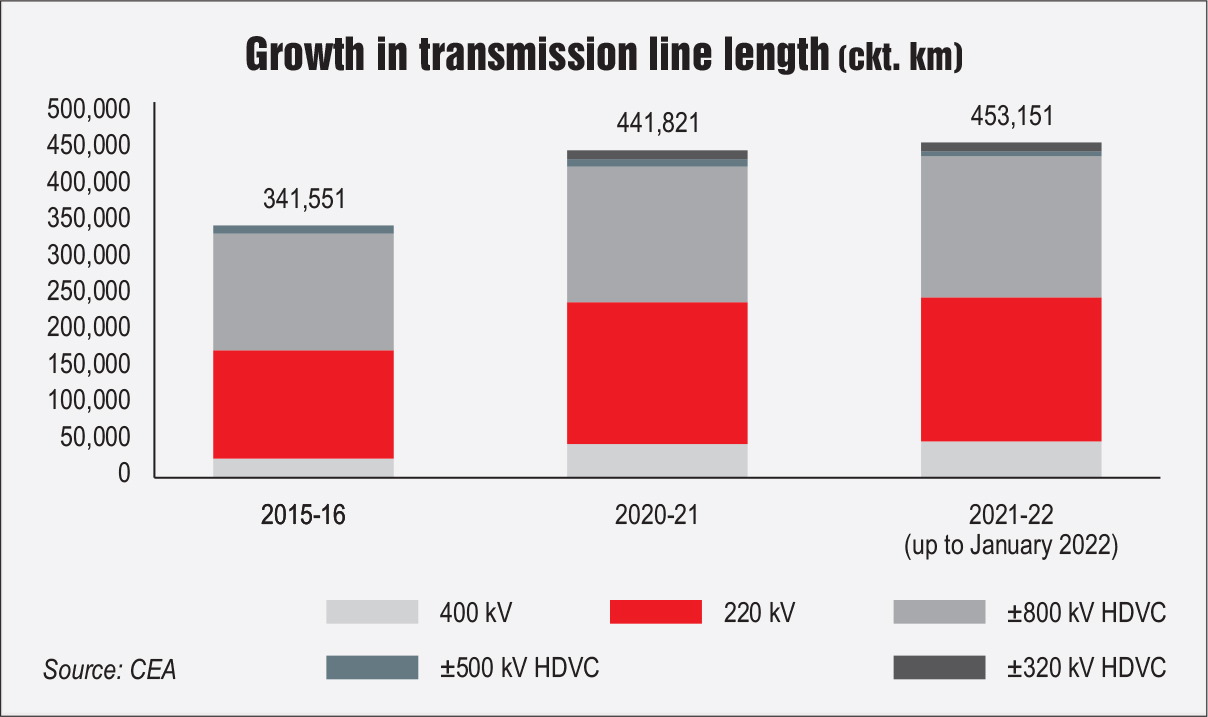

The Indian power transmission segment has grown significantly over the years, making the country’s electricity grid one of the largest synchronous grids in the world. As of January 2022, the total transmission line length (at the 220 kV level and above) stood at 453,141 ckt km, the total AC substation capacity stood at 1,055 GVA and the HVDC substation capacity stood at 33,500 MW. Between 2015-16 and 2020-21, the line length has grown at a compound annual growth rate of 5.3 per cent while AC and HVDC substation capacities have grown at 9 per cent and 14.5 per cent respectively. In absolute terms, about 100,270 ckt km of lines, about 352,000 MVA of AC substation capacity and 14,500 MW of HVDC substation capacity has been added during this period. The interregional transfer capacity has also grown considerably from 58,050 MW in 2015-16 to 112,250 MW in 2021-22 (as of January 2022).

