In September 2018, the Central Electricity Regulatory Commission (CERC) published a discussion paper on “Re-designing Ancillary Services Mechanism in India”. Based on the international and national experiences with ancillary services, the paper proposes to transform the existing administered ancillary services mechanism in India to a market-based one. The objective is to increase the ambit of potential providers of such services at efficient costs and enhanced reliability of the grid.

Given that the existing power plants (central generating stations [CGSs]), which are allowed to participate in the reserves regulation ancillary services (RRAS) (at regulated prices) can be recalled for serving the discoms/states that have paid the capacity charges for their share in the plants, it leads to uncertainty in the availability of reserves in the system. A market-based approach will ensure greater coverage and more efficient outcome in terms of price discovery and grid balancing.

This is a welcome move. Given the changes in technology and generation mix, increasing decentralised generation and locational ancillary requirements, long-term bilateral contracts for ancillary support have become irrelevant. As the grid moves towards a tighter frequency regime (50 Hz declared a national reference frequency), next-generation reforms in the form of auction-based procurement of ancillary service would help in more robust grid management.

However, parallelly the energy markets also need to be transformed and made auction based or competitive (majority of the generation capacity currently operates on a cost-plus basis). Further, universal service obligation has to be made mandatory and implemented for effective and competitive operation of markets – energy or ancillary services. This has to be ensured at the state level with the state regulators enforcing mandatory reserve demonstration by distribution companies over the medium to long term through adequate power purchase agreements. The regulators and policymakers need to address these fundamental aspects to ensure the resilient growth of the sector. Power Line presents the key highlights of the CERC discussion paper…

Ancillary services: Indian experience

The CERC in its roadmap for the implementation of reserves in the country (October 2015) identified the requirement of primary, secondary and tertiary reserves. While primary reserves are to be maintained mandatorily by all generators, secondary reserves are to be provided at a regional level and tertiary reserves are to be maintained in a distributed manner across states. Primary reserves are being ensured through requisite amendments in the Indian Electricity Grid Code, which mandates that generating stations should not schedule beyond their installed capacity. The CERC has approved automatic generation control pilots for the implementation of secondary control. Slow tertiary control has been operational since April 2016 in the form of RRAS. Recently, the CERC ordered pilot projects for fast response ancillary services (for providing frequency regulation service) to harness the potential of hydro projects to provide fast tertiary control.

Tertiary ancillary services facilitate balancing the demand for power with supply in real time. That is, after the markets have closed (gate closure – a concept which is proposed to be introduced in India soon), the system operator ensures a demand-supply balance while maintaining grid frequency at its nominal value, without compromising on grid stability with the help of available system reserves, accessible through ancillary services.

As of now, India is following an administered mechanism for ancillary services, which has served its purpose of providing valuable experiences and lessons. Some of the observed positive impacts of the RRAS regulations include larger balancing area and improved frequency profile; better real-time congestion management; enhanced grid resilience; proper implementation of merit order; and facilitation of reserve quantification.

The existing RRAS regulations utilise the unscheduled component of capacity of thermal-based regional CGSs (which have ramping limitations), whose tariff is determined/adopted by the CERC. The National Load Despatch Centre (NLDC), through the regional load despatch centres (RLDCs), is the designated nodal agency for ancillary services operations in the country. The NLDC prepares two separate merit order stack based on the variable generation cost for up and down services. The quantum of RRAS instruction is directly incorporated in the schedule of the providers and deviations are settled as per the CERC deviation settlement mechanism (DSM) regulations. The accounting for RRAS transactions is done by the regional power committees (RPCs) separately along with the DSM account on a weekly basis. For regulation-up instructions, fixed, variable and mark-up charges (at the rate of 50 paise per kWh) are paid to the RRAS provider from the DSM pool. The regulation-down instructions are settled with such providers by paying 75 per cent of the variable charges into the pool. No commitment charges are paid to the RRAS provider.

Some of the key design challenges of the existing RRAS are the inadequacy of available reserves for ancillary services during high demand periods (due to limited coverage); lack of a clear definition of reserves (with several instances of ancillary services being used to meet demand and supply for power in same time blocks on a day-to-day basis); the absence of a detailed performance monitoring mechanism of ancillary services (including accuracy of delivery; currently only a sustained failure to provide RRAS [over three times a month] invites penalty); and absence of a definition of adequacy in terms of flexibility (in terms of ramping requirements [MW per minute] along with MW). Thermal generators are ramp-limited resources while technologies like batteries and hydro generators are energy-limited resources. Therefore, once flexibility is factored in, ancillary services procurement can be technology-agnostic.

