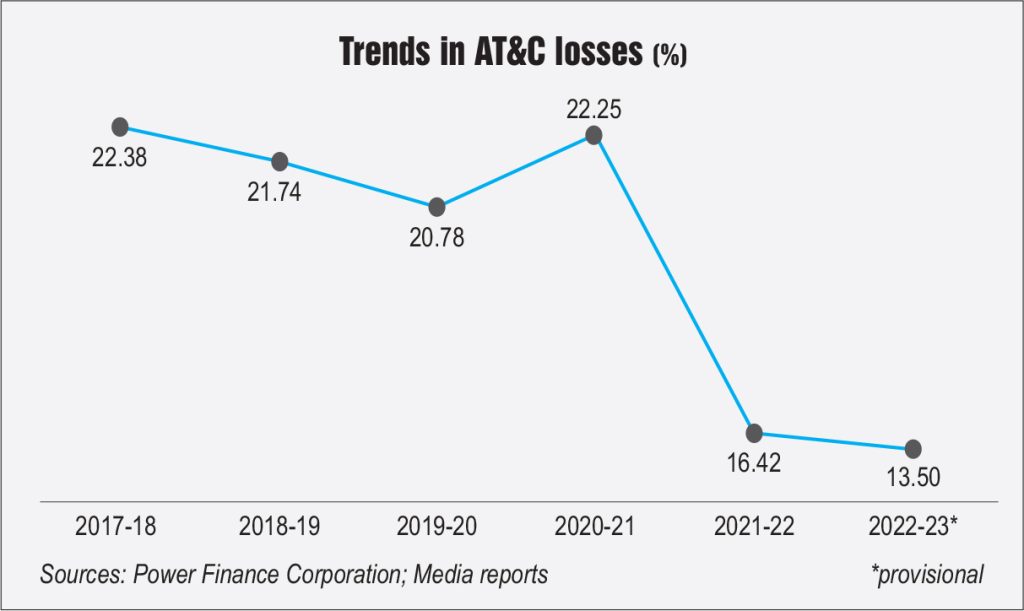

The health of the power distribution segment remains critical as India seeks to achieve ambitious energy transition targets of expanding its renewable energy installed capacity. Despite significant progress, the power distribution segment in India faces several challenges that affect its ability to provide reliable and affordable electricity to all. While the operational and financial performance of the segment continue to be areas of concern, there has been some improvement in the past few years. As per the Power Finance Corporation’s (PFC) Report on Performance of Power Utilities, aggregate technical and commercial (AT&C) losses decreased to 16.42 per cent in 2021-22 from 20.78 per cent in 2019-20.

The health of the power distribution segment remains critical as India seeks to achieve ambitious energy transition targets of expanding its renewable energy installed capacity. Despite significant progress, the power distribution segment in India faces several challenges that affect its ability to provide reliable and affordable electricity to all. While the operational and financial performance of the segment continue to be areas of concern, there has been some improvement in the past few years. As per the Power Finance Corporation’s (PFC) Report on Performance of Power Utilities, aggregate technical and commercial (AT&C) losses decreased to 16.42 per cent in 2021-22 from 20.78 per cent in 2019-20.

The government has been making significant efforts to improve the health of the power distribution segment. Key among these is the Rs 3 trillion Revamped Distribution Sector Scheme (RDSS), which aims to improve the operational efficiency and financial sustainability of discoms by providing results-linked financial assistance. Furthermore, in recent months, there have been significant policy and regulatory developments, including the introduction of the Electricity Rights of Consumer Rules, determination of green tariffs, and development of electricity markets to bring discipline in the segment, improve the tariff structure and empower consumers.

Size and growth

The distribution network has been growing steadily, in terms of line length and transformer capacity. As per India Infrastructure Research, the distribution line length and transformer capacity have grown at compound annual growth rates (CAGRs) of about 3.8 per cent and 7.6 per cent respectively between 2017-18 and 2021-22. As of March 2022, the distribution line length stood at about 13.9 million ckt. km. Utility-wise, the state-owned discoms of Maharashtra and Tamil Nadu have the largest distribution networks.

During 2021-22, the total energy sales to end-consumers in the country stood at 1,136 BUs. Industrial consumers accounted for the highest energy sales with a share of 33 per cent, followed by domestic (30 per cent), agricultural (20 per cent), commercial (9 per cent) and other consumers (8 per cent). Between 2017-18 and 2021-22, the CAGR for energy sales stood at 3.9 per cent.