This expansion of the transmission grid has facilitated seamless transfer of electricity from power-surplus regions to power-deficit regions, thereby optimising the use of generation resources as well as meeting the demands of end consumers. Now, the segment is set for another phase of accelerated growth, primarily driven by the need to evacuate large-scale renewables. With India targeting to meet 50 per cent of its energy needs from renewables and achieve 500 GW of non-fossil fuel capacity by 2030 as announced at COP26, significant expansion and strengthening of the interstate transmission system (ISTS) will be required. Simultaneously, the state utilities are expected to take measures to upgrade and augment intra-state transmission as well as sub-transmission networks. Power Line takes a look at the key trends and developments in the power transmission segment…

Key developments

The central government has undertaken many progressive policy and reform initiatives for the transmission segment in recent months. One of the most significant is the introduction of general network access (GNA) under the Electricity (Transmission System Planning, Development and Recovery of Inter-State Transmission Charges) Rules, 2021, which were released in a gazette notification dated October 1, 2021. The latest rules define GNA as non-discriminatory access to the ISTS, as requested by a designated interstate customer and granted by the central transmission utility (CTU) for a maximum injection or drawal in megawatts and for a specific period. A transition to GNA would provide the much-needed flexibility to state entities in purchasing electricity under contracts of varying durations without the limitations of ISTS network availability. For generators too, there will be enhanced flexibility in sales since target beneficiaries will not have to be specified.

In October again, the Ministry of Power (MoP) revised the terms of reference of the National Committee on Transmission (NCT) to fast-track the process of ISTS development. Earlier, all ISTS projects were approved by the MoP based on the NCT’s recommendations. Now, the ministry will only look at ISTS projects costing over Rs 5 billion while ISTS projects up to Rs 1 billion will be approved by the CTU and those between Rs 1 billion and Rs 5 billion will be approved by the NCT. Further, in order to encourage private participation in transmission, the MoP released revised standard bid documents (SBDs) for tendering of projects via tariff-based competitive bidding (TBCB) in August 2021. The last SBDs were issued in 2008 and there was a strong need to revise them in line with latest developments in the segment. Some of the key changes in the revised SBDs include signing of the transmission service agreement with the CTU instead of long-term transmission customers, provisions for an independent engineer during the construction phase and preparation of transmission line route survey in advance, and a reduction in timeline of the bidding process to 91 days from 145 days.

Other important policy initiatives include separation of the CTU from Power Grid Corporation of India Limited (Powergrid) to provide transparency and a level playing field in TBCB; a reduction in the lock-in period for transmission projects in order to attract investments and more competition; proposal to bring all 33 kV systems, which are currently maintained by state discoms, under STUs for better upkeep, and an extension of the ISTS charges waiver on solar and wind energy projects commissioned up to June 30, 2025. Another important development in the segment was the launch of the initial public offering of the Powergrid Infrastructure Investment Trust, the maiden infrastructure investment trust of Powergrid, in April 2021, marking the beginning of its asset monetisation drive. The Rs 77.35 billion public issue was oversubscribed nearly 4.83 times, having received bids for 2.05 billion units against an offer size of 425.4 million units. The National Monetisation Pipeline has set a target of monetising Powergrid’s transmission assets worth Rs 452 billion between 2021-22 and 2024-25.

Key programmes and initiatives

The Green Energy Corridors (GEC), initiated in 2015, is a key programme for renewable energy evacuation in the country. Under GEC Phase I, 3,200 ckt km of interstate transmission lines and 17,000 MVA of substation capacity have been commissioned. At the intra-state level, GEC Phase I targets an addition of 9,700 ckt km of transmission lines and 22,600 MVA of substation capacity with completion in 2022. Recently, the central government approved the GEC Phase II programme for intra-state transmission systems. Under this phase, projects would be set up in seven states – Gujarat, Himachal Pradesh, Karnataka, Kerala, Rajasthan, Tamil Nadu and Uttar Pradesh – for evacuation of about 20 GW of renewable energy. In addition, under the Transmission Scheme for Renewable Energy Zones (REZs), evacuation infrastructure for about 66.5 GW of renewable energy capacity (50 GW solar and 16.5 GW wind) is being created with an investment of Rs 432 billion. Another key initiative is the “One Sun One World One Grid” (OSOWOG) that envisions solar energy supply across borders. Recently, on the sidelines of the COP26 summit at Glasgow in November 2021, the UK and India agreed to combine forces of the Green Grids Initiative and the OSOWOG initiative.