The procedural challenges in ancillary services involve the absence of gate closure in the scheduling process under the existing RRAS regulations. This is, however, proposed to be introduced as per the CERC’s latest discussion paper (published in July 2018) on redesigning the real-time electricity markets. Another challenge relates to the need for a minimum threshold value for RRAS, up or down, to avoid too many generating stations getting a very small quantum of despatch instruction.

Ancillary services: International experience

The international experience with market design for ancillary services can be broadly classified into markets – an integrated market where the system operator centrally optimises the scheduling and despatch (followed in the US) and an exchange-based market where energy companies trade continuously at prices that clear the market (followed in Europe).

Most markets in the US procure ancillary services in the day-ahead or real-time market, which allows co-optimisation of energy and ancillary services markets. In contrast, European system operators procure the required ancillary services capacity well in advance (monthly or annually). Experience indicates that co-optimisation of markets is beneficial for both the system operator and generator – it provides flexible reliable services at minimal costs for the system operator and allows maximisation of the generator’s utilisation across both markets for the generator. Further, the integrated markets of the US follow uniform pricing where the market clearing price is received by the auction participants, encouraging them to bid at marginal costs. The pay-as-bid pricing under continuous trading implies that market participants have to anticipate the clearing price and mark up their bids accordingly. Thus, uniform pricing is a preferred method over continuous trade in advanced markets.

Proposed ancillary market design in India

Principles of the proposed ancillary market design: The new ancillary services market must be competitive and market based; transparent; provide a level playing field for all technologies (irrespective of size or type) to compete to provide such services; and be fit for the future. The future demand for various types of ancillary requirements are clear and quantified, given that the transmission constraints of ancillary services are locational and need to be defined upfront. The mechanism should ensure that there are no entry barriers (for any technology) and the system operator must be able to access the most flexible technology at the least possible transition cost.

Proposed ancillary services: The paper proposes introduction of two types of tertiary reserves – slow spinning reserves and slow non-sychronised reserves together classified as total slow reserve. Slow spinning reserves refer to operating reserves provided by qualified generators and demand-side resources within the RLDC control area that are already synchronised with the grid and can respond to instructions from the RLDC/state load despatch centre (SLDC) to make changes in the output within 15 minutes and 30 minutes. Reserves (generators) that can be started, synchronised and loaded within 15 minutes and 30 minutes are classified as slow non-synchronised reserve.

The existing ancillary services mechanism for slow tertiary reserves (RRAS) is proposed to be replaced with markets for ancillary services wherein all resources that can provide the defined services can participate. Such markets will operate both on a day-ahead basis and real-time basis through the power exchanges.

Who can participate: All interstate and intra-state (public or private) resources would be qualified to provide ancillary services depending on the technical characteristics and limitations. Eventually, retrofitted renewable energy resources would also be qualified to provide energy and ancillary services.

