The Indian power sector is on the cusp of an energy transition, as the share of renewable energy in the country’s power generation is rising rapidly. Aligned with the nation’s decarbonisation and net zero targets, industrial and commercial consumers are increasingly shifting towards renewable energy sources to fulfil energy requirements. Moreover, alongside the increasing share of short-term trading volumes, energy markets in the country are evolving to facilitate greater adoption of renewable energy. This is exemplified by the emergence of innovative products such as the green term-ahead market (GTAM), the green day-ahead market (GDAM), the real-time market (RTM) and market-based ancillary services. These developments are anticipated to facilitate large-scale capacity addition of renewable energy while reducing the costs of integration.

The Indian power sector is on the cusp of an energy transition, as the share of renewable energy in the country’s power generation is rising rapidly. Aligned with the nation’s decarbonisation and net zero targets, industrial and commercial consumers are increasingly shifting towards renewable energy sources to fulfil energy requirements. Moreover, alongside the increasing share of short-term trading volumes, energy markets in the country are evolving to facilitate greater adoption of renewable energy. This is exemplified by the emergence of innovative products such as the green term-ahead market (GTAM), the green day-ahead market (GDAM), the real-time market (RTM) and market-based ancillary services. These developments are anticipated to facilitate large-scale capacity addition of renewable energy while reducing the costs of integration.

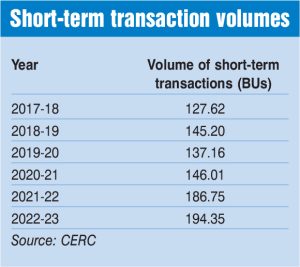

During 2022-23, short-term trading volumes stood at 194.35 BUs, marking a 4.1 per cent increase over the previous year. The volume accounted for 13.7 per cent of the total generation during this period. The volume of short-term transactions between 2017-18 and 2022-23 grew at a compound annual growth rate (CAGR) of 8.8 per cent, while power generation grew at a CAGR of 1.7 per cent. Power exchanges accounted for approximately 53 per cent (102.95 BUs) of the total transaction volume in the short-term market during 2022-23. The remaining portion includes volumes transacted through trading licensees, which accounted for a share of 17.4 per cent (33.80 BUs), deviation settlement mechanism transactions at 13.5 per cent (26.3 BUs), and bilateral transactions between discoms at 16.1 per cent (31.3 BUs).

Power exchange and bilateral transactions

During 2022-23, a volume of 102.95 BUs was transacted across three power exchange platforms, an increase of 1.5 per cent over the previous year, when an aggregate volume of 101.45 BUs was transacted on two power exchange platforms. Of the total volume, the Indian Energy Exchange (IEX) accounted for 89.2 per cent (91.85 BUs), while Power Exchange India Limited (PXIL) and Hindustan Power Exchange Limited (HPX) accounted for 9.7 per cent (9.96 Bus) and 1.1 per cent (1.14 BUs) respectively. Between 2017-18 and 2022-23, the aggregate trading volume transacted on the exchanges grew at a CAGR of 16.6 per cent.

- Day-ahead market (DAM): During 2022-23, an aggregate volume of 51.37 BUs was transacted on the three power exchange platforms in the DAM segment, a decrease of 21.2 per cent over the previous year when an aggregate volume of 65.18 BUs was transacted on two power exchange platforms. The IEX accounted for a major share in the DAM with a trading volume of 51.18 BUs, while PXIL accounted for 0.19 BUs and HPX accounted for the remaining volume.

- RTM: During 2022-23, an aggregate volume of 24.19 BUs was transacted on the power exchange platforms in the RTM segment, an increase of 21.5 per cent over the previous year wherein an aggregate volume of 19.91 BUs was transacted.

- Term-ahead market (TAM): During 2022-23, an aggregate volume of 19.4 BUs was transacted on the three power exchange platforms in this segment, an increase of 94.2 per cent over the previous year wherein an aggregate volume of 9.99 BUs was transacted. Of the total trading volume, the IEX accounted for approximately 10.1 BUs, while PXIL accounted for 8.2 BUs and the remaining 1.08 BUs were traded by HPX.

- GTAM: During 2022-23, an aggregate volume of 4.19 BUs was transacted in this segment on the three power exchange platforms, a decrease of 23.2 per cent over the previous year when an aggregate volume of 5.45 BUs was transacted. Of the total, around 2.6 BUs was traded on the IEX, while PXIL accounted for 1.5 BUs and HPX accounted for the remaining 0.07 BUs.

- GDAM: During 2022-23, an aggregate volume of 3.82 BUs was transacted in this segment on the power exchange platforms, as compared to 0.92 BUs transacted at IEX during the five months of operation in 2021-22.

During 2022-23, approximately 33.8 BUs of electricity was transacted through traders, marking a decline of 14.4 per cent from the 39.47 BUs recorded during 2021-22.