Operational and financial performance

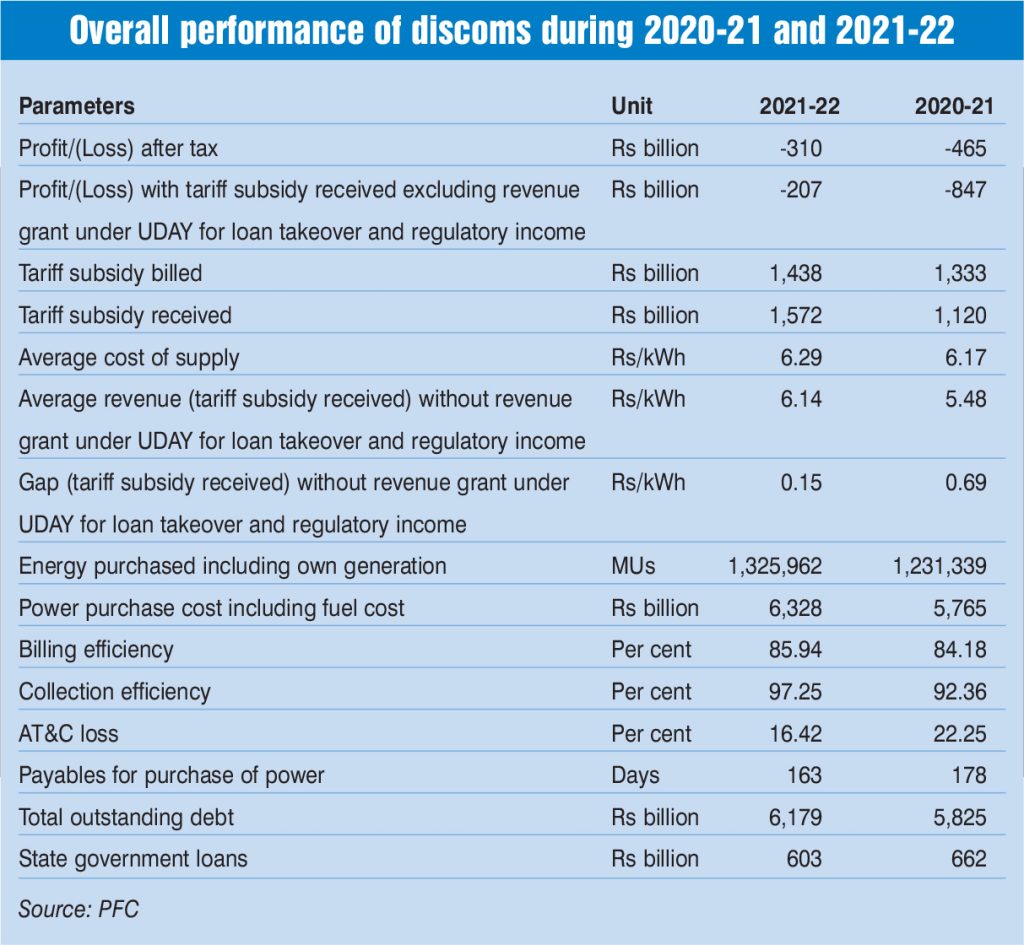

As per PFC’s Report on the Performance of Power Utilities, the aggregate losses of distribution utilities decreased from Rs 465.21 billion in 2020-21 to Rs 310.26 billion in 2021-22. Meanwhile, the tariff subsidy billed by distribution utilities increased from Rs 1,333.06 billion to Rs 1,437.81 billion. The tariff subsidy released by the state governments as a percentage of tariff subsidy billed by distribution utilities increased from 84 per cent in 2020-21 to 109 per cent in 2021-22. The revenue gap on a tariff subsidy billed basis decreased from Re 0.38 per kWh in 2020-21 to Re 0.23 per kWh in 2021-22, while the gap on a tariff subsidy received basis, excluding regulatory income and revenue grant under UDAY for loan takeover, improved significantly from Re 0.69 per kWh to Re 0.15 per kWh.

from Rs 465.21 billion in 2020-21 to Rs 310.26 billion in 2021-22. Meanwhile, the tariff subsidy billed by distribution utilities increased from Rs 1,333.06 billion to Rs 1,437.81 billion. The tariff subsidy released by the state governments as a percentage of tariff subsidy billed by distribution utilities increased from 84 per cent in 2020-21 to 109 per cent in 2021-22. The revenue gap on a tariff subsidy billed basis decreased from Re 0.38 per kWh in 2020-21 to Re 0.23 per kWh in 2021-22, while the gap on a tariff subsidy received basis, excluding regulatory income and revenue grant under UDAY for loan takeover, improved significantly from Re 0.69 per kWh to Re 0.15 per kWh.

Receivables from power sales decreased from 159 days of sale as of March 31, 2021 to 142 days as of March 31, 2022. Further, payables for the purchase of power decreased from 178 days of sale as of March 31, 2021 to 163 days as of March 31, 2022.