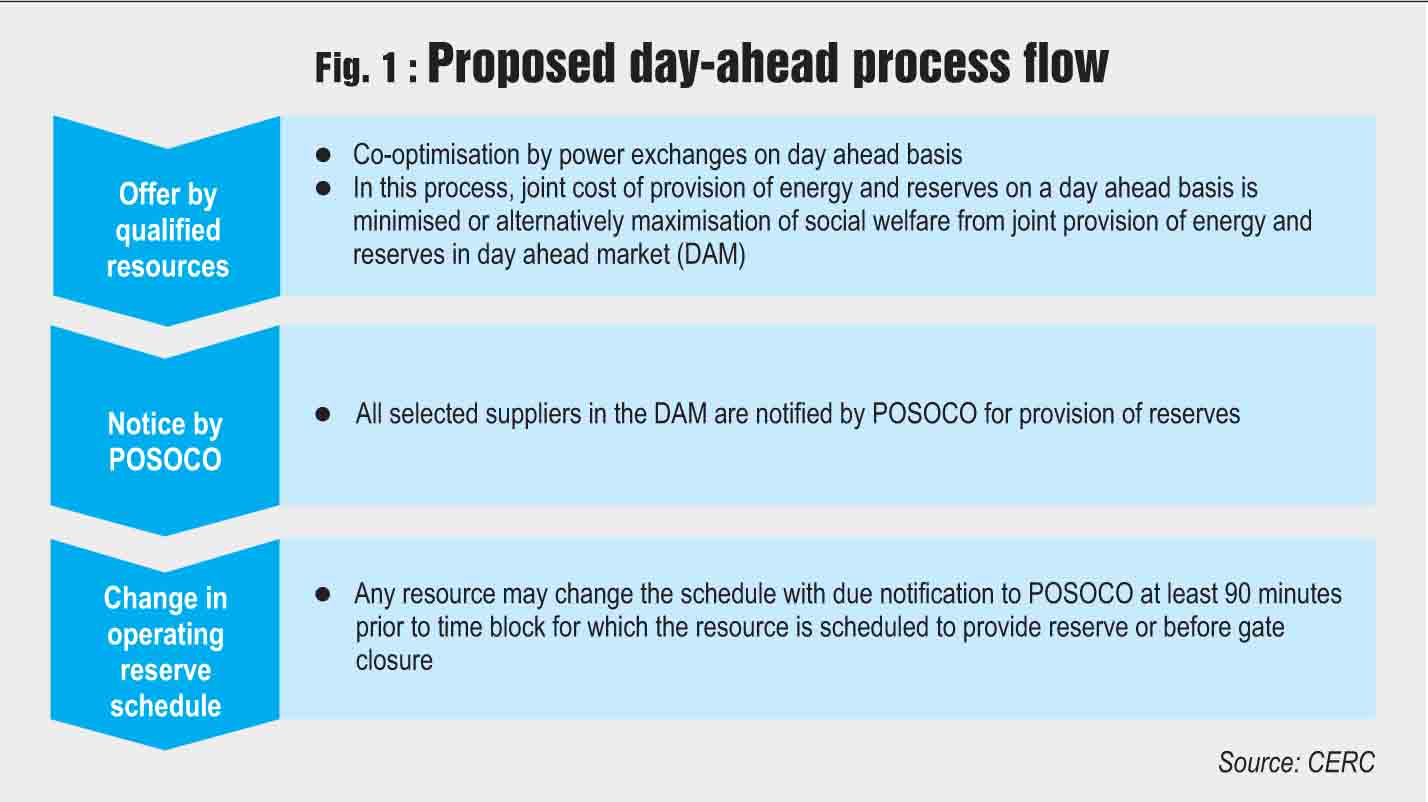

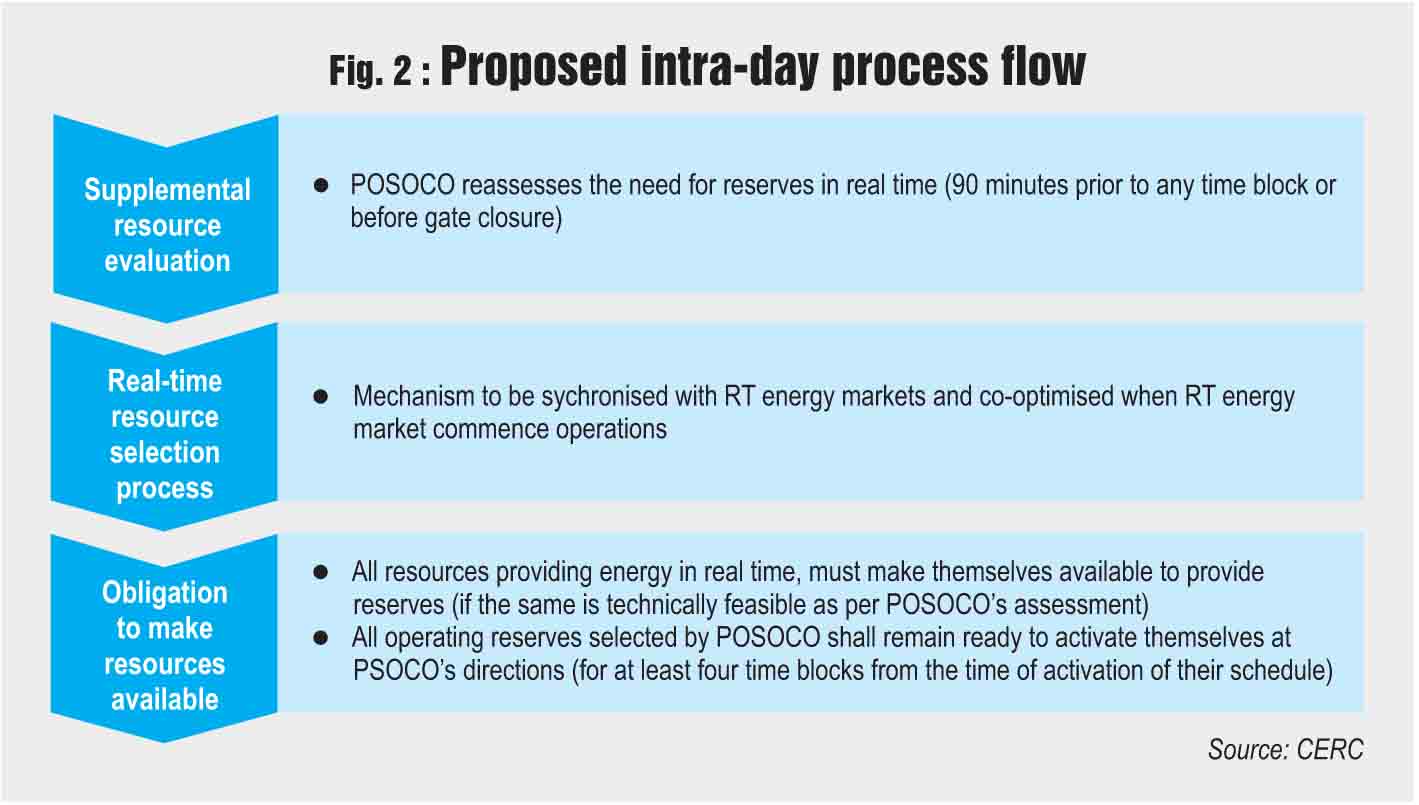

Procurement and clearing process: For the slow tertiary control, there will be a day-ahead market where generators will bid simultaneously in the day-ahead energy and day-ahead ancillary services market and the two will be cleared together. The demand curve in the day-ahead energy market is an aggregation of demand bid into the market, while the demand curve for each type of ancillary service is put forth by the NLDC/RLDCs. Based on system studies, the NLDC in coordination with RLDCs and SLDCs will determine the various types of slow tertiary services. The NLDC will further characterise these services in terms of ramp rates and duration for which continuous energy would be required from these resources. Each of the resources capable of providing tertiary reserve in the day-ahead commitment will mandatorily be required to submit availability bids (even if zero) for each hour of the next day in the day ahead market where such offers will be co-optimised with energy bids. As part of the co-optimisation process, the market clearing engine at the power exchange will determine how much of each operating reserve product a particular supplier will be required to provide in line with the reliability rules and standards. (see Figure 1). The resources designated to provide ancillary services are finally selected through a real time market. Suppliers will be selected in real-time based on their response rates, applicable operating limit, energy bid through a co-optimised real-time commitment and despatch process that minimises the total cost of energy and tertiary reserves. (For detailed intra-day process flow, see Figure 2).

Pricing: The lost opportunity of the generator foregone in the energy market will be the price of the ancillary service discovered through the markets. The costs may include the bid-in costs of the resource as well as the lost opportunity cost. Opportunity costs usually dominate the pricing of active power balancing ancillary services in organised markets. Spinning and non-spinning reserves are typically very low cost when the system is at minimum load since there are numerous generators operating below full load and have the ability to rapidly increase output. While RLDCs establish the demand curves for each type of tertiary reserve ancillary services, it will be subject to a price cap equal to the highest variable cost of the available CERC-regulated generation capacities in the country.