TBCB update

As of January 2022, 60 ISTS projects have been bid out to public and private players since 2009. This excludes four projects which have been cancelled or are under litigation. Of these 60 projects, while 20 projects were secured by Powergrid, 40 have been won by private players. Key private players in the segment include Sterlite Power (16 projects) and Adani Transmission Limited (ATL) (14 projects).

In December 2021, ReNew Transmission Ventures Limited secured the Koppal-Narendra transmission project in Karnataka. This marked the entry of ReNew Power, a key player in the renewable energy space, in the transmission segment. At the intra-state level, ATL bagged the MP Power Transmission Package II through TBCB in September 2021.

Cross-border interconnections

Several interconnections are planned between India and neighbouring countries including a new 765 kV link between India and Bangladesh – the 765 kV Katihar (Bihar)-Parbotipur (Bangladesh)-Bornagar (Assam) Line (initially operated at 400 kV) along with an HVDC back-to-back link at Parbotipur (2×500 MW, 1×500 MW at 400 kV and second 1×500 MW at 765 kV). A 400 kV D/C new Gorakhpur and new Butwal transmission line is planned between India and Nepal. Further, a transmission line from the upcoming 900 MW Arun-3 hydroelectric project in Nepal is being developed by SJVN Arun-3 Power Development Company Private Limited, SJVN’s subsidiary. In addition, there are plans for the development of an overhead electricity link with Sri Lanka, after the earlier proposal to set up an undersea power transmission link was shelved due to its high cost..

Technology focus

Technology focus

The transmission segment is at the forefront of adopting the latest technology. The voltage level has increased from 220 kV to 765 kV, ±800 kV HVDC and 1,200 kV, and advanced technologies such as voltage source converters and FACTS are being deployed. In 2020-21, Powergrid commissioned Bipole 1 and associated HVAC and HVDC links under the ±800 kV, 6,000 MW, Raigarh-Pugalur-Trichur HVDC project. One symmetrical monopole of the VSC HVDC link was also commissioned under the ±320kV, 2,000 MW, Pugalur-Thrissur HVDC project. Another technology trend in the power transmission segment is the growth in the uptake of digital switchgear and substations. In December 2020, Powergrid, in collaboration with Bharat Heavy Electricals Limited, successfully commissioned India’s first indigenously developed 400 kV optical current transformer and digital substation components at the 400/220 kV Bhiwadi substation. Powergrid has also commissioned digital substation based on IEC 61850 process bus technology at Malerkotla, Punjab.

Remote monitoring of substations and other equipment is also gaining traction as it helps utilities reduce manual intervention. During 2020-21, eight extra high voltage substations were integrated with Powergrid’s National Transmission Asset Monitoring Centre at Manesar, Haryana for remote operation, taking the total remotely monitored substations to 242. Further, project developers are deploying LiDAR technology, drones and air cranes for the construction of transmission lines, and thermovision cameras and Android-based applications for operations and maintenance.

Challenges and the way forward

The government expects an addition of about 17,500 ckt km of transmission lines per year and 80,000 MVA of transformation capacity per year over the next three years. The National Infrastructure Pipeline has estimated a capital expenditure of about Rs 3,040 billion for the power transmission segment between 2020 and 2025. State utilities are expected to lead the transmission segment with a projected capex of Rs 1,900 billion. In addition to expanding the physical grid, utilities will increasingly need to invest in advanced and grid-enhancing technologies to improve capacity, grid resilience and stability.

Neha Bhatnagar