The year 2017 is turning out to be quite eventful for the renewable energy sector. First, solar power prices plummeted to Rs 3.30 per kWh in early February in the auction for developing the 750 MW Rewa solar power park in Madhya Pradesh. If this was not striking enough, on February 24, wind power prices crashed to a record low of Rs 3.46 per kWh in the country’s first-ever auction of wind power capacity. The Solar Energy Corporation of India invited bids for 1 GW of wind capacity based on the viability gap funding (VGF) mechanism.

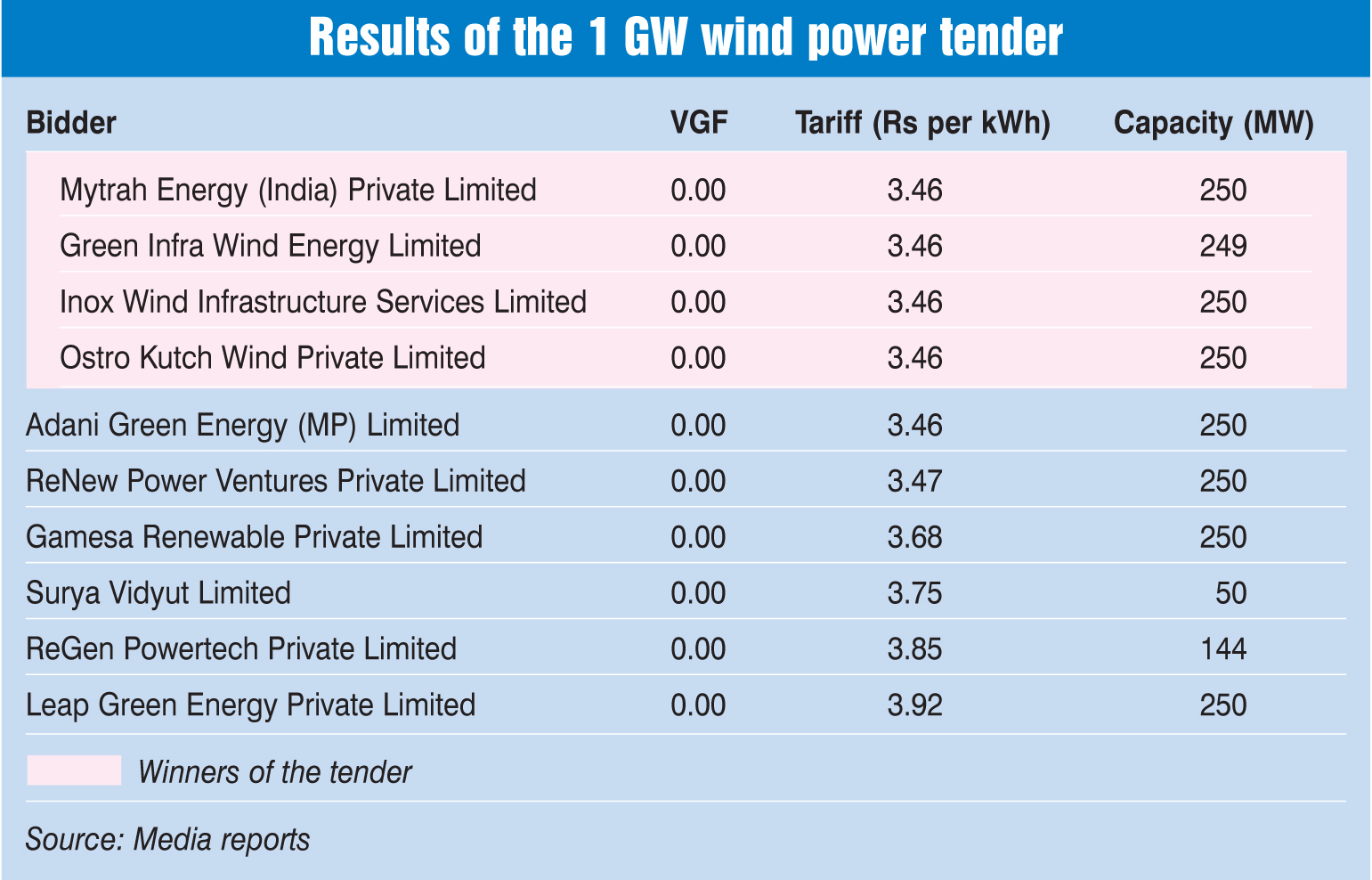

Mytrah Energy (India) Limited, Singapore-based Sembcorp Industries, IDFC Alternatives-backed Green Infra Limited, global private equity fund Actis Capital’s clean energy platform Ostro Kutch Wind Private Limited, and Inox Wind Infrastructure Services Limited bid Rs 3.46 per kWh to win contracts for 250 MW capacity each.