Performance evaluation: A predefined performance matrix will be used to release payments to tertiary reserves. This matrix will be based on the accuracy, delay and precision in response to requests from RLDCs and non-supply of services. Detailed non-compliance penalties will be defined. In extreme cases (contingencies), non-compliance of the required output level may lead to disqualification of the resources from these markets for a defined period.

Transmission corridor allocation and congestion management: POSOCO will declare in advance the available transmission corridor for real-time/ancillary services transactions. The power exchanges can accordingly factor in such margins for market clearing. Congestion management can be done as per the existing practice, including the market splitting method.

Who pays: Initially, the charges for tertiary services may be recovered from the DSM pool. Once the ancillary services market stabilises, the charges may be recovered as a “price adder” to the NLDC/RLDC service charges and recovered from the grid entities on a per unit energy basis or as a price adder in unscheduled interchange/DSM charges.

The way forward

The way forward

As the country is moving towards greater penetration of highly variable and unpredictable renewable energy sources, regulators and system operators face the challenge of ensuring efficient and economical grid operation. Ancillary services, in various forms including frequency support, voltage support and system restoration, are imperative for ensuring efficient and reliable grid operations.

Given that the Indian power system has evolved progressively (and uniquely) over the last couple of decades in phases to operate a huge synchronised grid, new concepts such as real-time markets, gate closure and co-optimisation may be introduced progressively for effective implementation. On the one hand, reforms need to ensure that discoms do not lean on the grid to meet their demand. On the other hand, the share of energy bid into the organised markets, which is currently minuscule, must also increase considerably. These measures will facilitate the smooth implementation of market-based models for ancillary services, which will be imperative as more and more decentralised sources are integrated into the grid and tighter frequency control is implemented.

Swarna Kesavan