Coal India Limited (CIL) is set to implement a coal pricing mechanism based on the gross calorific value (GCV) of each coal consignment from April 1, 2018. A more transparent and reliable methodology will replace the mid GCV-based pricing mechanism across coal grades. This would resolve the long-standing differences over coal quality and grade slippage between CIL and power plant developers.

Aside from the introduction of a new pricing methodology, the coal sector has witnessed several other significant changes on the pricing front in recent months. In January 2018, coal prices were increased by almost 22 per cent. Earlier, in December 2017, CIL had announced the imposition of coal evacuation surcharges. While these developments will improve CIL’s revenues, they will also increase the cost of power generation. A look at the key developments in coal pricing and their impact on the cost of power generation…

Revised coal pricing methodology

From April 1, 2018, CIL will price coal on the basis of the actual GCV of coal in a given consignment. While the coal grading system based on the total energy content per kilogram will remain, the actual price of each consignment will be calculated on the basis of a fixed rate for each unit of energy for that particular grade. To this end, each consignment will be tested for the exact quantum of energy in every kilogram of coal, which requires special systems and infrastructure. CIL’s revised coal price policy is in line with global coal pricing policies.

Currently, coal prices are based on the mid-point GCV of an energy slab having a bandwidth of 300 kCal. As long as the GCV of coal falls within the slab, its price is determined by the mid-GCV. If the actual GCV of coal is lower or higher than the mid-point GCV, it leads to over/under recovery.

Under the new pricing methodology, deterioration in coal quality even by one unit of energy would affect the selling price of coal. For a 100 unit reduction in energy content, the price of coal would vary by a minimum of Rs 19 per tonne (for the lowest grade) and a maximum of Rs 48 per tonne (for the highest grade).

The new pricing policy will help in determining accurate coal prices in a more transparent and simple manner. This would also incentivise mine managers to maintain the quality of coal since even a marginal improvement in the unit of energy will fetch additional revenue. For power producers, the policy is expected to provide some relief and address their concerns regarding grade slippages.

Meanwhile, for CIL to benefit from the new pricing mechanism, the company must ensure homogenous coal supply, control quality and provide assured supplies of higher grade coal.

Coal prices and evacuation charges

Coal prices and evacuation charges

In January 2018, CIL notified an increase of up to 22 per cent in the prices of coal grades between G6 and G14. While grades G8 to G10 witnessed a marginal increase of 3-5 per cent, grades G6 to G7 and G11 to G14 witnessed an increase of 13-22 per cent. On the other hand, the prices of the highest and lowest grades of coal have been reduced. This has made top-grade coal, which was more costly than the landed cost of imports, more marketable.

Earlier, in December 2017, CIL had introduced a coal evacuation facility charge of Rs 50 per tonne, except in cases where rapid loading silo (RLS) arrangements are in place. As per the Captive Power Producers Association, the evacuation charge has led to a 4-7 per cent increase in coal prices over the notified price. The charge has been introduced in response to a reduction in the free loading time (FLT) by Indian Railways for all mechanical loading sidings from nine hours to six hours. Reportedly, Indian Railways is likely to further reduce the FLT to three hours to optimise utilisation of rolling stock. As a result of this reduction, CIL is required to deploy high capacity loading equipment and maintain readily available loading yards and sidings. Reportedly, till now, the expenditure on these was being borne by CIL, but it will now be met through the evacuation charge.

ICRA Research estimates that the increase in coal prices along with the imposition of evacuation charges will increase the cost of coal-based power generation by 13-15 paise per unit. This is based on a hike of 15-18 per cent in the prices of thermal-grade coal (GCV of 3,100-4,300 kCal per kg). While independent power producers (IPPs) and state gencos with cost plus-based power purchase agreements (PPAs) will be able to pass on the increase in the cost of fuel to their offtakers, IPPs with competitively bid-based PPAs will depend on the extent of escalable energy charge determined by the Central Electricity Regulatory Commission. However, the profitability of IPPs having short-term PPAs with discoms is likely to be negatively affected by the rise in coal prices, since it is an uphill task for discoms to recover the increased cost of power.

As for CIL, the increase in coal prices and imposition of evacuation surcharge would significantly increase its annual income by Rs 89 billion (Rs 64 billion from coal price increase and Rs 25 billion from evacuation charges). The company will utilise the additional revenue to meet the increasing salary bills of workers and officers.

