The key global trends currently shaping the power sector are an increase in the share of renewable energy sources in power generation, the use of sophisticated and energy-efficient technologies, and the rise in power demand as well as in private participation across the power value chain. The World Economic Forum (WEF) points to these trends in its recent report, “The Future of Electricity in Fast-growing Economies Attracting Investment to Provide Affordable, Accessible and Sustainable Power”, released in January 2016. The report, which is the second in the series of “Future of Electricity” reports by the WEF, outlines the need for policy intervention to achieve the three key objectives of security and accessibility, short- and medium-term affordability, and environmental sustainability in energy markets.

According to the report, fast growing economies face different challenges than matured ones. While the latter aim to obtain a sustainable mix of generation technologies, the former target to meet the growing energy demand with an increase in consumer connections to the grid and rise in per capita power consumption.

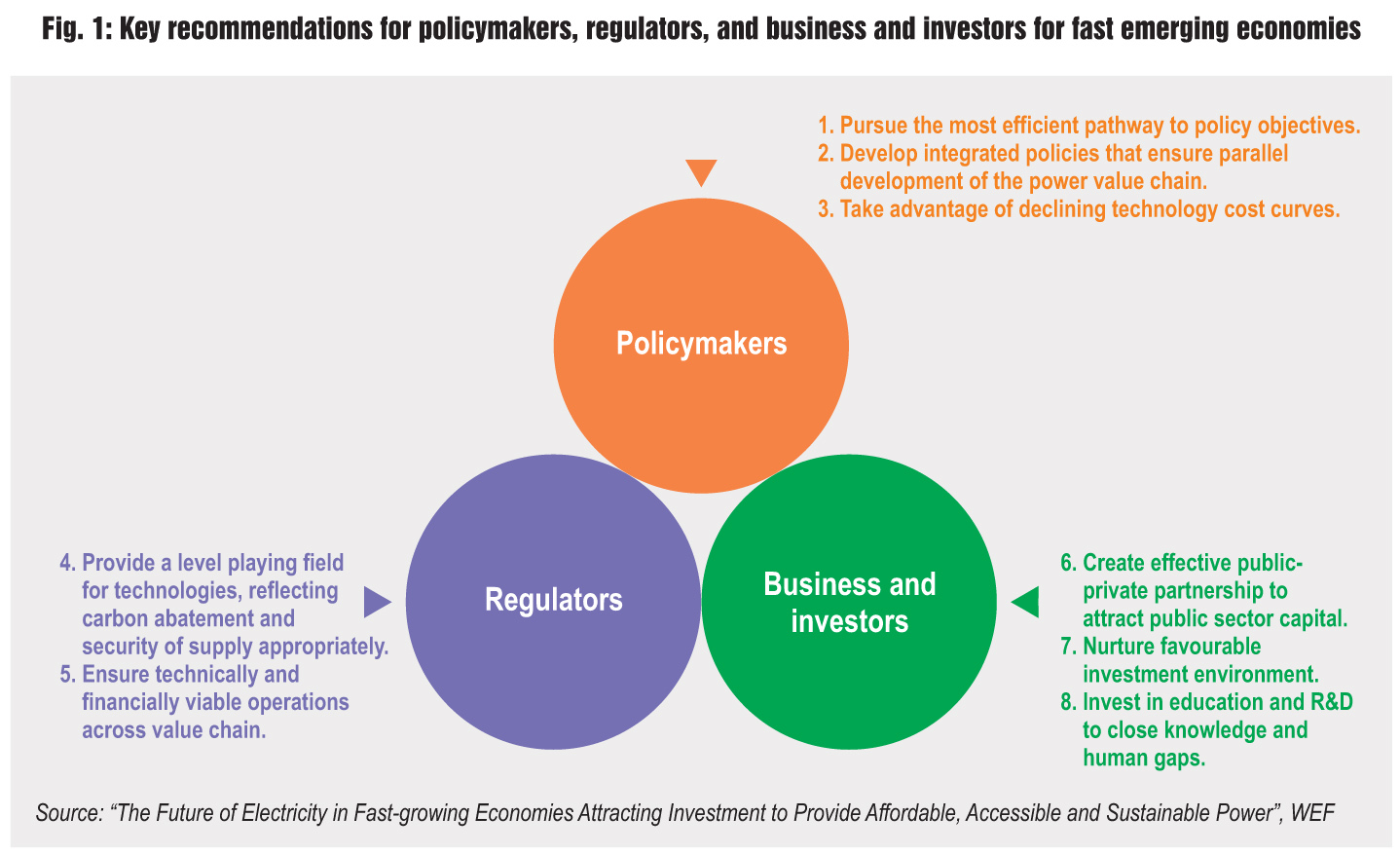

Further, the report makes recommendations for policymakers, regulators and investors, to attract investments in the electricity sector of fast-growing economies to obtain secure, sustainable and competitive power (Figure 1). A chapter in the report, Fuelling India’s Potential, contains recommendations to resolve issues in India’s distribution sector, tackle the fuel supply challenge, achieve the country’s 175 GW renewable energy target, and improve power infrastructure.

Excerpts from the “Fuelling India’s Potential” section the report…

India’s power sector is at an inflection point, given the government’s conviction that electricity is a critical enabler for economic growth. India’s government recognises the need for private investment in the power sector and is planning to adopt progressive policies on renewables and the sector overall. Alignment between federal and state government objectives is critical, as India devolves significant power to its states.