The total outstanding debt by distribution utilities increased from Rs 5,825.47 billion as of March 31, 2021 to Rs 6,179.28 billion as of March 31, 2022. With regard to outstanding discom dues, as per the PRAAPTI portal, accessed on September 14, 2023, the total dues of discoms to gencos comprised balance legacy dues of Rs 269.5 billion and current dues of Rs 633.3 billion. This is a significant decline from the total outstanding dues of Rs 1.38 trillion as of June 3, 2022, when the Late Payment Surcharge (LPS) Rules were notified. A one-time relaxation for discoms under the rules, wherein the amount outstanding including the principal and the LPS, was frozen and was to be repaid by discoms in monthly instalments over 12-48 months. This encouraged discoms to make timely bill payments, leading to improved payment discipline.

On the operational performance front, AT&C losses fell to 16.42 per cent in 2021-22, almost 6 per cent lower than 2020-21 and 4 per cent lower than 2019-20 levels. The AT&C losses have been further reduced to 13.5 per cent (provisional) in 2022-23. This was driven by improvement in collection efficiency, which increased from 92.71 per cent in 2019-20 to 97.25 per cent in 2021-22. Meanwhile, billing efficiency remained constant at about 85 per cent during the same period.

As per the 11th Annual Integrated Rating and Ranking of Power Distribution Utilities report, the financial deficit of discoms nearly halved in 2021-22 compared to 2019-20, despite an 8 per cent increase in gross input energy. The national absolute cash-adjusted gap in the distribution segment was recorded at Rs 530 billion in 2021-22, while the sector’s total liquidity gap was nearly Rs 3.03 trillion. The discoms’ current liabilities of Rs 6.63 trillion exceeded their overall current assets of Rs 5.57 trillion, which is almost double the amount of their current liquid assets of Rs 3.61 trillion.

Update on RDSS

Update on RDSS

The reforms-based and results-linked RDSS has an outlay of Rs 3,037.58 billion over five years (2021-22 to 2025-26), with an estimated government budgetary support (GBS) of Rs 976.31 billion. The scheme aims to reduce AT&C losses on a pan-Indian level to 12-15 per cent by 2024-25; reduce the ACS-ARR gap on a pan-Indian level to zero by 2024-25; and improve the quality, reliability and affordability of power supply to end-consumers. The RDSS focuses on providing financial support for smart metering systems, distribution infrastructure upgrades, training, capacity building and other enabling and supporting activities.

According to the Report of the Standing Committee on Energy (March 2023), the utilisation of funds under the scheme during 2022-23 stood at Rs 45.56 billion against the budgeted outlay of Rs 60 billion. Under the RDSS, detailed project reports totalling Rs 1,191.34 billion, including GBS of Rs 758.84 billion, were sanctioned. Out of the total sanctioned funds, as proposed by state/discoms, Rs 145.09 billion was sanctioned for works pertaining to high voltage distribution system implementation, cabling and feeder segregation.

On the metering front, 205.32 million consumer meters, 5.41 million distribution transformer meters and 201,695 feeder meters have been sanctioned under the RDSS, at a total sanctioned cost of approximately Rs 1.35 trillion. As of February 2023, tenders have been issued for smart metering works, covering approximately 103 million prepaid smart meters for consumer metering, as well as 3.8 million system meters for distribution transformers and feeders. Further, tenders have been issued for distribution infrastructure/loss reduction works amounting to Rs 788.27 billion.

Key developments

Electricity (Amendment) Rules: The MoP notified the rules in December 2022, bringing about several changes to the Electricity Rules, 2005. The new rules permit discoms to automatically recover payments for expenses related to fluctuations in fuel prices and power purchase costs from consumers on a monthly basis. Also, under the new rules, the MoP has mandated the implementation of a uniform renewable energy tariff for a central pool, from which an intermediary company will procure power, which will be supplied to an entity that is responsible for distribution and retail supply to more than one state.

In another development, the MoP issued the Electricity (Second Amendment) Rules, 2023, incorporating provisions for subsidy accounting and payment and the framework for financial sustainability. As per these amendments, discoms are now required to provide quarterly reports with detailed information about subsidy payments. The amendment also introduces procedures for allowing the transfer of expenses incurred by distribution licensees for the creation and upkeep of distribution assets. Followed by the second amendment, the MoP issued the Electricity (Third Amendment) Rules, 2023. As per the amendment, the captive status of generation plants will be verified by the Central Electricity Authority (CEA) if the captive generation plant and its captive user(s) are located in multiple states, as per the procedure issued by the authority with approval of the central government.

Electricity (Rights of Consumers) Amendment Rules, 2023: In June 2023, the MoP issued the Electricity (Rights of Consumers) Amendment Rules, 2023. The rules require smart meters to be read remotely at least once a day, and other pre-payment meters to be read by an authorised distribution licensee representative at least once every three months. In addition, time-of-day tariffs will come into effect from April 1, 2024 for commercial and industrial consumers with a maximum demand of over 10 kW; and April 1, 2025 for other consumers, except agricultural consumers. The new rules will help streamline the procedures and protocols for smart meter reading and improve access to smart meter data for consumers while enabling energy efficiency.

