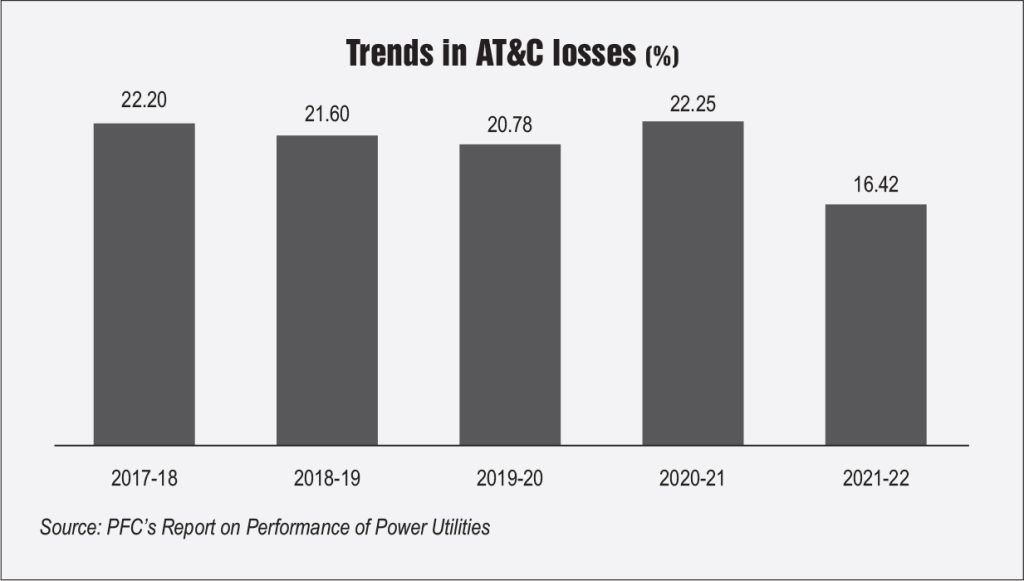

The distribution segment has continued to be the centrepiece of government reforms and schemes in the power sector for many years. In 2021, the central government launched the biggest ever distribution segment scheme, the Revamped Distribution Sector Scheme (RDSS), with an outlay of Rs 3 trillion from 2021-22 to 2025-26. The scheme is reform oriented and result based in nature and aims to reduce aggregate technical and commercial (AT&C) losses on a pan-India level to 12-15 per cent and reduce the average cost of supply (ACS) and average revenue realised (ARR) gap to zero by 2024-25. While the operational and financial performance of the segment continues to be an area of concern, there has been some improvement in the past few years. As per the PFC’s Report on Performance of Power Utilities, the aggregate technical and commercial (AT&C) losses have improved to 16.42 per cent in 2021-22 from 20.78 per cent in 2019-20.

Size and growth

The distribution network has been growing steadily, in terms of line length and transformer capacity. As per India Infrastructure Research, the distribution line length and transformer capacity have grown at a compound annual growth rate (CAGR) of about 3.8 per cent and 7.6 per cent, respectively, between 2017-18 and 2021-22. As of March 2022, the distribution line length stood at about 13.9 million ckt. km. Utility-wise, the state-owned discoms of Maharashtra and Tamil Nadu have the largest distribution networks.

During 2021-22, the total energy sales to end-consumers in the country stood at 1,136 BUs. Industrial consumers accounted for the highest energy sales with a share of 33 per cent, followed by domestic (30 per cent), agricultural (20 per cent), commercial (9 per cent) consumers, and others (8 per cent). Between 2017-18 and 2021-22, the CAGR for energy sales stood at 3.9 per cent.

Operational and financial performance

As per the PFC’s Report on the Performance of Power Utilities, aggregate losses for distribution utilities has decreased from Rs 465.21 billion in 2020-21 to Rs 310.26 billion in 2021-22. Tariff subsidy billed by distribution utilities has increased from Rs 1,333.06 billion in 2020-21 to Rs 1,437.81 billion in 2021-22. Meanwhile, tariff subsidy released by the state governments as a percentage of tariff subsidy billed by distribution utilities, increased from 84 per cent in 2020-21 to 109 per cent in 2021-22. The revenue gap, on tariff subsidy billed basis, has decreased from Rs 0.38 per kWh in 2020-21 to Rs 0.23 per kWh in 2021-22. Total borrowings by distribution utilities have increased from Rs 5,825.47 billion as on March 31, 2021, to Rs 6,179.28 billion as on March 31, 2022.