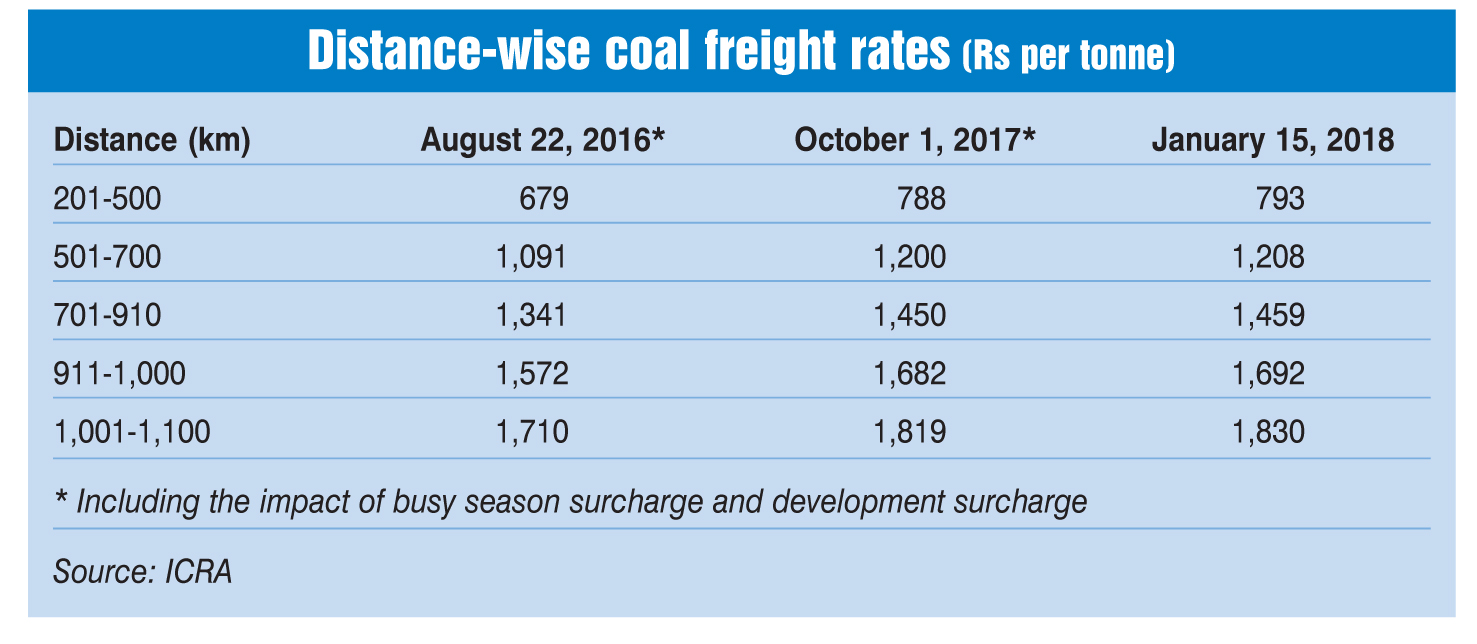

Coal freight charge rationalisation

Coal freight charge rationalisation

In January 2018, Indian Railways revised the freight rates for carrying coal by subsuming additional charges in the standard tariff. These include a 15 per cent busy season surcharge levied over and above the freight rate for nine months of the year (April to June and October to March), and a 5 per cent development charge. The lean season will now attract rates akin to those in the busy seasons.

With the rationalisation of freight rates, the overall annual transport bill is expected to improve by around 5 per cent. Notably, in recent times, the concept of “lean season” has become redundant given the current annual trend of coal transportation. Therefore, effectively, certain charges, which were earlier being levied as surcharge, have merely been added to the tariff structure. The move has been welcomed by power producers as incorporating the surcharges in the freight tariff would make the tariff determination process easier for them. Besides this, there has been a marginal increase in coal freight charges over the previous rates calculated along with the two additional charges.

To conclude, the recent developments on the pricing front, especially the revision in the coal pricing policy, augur well for the power sector. It is in the best interest of CIL and power plant developers that the former provides good quality coal that is homogenous in nature. However, it remains to be seen whether the developers are adequately compensated for the increase in their fuel cost burden in a timely manner.