Consumers) Amendment Rules, 2023. The rules require smart meters to be read remotely at least once a day, and other pre-payment meters to be read by an authorised distribution licensee representative at least once every three months. In addition, time-of-day tariffs will come into effect from April 1, 2024 for commercial and industrial consumers with a maximum demand of over 10 kW; and April 1, 2025 for other consumers, except agricultural consumers. The new rules will help streamline the procedures and protocols for smart meter reading and improve access to smart meter data for consumers while enabling energy efficiency.

Green power tariffs: In May 2023, the MoP directed all state electricity regulatory commissions (SERCs) to take appropriate action for the determination of green tariffs, implement the green open access rules notified by the central government and align open access regulations with the notified rules at the earliest. The MoP noted that only a few states have determined green tariffs and such tariffs have been set at a rate much higher than the average power purchase cost of renewable energy procured by discoms. Further, the MoP noted that some SERCs that have notified the green energy open access regulations have not completely aligned the regulations with the MoP’s rules. Therefore, the MoP has directed the SERCs to align the regulations with the Electricity Act and the MoP’s rules. It has also directed the SERCs that have not notified green energy open access regulations to promptly do so, and failure to comply with this will result in them being held accountable for inaction under the provisions of the law.

Development of Electricity Market in India report: The MoP had constituted a group for the development of the electricity market in India to review the issues faced in electricity markets at present, identify the required interventions for implementation and lay out a roadmap for the future. The group identified key issues to be addressed in the redesign of the Indian electricity market including dominance of inflexible, long-term contracts, resource adequacy planning, reliance on self-scheduling and increasing share of renewables in the overall energy mix. The group has recommended a roadmap outlining the interventions for the near, medium and long terms such as setting up a mechanism to monitor whether adequacy of supply is being maintained by the state utilities, enhancing the efficacy of the day-ahead market, and introducing a market-based mechanism for secondary reserves.

Resource adequacy framework for reliable power supply: In June 2023, the MoP issued guidelines for the resource adequacy planning framework for India, in consultation with the CEA. The guidelines aim to ensure that sufficient electricity is available to power the country’s growth by putting in place a framework for the procurement of resources by discoms in advance to meet the electricity demand in a cost-effective manner. The guidelines also suggest that at least 75 per cent of the total capacity required by discoms should be secured through long-term contracts. Medium-term contracts are suggested to be in the range of 10-20 per cent, while the remaining power demand can be met through short-term contracts.

Guidelines for medium- and long-term power demand forecasts: In July 2023, the CEA notified guidelines for medium- and long-term power demand forecasts to provide a basic framework of medium-term and long-term power demand forecast for a discom/state/union territory (UT). As per the guidelines, the medium-term forecast should be prepared for more than one year and up to five years and the long-term forecast should be for the next 10 years at least. The detailed power demand forecasting exercise should be undertaken every five years. However, the forecast should be reviewed on a yearly basis and updated if required.

Discom privatisation in UTs: The discom privatisation process of UTs, announced in 2020, has made limited headway so far. The Government of India announced discom privatisation in UTs under the Aatmanirbhar Bharat Abhiyaan to provide better services to consumers and improve the operational and financial efficiencies of disocms. The UTs have undertaken the necessary steps for the privatisation of their electricity distribution business. However, employee unions in Chandigarh and Puducherry initially opposed the privatisation and filed writ petitions in the High Court of Punjab and Haryana, and the High Court of Madras. In September 2022, the Puducherry government invited bids for the privatisation of the UT’s power distribution for the purchase of 100 per cent shares in the company. Later, in March 2023, the Puducherry government revised its plan from fully privatising the UT and decided to transfer only 51 per cent of its share to a private entity and retain a 49 per cent stake.

The way forward

The power distribution segment is at a crucial juncture. While it is facing several challenges, it is also witnessing significant reforms, innovations and investments that have the potential to transform the sector.

The Electricity (Amendment) Bill, 2022, introduced in the Lok Sabha, seeks to facilitate the use of distribution networks by all licensees under the provisions of non-discriminatory open access. It aims to enable competition, enhance efficiency of distribution licensees and ensure sustainability of the power sector.

Overall, the ongoing reforms in the power distribution segment hold significant promise for the energy landscape. These reforms aim to enhance efficiency and reliability, and align with global efforts to transition to cleaner energy sources, promoting renewable energy integration and grid decarbonisation. Going forward, the implementation of central government schemes is expected to improve the operational and financial performance of discoms.

Akanksha Chandrakar