With regard to outstanding discom dues, as per the PRAAPTI portal accessed on June 12, 2023, the total dues of discoms towards gencos comprised balance legacy dues of Rs 504.43 billion and current dues of Rs 559.29 billion. This is a significant decline compared to the total outstanding dues of Rs 1.38 trillion as of June 3, 2022, when the late payment surcharge (LPS) rules were notified. The LPS rules offered a one-time relaxation to discoms wherein the amount outstanding, including the principal and the LPS, was frozen and was to be repaid by discoms through monthly instalments of 12-48 months. The scheme encouraged discoms to make timely bill payments, leading to their improved payment discipline.

On the operational performance front, AT&C losses fell to 16.42 per cent in 2021-22, almost 6 per cent lower than 2020-21 and 4 per cent lower than 2019-20 levels. This was driven by improvement in collection efficiency, which increased from 92.71 per cent in 2019-20 to 97.25 per cent in 2021-22. Meanwhile, billing efficiency remained constant at about 85 per cent during the same period.

Update on RDSS

The reforms-based and results-linked RDSS has an outlay of Rs 3,037.58 billion over five years (2021-22 to 2025-26), with an estimated government budgetary support (GBS) of Rs 976.31 billion. The scheme aims to reduce AT&C losses on a pan-India level to 12-15 per cent by 2024-25; reduce the ACS-ARR gap on a pan-India level to zero by 2024-25; and improve the quality, reliability and affordability of power supply to end-consumers. The RDSS focuses on providing financial support for smart metering system, distribution infrastructure upgrades as well as training, capacity building and other enabling and supporting activities.

In terms of financial outlay, the scheme envisages Rs 1.51 trillion (GBS: Rs 733 billion) for distribution infrastructure strengthening and modernisation; Rs 1.5 trillion (GBS: Rs 233 billion) for smart metering and related advanced metering infrastructure; and Rs 14.3 billion (GBS: Rs 10.3 billion) for training, capacity building, and other enabling and supporting activities.

So far, around Rs 1.19 trillion has been sanctioned for loss reduction works and Rs 1.35 trillion for smart metering works. Meanwhile, with regard to disbursement, Power Finance Corporation Limited and REC Limited had disbursed an amount of Rs 15,620 million and Rs 17,580.64 million respectively, to discoms, as of December 31, 2022.

With regard to smart metering, the scheme aims to install a total of 250 million smart meters during the period 2021-22 to 2025-26. So far, a total of 204.6 million smart prepaid meters, 5.4 million smart system meters for distribution transformers (DTs) and 0.2 million feeder meters have been sanctioned across the onboarded states. Meanwhile, tenders for smart metering works, covering nearly 103 million prepaid smart meters for consumer metering and 3.8 million system meters (DT and feeder) have been issued. As per the National Smart Grid Mission portal, as of June 2, 2023, 1.66 million smart consumer meters, 12,427 DT meters and 2,552 feeder meters have been installed under the RDSS. Meanwhile, with regard to distribution infrastructure/loss reduction works, tenders worth Rs 788.27 billion have been issued.

Discom privatisation in UTs

The discom privatisation process of union territories (UTs), announced in 2020, has made limited headway so far. In April 2022, Torrent Power announced a formal takeover of the power distribution operations in the UTs of Dadra & Nagar Haveli and Daman & Diu. Torrent Power holds 51 per cent stake in Dadra & Nagar Haveli and Daman & Diu Power Distribution Corporation Limited. Meanwhile, Eminent Electricity emerged as the highest bidder in the privatisation process of power distribution in the UT of Chandigarh in 2021. However, the matter of privatisation is sub judice and is yet to be concluded.

Policy and regulatory updates

- Electricity (Amendment) Bill, 2022: The Electricity (Amendment) Bill, 2022 was introduced in Parliament in August 2022, proposing significant changes to the flagship Electricity Act, 2003. Significantly, it proposes to enable competition in retail power supply through non-discriminatory open access to multiple distribution licensees in an area and to allow consumers to choose their electricity supplier. Further, it seeks to facilitate the management of power purchase and cross-subsidy in the case of multiple distribution licensees in the same area of supply. Additionally, the bill specifies penalties for default by obligated entities in meeting their renewable purchase obligations.

- Electricity (Amendment) Rules: The Ministry of Power (MoP) has notified the Electricity (Amendment) Rules, 2022, bringing about several changes to the Electricity Rules, 2005. Significantly, the new rules permit distribution companies to automatically recover from consumers, on a monthly basis, the expenses arising out of variations in fuel price and power purchase costs. Also, under the new rules, the MoP has mandated the implementation of a uniform renewable energy tariff for a central pool, from which an intermediary company will procure power to be supplied to an entity that will undertake distribution and retail supply to more than one state.

