There have been several positive developments in India’s power generation and transmission segments over the past year. The rising trend in power generation capacity, reforms in the fuel sector and ambitious targets for installed renewable capacity have triggered the need for additional transmission capacity and a robust infrastructure to support the increasing generation capacity and peak demand. There have also been significant developments in the transmission segment, aimed at meeting the increased generation capacity and bulk power evacuation requirements, and at enhancing the inter-regional power transfer capacity. These include the implementation of high capacity corridors, the development of green energy corridors, the installation of high voltage direct current (HVDC) lines and greater private sector participation.

In order to outline the roadmap for further transmission capacity development, the Central Electricity Authority (CEA) has recently released a perspective transmission plan for the period 2016-36, which includes projections for the transmission system based on future power demand and generation capacity addition plans. The CEA has worked out region-wise and all-India surplus-deficit scenarios for assessing transmission requirements using detailed load flow modelling of possible load growth, along with generation capacity addition scenarios. The 20-year 2016-36 perspective transmission plan is an update on the previous 2014-34 transmission plan for estimating the grid expansion and investment requirements of the transmission network.

Under the 2014-34 transmission plan, it was estimated that around 62,800 ckt. km of transmission lines, 15,000 MW of HVDC terminal capacity and 128,000 MVA of transmission capacity at the 400 kV and above levels would be required to meet the peak energy demand and increased generation capacity. The peak energy demand was estimated at 403,800 MW for the Fourteenth Plan period, 546,000 MW for the Fifteenth Plan period and 615,700 MW for 2033-34. The installed capacity was estimated at 691,122 MW at the end of the Fourteenth Plan period, 948,509 MW at the end of Fifteenth Plan and at 1,029,410 MW at the end of 2033-34.

Need for the plan

The Electricity Act, 2003 opened up the previously constrained electricity market, which was characterised by long-term power purchase agreements and the inability of discoms and consumers to choose their suppliers. Besides delicensing generation and removing controls on captive generation, the act provided non-discriminatory open access to the transmission and distribution segment. However, the participation of discoms in the bidding process is not satisfactory and results in suboptimal utilisation in some parts of the grid. Therefore, it is important to frame an optimum transmission plan, which will decide the course of transmission capacity development to support the increased energy demand and generation capacity.

Electricity demand projections

Demand assessment is an essential prerequisite for planning the generation capacity addition and associated transmission infrastructure required to meet the future power requirement of various sectors of the economy. As per the new transmission plan (2016-36), the all-India peak power demand is expected to reach 236,000 MW during the Thirteenth Plan period (ending 2021-22), 349,500 MW during the Fourteenth Plan period (ending 2026-27), 506,900 MW during the Fifteenth Plan period (ending 2031-32) and 681,900 MW during the Sixteenth Plan period (ending 2035-36), reflecting a compound annual growth rate (CAGR) of around 8 per cent for the period 2021-36.

In addition, the report has estimated peak export demand from the neighbouring South Asian Association for Regional Cooperation (SAARC) countries. The total peak load demand of these countries to be served from the Indian grid has been estimated at 237,000 MW, 352,000 MW, 511,000 MW and 686,000 MW for the Thirteenth, Fourteenth, Fifteenth and Sixteenth Plan periods respectively.

Generation capacity projections

As per the transmission plan, the generation capacity from conventional fuels will increase to 377.5 GW by the end of 2021-22. Of the 377.5 GW, around 72 per cent of capacity will be coal based, followed by hydropower (18 per cent), gas (7 per cent) and nuclear (4 per cent). Meanwhile, the aggregate generation capacity including importable generation capacity of SAARC countries is expected to reach around 750 GW.

With the Ministry of New and Renewable Energy’s ambitious target of installing 175 MW of renewable energy capacity by 2022, the fuel mix is expected to undergo a major change. As per the plan, at the end of 2026-27, around 52 per cent of the total generation capacity will be thermal followed by renewable (33 per cent), hydropower, including 24.3 GW of installed capacity from Nepal and Bhutan (12 per cent), and nuclear energy (3 per cent).

As per long-term projections, the generation capacity is expected to increase to around 1,047 GW during the Fifteenth Plan period and 1,337 GW over the Sixteenth Plan period. The projections reflect that the generation capacity will grow at a CAGR of 9.5 per cent during the period 2021-36, mainly driven by the increase in renewable energy capacity. However, due to their low plant load factor of about 20 per cent and non-availability during peak hours (6 to 9 p.m.), renewable energy projects will make a lower contribution towards meeting the overall energy demand.

Transmission capacity projections

The transmission corridor capacity requirements have been worked out based on advance estimates of peak load demand and preliminary assessments of region-wise generation addition over the next 20 years. A load generation balance analysis for 2021-22 has indicated that the northern and southern regions would be required to import power and the remaining (western, eastern, north-eastern, Bhutan and Bangladesh) regions would be in a position to export power. To cater to this requirement, a number of interregional transmission corridors have been planned. The interregional transmission capacity expected to be installed by 2021-22 is estimated at 91,250 MW. These high capacity transmission corridors are at various stages of implementation and most of these are likely to be commissioned by 2021-22. The total transmission capacity addition between 2015 and 2022 is estimated at 35,900 MW. Of this, around 19,000 MW is expected to be installed during 2017-22. The maximum addition is planned in the west-south region (76 per cent) followed by the west-north (16 per cent) and east-north (8 per cent) regions.