This winning tariff is in sharp contrast to the average wind feed-in tariff (FiT), which is close to Rs 5 per kWh across the country. Notably, the winning bid is not an outlier, as is evident from the bids placed by Adani Green Energy (MP) Limited (Rs 3.46 per kWh), ReNew Power Ventures Private Limited (Rs 3.47 per kWh) and Gamesa Renewables Private Limited (Rs 3.68 per kWh) – all quite close to the winning tariff.

Significantly, the tariffs have fallen to this level despite the prevailing uncertainties and risks, which would have been woven into the bids. These include uncertainty over the goods and services tax (GST) rate and its applicability to renewables. It has been estimated that at 12 per cent GST, wind project costs could increase by anywhere between Rs 1.5 million per MW and Rs 2.5 million per MW. This roughly translates into an addition of Re 0.07-Re 0.12 per kWh to the tariff. Further, there is no clarity on whether the generation-based incentive, a key benefit enjoyed by the wind segment, would be continued or not and, if it is, what the new terms would be. The other fiscal benefit – accelerated depreciation – will be discontinued post March 2017, as mentioned in the Union Budget 2017-18.

The viability question

While the competitive bidding mechanism has brought the wind power segment back into the limelight, the jury is still out on the financial viability of the record low bids for project developers.

The transition to competitive tariffs should help the financially stressed discoms and price-sensitive consumers in India. But as has happened in the solar energy space, competitive bidding and low tariffs can compress the returns of wind project developers. According to ratings agency ICRA, at a capital cost of Rs 65 million per MW, capacity utilisation of 24 per cent, debt tenors of 18 years and interest rates of 10 per cent, the internal rate of return for wind energy projects would be less than 10 per cent at the tariff discovered in the latest auction.

However, there are several arguments in favour of the low bids as well. First, it must not be forgotten that the wind segment has been hit by untimely payments and inordinate delays in the signing of power purchase agreements (PPAs) as distribution firms have shied away from procuring electricity generated by wind plants. This is largely because the high FiTs had no buyers of power. But now the contract winners will have a 25-year PPA with PTC India. Under the FiT regime, a renewable power generator is paid a cost plus return-based price for the power it supplies, but the risk of payment delays and grid unavailability is too high. In contrast, the recently allocated projects have guaranteed offtake accompanied by payment credibility. Power producers may not incur a loss in power as these projects will be connected to the high voltage national grid. So far, wind projects have typically been connected to the low voltage state grids, which have led to a loss in power generation.

According to experts, if developers adopt high efficiency turbines, reduce their capital expenditure, negotiate with suppliers and service providers, the tariff of Rs 3.46 per kWh will become financially feasible for generators. While the returns will still be low, they will be guaranteed to a large extent.

Impact on turbine suppliers

Such low returns will force project developers to strike hard bargains on equipment prices, which can, in turn, impact the profitability of wind turbine manufacturers. More so because, due to the auction-based allocation, developers will choose the most cost-efficient turbines rather than buy a package of land, machine and construction work at a premium from engineering, procurement and construction (EPC) contractors.

“The preferential tariff regime was used by some wind turbine manufacturers to bundle together land, turbines and EPC work. This allowed them to command a significant price premium and dominate the market. Auctions will provide more transparency, break wind turbine manufacturers’ domination and make the wind turbine market more efficient,” stated BRIDGE TO INDIA, a consulting firm, in a blog.

A sensitivity analysis carried out by Elara Securities (India) Private Limited for Suzlon and Inox Wind shows that a 100 basis points hit in the earnings before interest, taxes, depreciation and amortisation margin for a 500 MW project execution in 2018-19 could impact earnings by 3 per cent for Suzlon and by 4 per cent for Inox Wind.