In another development, the MoP has issued the draft Electricity (Amendment) Rules, 2023 incorporating provisions for subsidy accounting and payment and the framework for financial sustainability. As per the draft, state commissions will issue quarterly reports for each discom in their jurisdiction, giving findings on demands for subsidies raised by the discom in the quarter, based on accurate accounts of the energy consumed by the subsidised category and consumer category-wise per unit subsidy declared by states. Further, the actual payment of subsidy and the gap in subsidy due and paid will also be reported.

- Electricity (Rights of Consumers) Amendment Rules, 2023: Recently, the MoP issued the Electricity (Rights of Consumers) Amendment Rules, 2023. The rules require smart meters to be read remotely at least once a day, and other pre-payment meters to be read by an authorised distribution licensee representative at least once every three months. In addition, time-of-day tariffs will come into effect from April 1, 2024 for commercial and industrial consumers with a maximum demand of over 10 kW; and April 1, 2025 for other consumers, except agricultural consumers.

- Resource adequacy framework for reliable power supply: The MoP recently issued guidelines for the resource adequacy planning framework for India, in consultation with the Central Electricity Authority (CEA). The guidelines will ensure that sufficient electricity is available to power the country’s growth, by putting in place a framework for procurement of resources by discoms in advance to meet the electricity demand in a cost-effective manner. These guidelines provide an institutional mechanism for resource adequacy, spanning from the national level down to the discom level, such that the availability of resources to meet the demand is ensured at each level. The guidelines also suggest that at least 75 per cent of the total capacity required by discoms should be secured through long-term contracts. The medium-term contracts are suggested to be in range of 10-20 per cent, while the remaining power demand can be met through short-term contracts.

- Draft guidelines for medium- and long-term power demand forecast: In April 2023, the CEA prepared draft guidelines for medium- and long-term power demand forecast. It aims to serve as a guiding document for power utilities to bring uniformity in their demand forecast approach. As per the draft, the forecast should be prepared for the medium term (more than one year and up to five years) as well as for the long term (more than five years). The long-term forecast should at least be for the next 10 years. The forecast should be reviewed on a yearly basis and updated, if required. The base year for the forecast should ideally be taken as the two-years (T-2), preceding the year during which the forecast exercise is being carried out. The CEA further proposed that the forecast should be carried out for at least three scenarios – optimistic, business-as-usual and pessimistic.

Challenges and the way forward

As per ICRA’s research, tariff orders for 2023-24 have been issued in 22 out of 28 states, as of May 2023. The tariff hikes approved remain modest across most states, despite the rising cost of supply. Delays in the pass-through of cost variations remain a key challenge for distribution companies. Moreover, the cash gap for discoms has remained high, owing to high AT&C losses and lack of timely and adequate tariff revision.

Further, as per the PFC’s report, the total sectoral debt has increased by 24 per cent to Rs 6.2 trillion from 2019-20 to 2021-22. Meanwhile, as per the 11th Annual Integrated Rating and Ranking of Power Distribution Utilities, 33 utilities did not achieve the targets set by their respective state electricity regulatory commissions in 2021-22. The sector’s regulatory assets have remained stagnant from 2019-20 to 2021-22 at Rs 1.6 trillion, highlighting the need for greater state efforts through appropriate tariff increments, capital support and efficiency measures. Five states, Tamil Nadu, Rajasthan, Delhi, Maharashtra and Kerala, have contributed heavily to the sector’s regulatory assets. To address this challenge, states are being pushed to formulate liquidation plans and not create new regulatory assets going forward. Further, there is scope for improvement in metrics such as days payable, which has fallen from 178 days in 2020-21 to 163 in 2021-22, but can be reduced further; and days receivable, which fell significantly from 159 days to 142 in the same period, but are still higher than the benchmark levels.

In the coming years, electricity flows will become increasingly complex with the growth of decentralised generation and proliferation of EV charging infrastructure. In addition, peak demand is expected to continue growing, putting pressure on discoms to provide reliable power. Going forward, effective implementation of capex initiatives under the RDSS, including smart metering, remain key to improve operating efficiencies; and timely pass-through of cost variations, optimising the operations and maintenance cost structure and payment security mechanism for recovery of dues from government bodies are some of the measures required to improve discom finances.