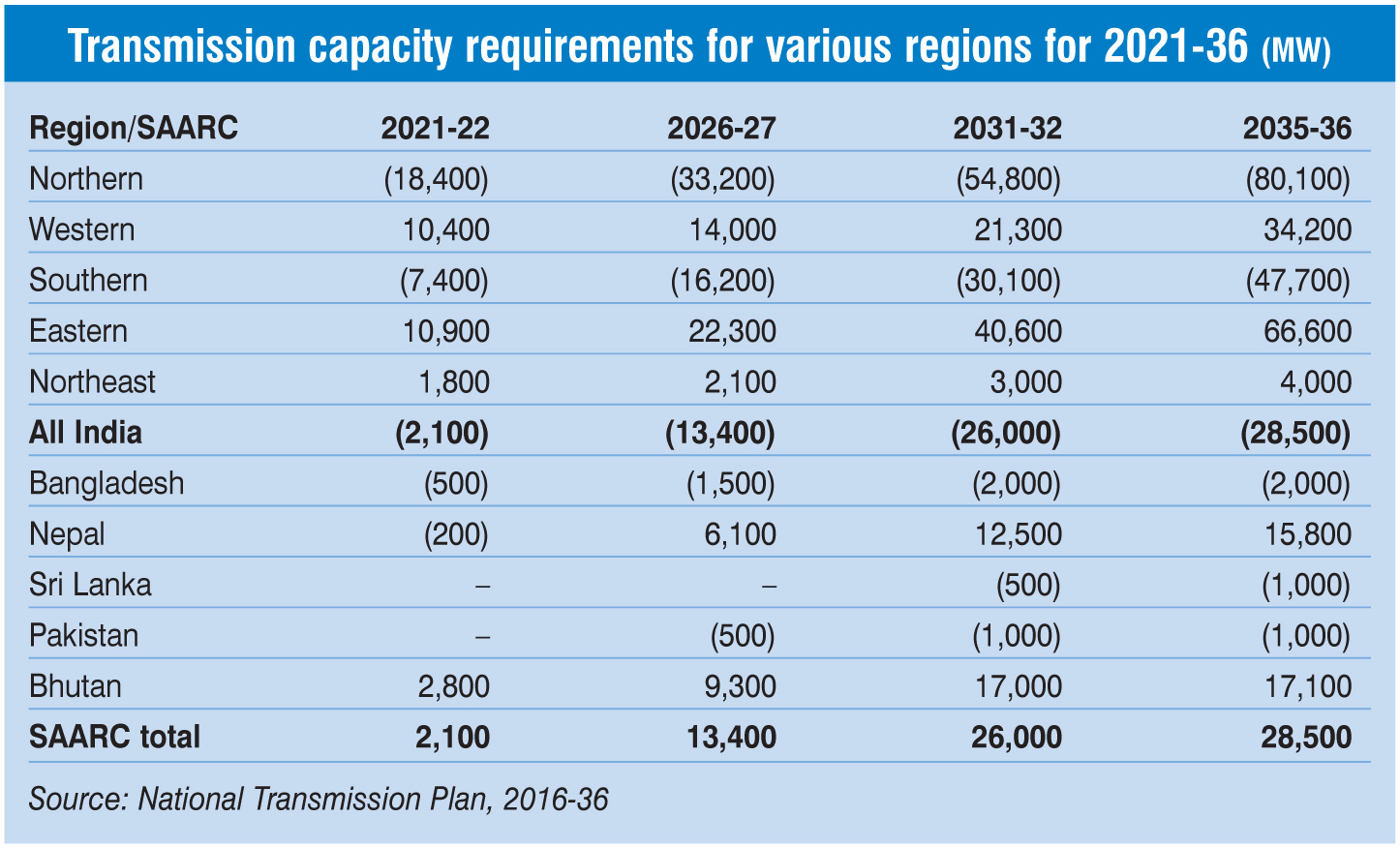

As per the long-term estimates, the total transmission capacity requirements considering export/import for various regions will increase at a CAGR of 20.5 per cent, from 2,100 MW in 2021-22 to 28,500 MW in 2035-36.

Conclusion

A region-wise analysis shows that major transmission corridors need to be set up in the northern and southern regions. To reduce the burden on the transmission system, there is a need to develop more hydro generation capacity in these regions.

With the expected increase in generation capacity driven by independent power producers, transmission systems will need further strengthening in a phased manner to meet the grid reliability criteria. Further, high capacity transmission systems will be required for the upcoming ultra mega power projects. However, transmission strengthening schemes will be taken up once the generation projects have been confirmed.

Moreover, the state transmission utilities are required to undertake planning and implementation of intra-state systems and their interconnection with the interstate transmission system as scheduled by various transmission schemes so that the planned generation reaches the target beneficiaries.

There is a need to review the existing methods and adopt a different approach to maintain the load generation balance of the grid and manage the large renewable energy capacity addition proposed for the future.