Energy markets in the country are evolving to facilitate greater adoption of renewable energy.

Open access consumer participation

Open access consumer participation

During 2021-22, over 5,628 open access (OA) consumers procured power through two exchange platforms, compared to approximately 5,400 consumers in 2020-21. In both the power exchanges, OA industrial consumers bought 9.74 BU of electricity, which formed 11 per cent of the total DAM, GDAM and RTM volume transacted in the power exchanges during 2021-22. The weighted average price (WAP) of electricity bought by OA consumers at IEX was Rs 3.20 per kWh, which was lower as compared to the WAP of the total electricity transacted through IEX (Rs 4.73 per kWh), i.e., through DAM, GDAM and RTM. However, the WAP of electricity bought by OA consumer (Rs 4.99 per kWh), was higher compared to WAP of the total electricity transacted through PXIL (Rs 3.68 per kWh) in 2021-22.

Market coupling will lead to the determination of a uniform market clearing price across the country.

Renewable energy certificates

During 2022-23, 8.16 million renewable energy certificates (RECs) were traded on the three power exchange platforms. Of the total, around 5.97 million RECs were traded on the IEX, while 2.1 million RECs were traded on PXIL and the remaining 0.09 million RECs on HPX. During the five months of 2021-22 when RECs were transacted, a total of 8.46 million RECs, comprising 1.36 million solar RECs and 7.1 million non-solar RECs, were traded on two exchange platforms.

Key developments

Market coupling: In June 2023, the Ministry of Power (MoP) directed the Central Electricity Regulatory Commission (CERC) to initiate the consultation process for market coupling and finalise the framework for its implementation. Market coupling, which involves the aggregation of buy and sell bids from all power exchange platforms in the country under a single power trading entity, will lead to the determination of a uniform market clearing price across the country.

Recently in August 2023, the CERC has issued a staff paper on market coupling. The paper discusses the regulatory provisions for market coupling, international experiences, objectives of market coupling in India, the issues and challenges in implementing market coupling, and the key points for discussion.

The development of new products, more trade activity, and positive policy and regulatory changes are expected to contribute to the power market’s expansion.

Redesign of the Indian electricity market: A group constituted by the MoP for “Development of Electricity Market in India” has proposed comprehensive solutions to address the key issues in the country’s electricity market design, such as the prevalence of inflexible long-term contracts, the lack of resource adequacy planning and the high reliance on self-scheduling by states. The report highlighted several near-term (less than one year) high-priority items to initiate power market reforms. These items include implementing security-constrained economic despatch and unit commitments for thermal fleets, operationalising ancillary services regulations, mainstreaming renewable energy participation for select capacity, introducing resource adequacy and integrated resource planning for states/utilities, and implementing time-of-day tariff.

HP-DAM: In February 2023, the IEX received the final approval from the CERC to introduce trading in high-price DAM (HP-DAM) contracts. Eligible sellers in the HP-DAM category would include gas-based power plants that utilise imported regasified liquefied natural gas and naphtha, imported coal-based power plants that utilise imported coal, and battery energy storage systems. The category of plants eligible to participate in HP-DAM will be subject to a quarterly review by the CERC. The power regulator has fixed a ceiling of Rs 20 per unit for electricity traded in HP-DAM, while a price cap of Rs 10 per unit is applicable across all the other spot power market segments.

DAM (HP-DAM) contracts. Eligible sellers in the HP-DAM category would include gas-based power plants that utilise imported regasified liquefied natural gas and naphtha, imported coal-based power plants that utilise imported coal, and battery energy storage systems. The category of plants eligible to participate in HP-DAM will be subject to a quarterly review by the CERC. The power regulator has fixed a ceiling of Rs 20 per unit for electricity traded in HP-DAM, while a price cap of Rs 10 per unit is applicable across all the other spot power market segments.

Ancillary service market: The CERC gave its approval for the power exchange platforms to launch the tertiary reserve ancillary service (TRAS) market segment in April 2023. The TRAS is a frequency control ancillary service capacity meant to keep grid frequency within a specified range. To ensure the availability of secondary reserves and accommodate variations in renewable energy supply, the TRAS framework covers qualified power plants, energy storage systems and interruptible loads ready for despatch. The implementation of TRAS commenced from June 1, 2023.

Outlook

Going forward, the implementation of several new regulations for general network access, transmission sharing, REC, and the deviation settlement mechanism in the coming months will significantly transform the electricity market. Further, the market will witness the launch of new products including ancillary markets, derivatives, capacity markets and contract for differences. These developments are projected to transform the allocation and utilisation of interstate transmission systems in the country, and will also offer discoms the opportunity to reduce their overall power purchase cost, including transmission charges, by exploring various alternatives in the market. Overall, the development of new products, more trade activity, and positive policy and regulatory changes are expected to contribute to the power market’s expansion during the coming years.