However, it is important to take cognisance of the key underlying positive of the competitive bidding mechanism. According to an industry expert, turbine manufacturers do not need to be worried about their margins shrinking because what they may lose in margins, they would make up in volumes. If implemented in a planned manner, the auction route will not only ensure project continuum but will provide greater clarity regarding the pipeline of projects. This will help manufacturers build their long-term strategies.

In a recent interview with a news daily, Devansh Jain, director, Inox Wind, stated, “The government is very clear that it will be auctioning another 3-4 GW of wind capacity over the next one year. There is a very robust line-up of projects, thanks to the auctions.”

Another key positive of increasing the segment’s competitiveness through the bidding process will be a greater drive to innovate and increase efficiency so as to bring down costs. Equipment suppliers have already started working towards this. Recently, Inox Wind announced the launch of the company’s 113 metre rotor diameter wind turbine generator. The 2 MW turbine, with a 120 metre tower, which will be the highest hub height produced by Inox Wind, will significantly increase energy production.

States to join the race

The states have till now been awarding wind energy contracts and signing electricity purchase agreements on a preferential basis with the FiTs varying from Rs 3.80 per kWh to Rs 6.04 per kWh. The recently concluded auction will change this. One, the tariff gap between state- and national level auctions will shrink. Second, project awards at the state level will move towards auctions.

Competitive bidding will also help expand the market for wind power. Today, the wind market comprises only eight windy states. PTC, by purchasing wind power from developers in these states and selling it in, say, Bihar or Haryana, will help open up new markets for this power. Further, falling tariffs would attract more customers and discoms would be willing to buy more of this power given that the average tariff for coal-based power for the nine-month period ended December 2016 was Rs 3.28 per unit, as per NTPC’s data. Therefore, the industry should now get prepared for wind project allocations through competitive bidding by various state nodal agencies. The dynamics may be different in this scenario. The risks related to power offtake and payments will need to be addressed more intelligently at the state level given the stressed balance sheets of discoms and the lack of adequate transmission infrastructure.

Gearing up for a clean energy revolution

Both solar and wind power have had two key problems in their offtake – high cost and intermittency. Now, with prices plummeting to a reasonably low level, half the battle has been won. As for the other issue, intermittency, the government is taking proactive steps to address this challenge. In a development that is no less significant than the falling energy prices, it has invited bids to set up the country’s first renewable energy management centre (REMC). The REMCs will essentially have a Supervisory control and data acquisition (SCADA) system designed to predict wind and solar power generation, which will eventually help balance supply with demand.

There are four companies in the race – Siemens, ABB, Alstom and OSI – to set up the REMC in southern India. Meanwhile, Power Grid Corporation of India Limited has also come up with a tender for an REMC for the western region. As such, India will soon have a string of REMCs.

These REMCs are a part of the broader forecasting and scheduling framework devised to manage renewable power more efficiently. According to the Central Electricity Regulatory Commission’s norms for forecasting and scheduling of renewable energy, if a generator or a consumer deviates from the forecast, the penalties (paid by the plant operator) are to be absorbed by either the Power System Development Fund or the National Clean Energy Fund. This will significantly reduce the financial risks for investors as the infrastructure for managing fickleness of supply is the first attack on intermittency.

Another key revolution in the making is storage. If energy can be stored, its supply can be regulated. Storage is still at a nascent stage in India, as elsewhere. But it is bound to pick up pace. According to an estimate by Bloomberg New Energy Finance, 800 MW of storage could be built in India by 2020 – apart from the 10 GW of pumped storage planned for the next five years. A 2016 study of the Indian Energy Storage Association states that by 2022, India will have 70 GW/200 MWh of storage. Already, due to increased research and development across the world, battery prices have fallen 40 per cent since 2014.

The two aforementioned developments – the implementation of forecasting and scheduling norms and the progress in the energy storage space – will further help reduce the risks associated with renewable energy, in turn preparing the market for a clean energy revolution.

Summing up

Despite concerns related to viability, the good news is that the auction reinforces the IPP-led wind energy business model. Moreover, this will trigger higher capacity additions in the wind power market, which has so far been adding 2-3 GW per annum. Low tariffs would make wind energy more acceptable to the financially stressed discoms. The ministry is believed to be now working on the next wind power tender, which may see a capacity allocation of up to 5,000 MW. If all goes well, this will help the industry achieve the 60 GW by 2022 wind target.