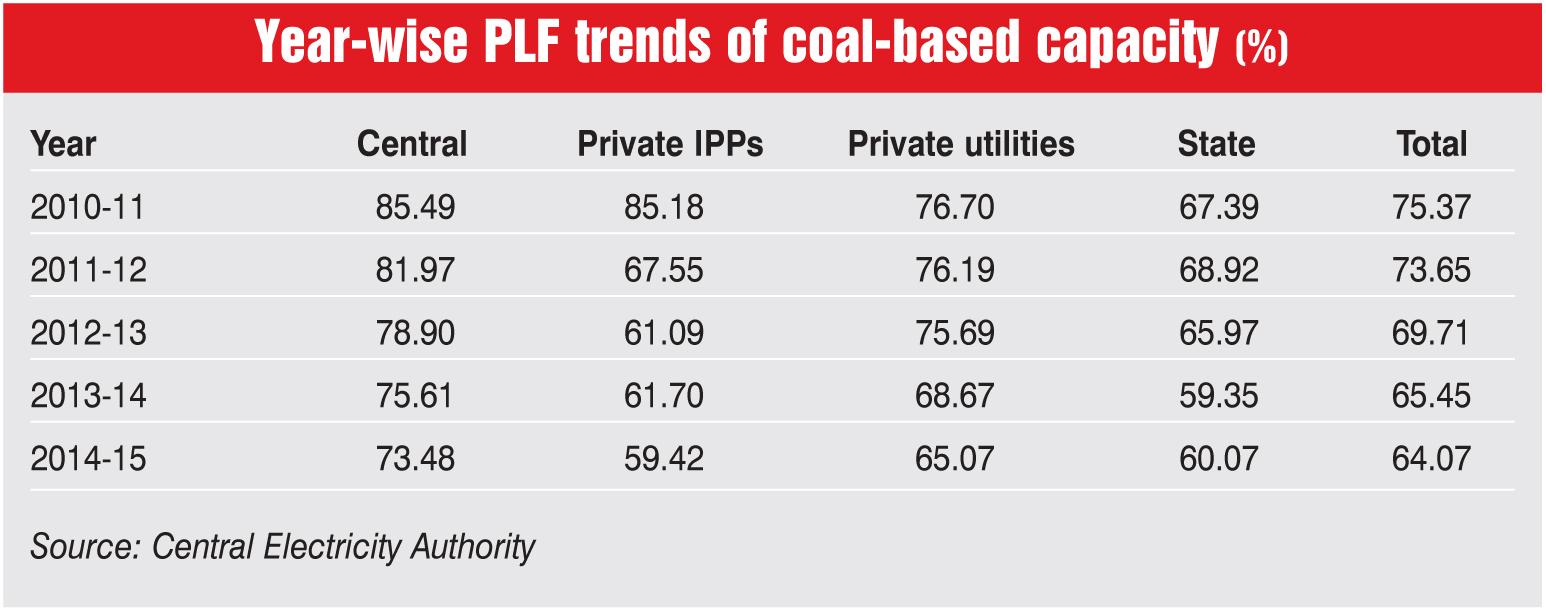

PLF trends

The average plant load factor (PLF) of coal- and lignite- based plants has been declining consistently since 2007-08, going from over 78 per cent to less than 65 per cent in 2014-15. In 2015-16, the average PLF of coal-based plants stood at 61.42 per cent while that of lignite-based plants stood at 68.83 per cent for the April-December period.

While fuel shortage has eased in the past year and a half, the backing down of generators due to low offtake by discoms is the primary reason for the PLF decline. The PLFs of private independent power producers (IPPs) have seen the maximum decline, going from over 85 per cent in 2010-11 to about 59 per cent in 2014-15.

Generation performance

In 2014-15, generation from coal-based units stood at over 800 billion units (BUs), accounting for 80 per cent of the total generation during the year. This marked an increase of 12 per cent over the 714 BUs recorded in the previous year. Between April and December 2015, the total generation from coal-based units stood at 635 BUs, up from 598 BUs in the corresponding period of the previous year.

Improvement in coal supply

Owing to the increase in Coal India Limited’s output by about 7 per cent in 2014-15 and by over 9 per cent in the April-December 2015 period, coal supply to power plants has improved. As per the Ministry of Power (MoP), the growth in domestic coal supply for power plants during 2014-15 was 10.4 per cent.

To ensure coal supply for plants lacking captive coal blocks, linkages or long-term power purchase agreements (PPAs), the Ministry of Coal (MoC) has stipulated that a separate quantity must be earmarked for the power sector.