Recommendations identified in the best practices section of this report are all relevant for India, but there are also four key imperatives that India can focus on to improve the sector’s attractiveness to investors.

- India needs to fix the viability of its distribution system.

- Policymakers can help by developing and promoting a framework conducive to public-private partnerships in electricity transmission, distribution and generation. In the short-term, basics need to be fixed – for example, separate electricity infrastructure for different industries (feeder segregation), and metering systems and collection systems, all of which require strong political will to execute.

- Regulators can help by ensuring a level playing field for private players that enter the market, and working to stem non-technical losses. They can ensure transparency in overall industry governance and clear separation between policymakers and regulators. Regulators also can ensure the delivery of open access, which is the ability of large commercial and industrial customers to purchase power from an open market.

- The private players who enter the distribution market will be able to help improve the viability of the distribution network in several ways. They are most likely to introduce new technologies in the grid, such as outage management systems (OMS), distribution management systems (DMS) and demand management systems (including matching power purchase agreements to demand curves), while also helping to accelerate adoption of smart grid and meter technology. Private players can bring the capabilities to develop integrated regional or national systems that will yield substantial benefits in load and supply forecasting. They can also help establish an integrated peak power capacity to stabilize the grid and a national ultra-high voltage (UHV) network.

- India needs to address its fuel supply challenge.

- Policymakers have an important role to play by moving upstream industries towards the free market and attracting more participation from the private sector. Initiatives such as a streamlined and viable coal auction process, defined risk-reward frameworks to attract global majors with the right technologies and capabilities, and adopting free market driven pricing will all help increase supply.

- Indian regulators can also optimize and scale the model of Mine– Develop–Operate by accelerating the MDO award process, adopting single-window clearance through a coordinated approach across ministries.

- Businesses and investors have an important role to play in improving the operational efficiency of Coal India Ltd. (CIL) by streamlining processes, improving productivity and implementing more efficient managerial practices. A new long-term strategic model for CIL needs to be adopted with a better capital management and asset strategy, including potentially breaking out parts of CIL. Power infrastructure needs to be optimised with more pithead plants, which generate power from coal at the mines, and UHV lines from coastal locations.

- Private players will likely build much of the additional capacity to alleviate bottlenecks in the coal distribution system at the ports and in the railways. Building rail corridors dedicated to coal, dedicated LNG ships, regasification terminals, and dredging deeper sea berths for larger ships will also be required.

- With potential government support, private players could help build a world-class technology cell to assess and commercialize new technologies (for example underground mining), which could help attract more skilled technological talent to the industry.

- India’s plan to add 175 GW of capacity from renewables by 2022 can succeed only if the relevant stakeholders act in ways that encourage investment in this part of the sector.

- Policymakers should develop the blueprint for the country’s renewable energy capacity by 2022 and provide policy support to foster investment in solar power. They can help attract external capital by reducing borrowing costs through strengthening the state electricity boards. They can also boost the solar industry by simplifying rules and regulations of the construction of distributed solar power across many different types of infrastructure. Similarly, land acquisition regulations should be simplified to accelerate growth of wind and solar power generation.

- Regulators should enable distributed generators to feed excess power into the grid and receive payments or discounts for it. Regulators can enforce the mechanisms underlying renewable purchase obligations (RPOs) and renewable generation obligations (RGOs), while also promoting open access for wind power. Critically, they should ensure long-term tariff consistency with no retroactive changes or flip-flops.

- Investors and businesses can contribute in all areas. There are opportunities to set up large solar and wind power plants on idle land through both bilateral and auction routes, promote rooftop PV through solar leasing models supported by feed-in tariffs and tax benefits, and develop the infrastructure to support new capacity. These will require businesses to incubate new technologies (for example, for wind, higher capacity turbines, gearless generators, offshore masts, central and distributed storage technologies and wind generation forecasting tools) and launch training programmes to create the skills base required for the next wave of investment.

- Even with the huge investments in renewables, most of the electricity consumed in India over the next two decades will be generated by burning fossil fuel, and India can do much to improve the efficiency of the existing power infrastructure.

- Policymakers should develop an integrated outlook for India’s energy, including targets for fuel mix, emissions and sector progress, and set a government body to monitor progress. Tariffs and rates for fuel pricing, costs that are passed through to customers, and peak power policies and pricing should all be transparent and consistent across India’s states.

- Policymakers should continue their work on improving demand-side energy efficiency, extending efforts such as the domestic lighting initiative to include other sectors of the economy.

- Regulators should define clear guidelines for public and private sector participation and develop “single-window clearance” for large projects like Ultra Mega Power Projects (UMPP), assigning to developers only those risks that they can control.

- The private sector is best suited to define blueprints for systems that include large coal and gas plants and the coastal infrastructure to import coal and LNG.

- Businesses also play a critical role in promoting efficient new technologies, such as ultra-super critical boilers, particularly as they become more financially viable. They can also help optimise the use of the coal through coal-to-power system efficiency initiatives such as heat rate optimization, gangue reuse, washed coal and fire minimization. They will also be the training ground for the next generation of skilled workforce for the energy industry.

To conclude, there is a need for concerted efforts by the authorities, both central and state, as well as other stakeholders in the sector to encourage growth in the country’s power sector. Besides, focusing on all the elements of the power value chain, including generation, transmission and distribution, increasing private participation, and improving investment viability in the country.