In a bid to incentivise the efficiency of coal-based power generation, the government has approved the automatic transfer of coal linkages of old plants (more than 25 years old) to new supercritical plants. These automatic transfers are permissible only when a new plant has been set up in the state where the old plant is located and the old plant has actually been scrapped.

Aggressive bidding in captive coal block auctions

Coal-based IPPs bid aggressively in the captive coal block auctions of February-March 2015. All nine blocks on offer witnessed negative bidding as power producers relinquished their right to pass on fuel costs to consumers, and instead agreed to bear mining costs and pay the government an additional premium. The forward premiums in the two bidding rounds ranged from Rs 302 per tonne (Jitpur-Adani Power) to Rs 1,110 per tonne (Tokisud North-Essar Power). The aggressive bidding can be attributed to the bidders’ focus on ensuring fuel security for power projects rather than profitability.

Revised bidding guidelines for UMPPs

Several key developments have taken place on the ultra mega power project (UMPP) front. The union government released draft standard bidding documents (SBDs) for domestic coal-based UMPPs in August 2015, and for imported coal-based UMPPs in January 2016 after the tendering process was cancelled in January 2015. A key feature of the draft guidelines is the return to the build-own-operate model of UMPP development rather than the earlier design-build-finance-operate-transfer model. The SBDs attempt to address developer concerns on the variations in imported coal costs through a provision for blending.

In a separate development, Reliance Power (RPower) pulled out of the 3,960 MW Tilaiya UMPP in Jharkhand due to land acquisition delays by the state government. It is also seeking to exit the 4,000 MW Krishnapatnam UMPP in Andhra Pradesh due to imported coal cost escalation issues. It has reportedly made an offer to the Power Finance Corporation to buy back the 3,960 MW Sasan UMPP on account of the cancellation of the associated Chhatrasal coal block by the MoC. Meanwhile, the Central Electricity Regulatory Commission (CERC) came out with a favourable order for RPower’s Sasan UMPP, allowing it to claim an increase in the electricity duty rate and energy development cess.

Revised bidding guidelines for Case I projects

The MoP issued amended guidelines for Case I power procurement on May 5, 2015 to enable utilities to use SBDs for inviting tariff-based bids for electricity supply. As per the amendments, to decentralise the decision-making process, any deviation from the SBDs for Case I power projects will have to be made by the distribution licensees with the approval of the appropriate commission instead of the central government.

Due to the change in the coal policy, wherein concessional coal is available, the contract period for long-term procurement has been changed from the current 25 years to seven years and above, up to a period of 25 years from the date of commencement of power supply with a provision for a five-year extension at the option of either party in accordance with the power supply agreement. While the lowest bidder will be selected, the amendments state that the remaining bidders will be kept in reserve.

Mergers and acquisitions continue

Some key merger and acquisition deals were announced in the coal-based segment over the past 12 months. JSW Energy entered into a binding MoU with Jaiprakash Power Ventures Limited for acquiring 100 per cent stake in its 500 MW Bina thermal power plant in Madhya Pradesh in September 2015. Meanwhile, Adani Power continues to expand inorganically by signing a share purchase agreement (SPA) with Avantha Power in March 2015 for acquiring the latter’s 600 MW coal-based plant at Korba, Chhattisgarh. However, Tata Power ended its SPA with Ideal Energy Private Limited for the acquisition of a 540 MW thermal project in Nagpur owing to the non-fulfilment of conditions.

Increase in stressed assets

Due to the lack of long-term PPAs, delays in land acquisition and other statutory clearances, and fuel supply constraints, several power projects, including coal-based ones, faced financial viability issues. According to Crisil Ratings, power projects aggregating 46,000 MW are held up due to these problems. This has put massive pressure on the banking system as loans worth about Rs 750 billion are estimated to be at risk.

Future outlook

In recent months, there have been several significant policy developments in the coal-based power segment. The union government is confident of finalising the UMPP bidding guidelines within this financial year, and of awarding three UMPPs at Banka in Bihar, Bedabahal in Odisha, and Cheyyur in Tamil Nadu by March 2016. IPPs and state utilities are also exploring new mechanisms like reverse auctions to source coal and get competitive prices, the benefits of which can be passed on to consumers.

Moreover, the amendments to the Tariff Policy, 2006 are set to have a far-reaching impact on coal-based IPPs. The revised policy has introduced the concept of renewable generation obligations, under which new coal- and lignite-based plants will be required to set up or procure renewable capacity. Investments in coal-rich Odisha, West Bengal, Jharkhand and Chhattisgarh are also being encouraged for creating employment opportunities in these states. The amendments even allow for the 100 per cent expansion of existing plants.

Overall, the outlook for the coal-based power segment looks positive, but issues regarding the lack of industrial electricity demand and the backing down of power purchase by discoms need to be resolved.