With the shift towards cleaner energy sources and the surge in energy demand, hydropower is poised to gain significant traction, especially in addressing the need for system flexibility. Hydropower demonstrates versatility in various functions such as peak load shaving, regulation, frequency response, and reserve support. According to the Central Electricity Authority (CEA) estimates, India has a massive hydroelectric potential of 145,320 MW, but only 29 per cent has been harnessed so far. Several policy measures have recently been implemented to promote the sector, such as the waiver of interstate transmission system (ISTS) charges for hydroelectric plants (HEPs) and the release of guidelines for pumped storage plants (PSPs) to simplify clearance processes.

Size and growth

The installed large hydropower capacity in the country stood at 46,880 MW as of November 2023. The share of hydropower in the country’s total installed capacity is 11 per cent. According to a CEA report, hydropower electricity generation from April 2023 to November 2023 was 108.59 billion units (BUs), as against 129.52 BUs in the corresponding period of the previous year. Meanwhile, during 2022-23, hydropower generation stood at 162.09 BUs, an increase of 6.9 per cent over the previous year.

During the past five years (2018-19 to 2022-23), 1,463 MW of hydropower capacity was added. Recently commissioned key projects include Uttarakhand Jal Vidyut Nigam Limited’s Vyasi HEP (2×60 MW); North Eastern Electric Power Corporation Limited’s Kameng HEP Units 3 and 4 (150 MW each); Himachal Pradesh Power Corporation Limited’s Sawra Kuddu HEP Units 1, 2, and 3 (3×37 MW); Larsen and Toubro Uttaranchal Hydropower Limited’s Singoli Bhatwari HEP Units 1, 2 and 3 (33 MW each); Himachal Sorang Power Private Limited’s Sorang HEP Units 1 and 2 (2×50 MW) in Himachal Pradesh; and Madhya Bharat Power Corporation Limited’s Rongnichu HEP Units 1 and 2 (56.5×2 MW) in Sikkim.

Policy updates

In September 2023, the central government constituted a standing technical committee to assess issues arising from geological surprises in HEPs, as well as to examine any additional time or cost involved. The committee will prepare biannual reports for the Ministry of Power (MoP) and has the flexibility to include additional members for specific projects when necessary.

In another development, In October 2023, the CEA issued guidelines for slope stability in hydropower projects (HPPs). These guidelines are applicable to HPP developers in hilly terrain, enabling them to take cognisance of past slope failures and unstable slopes in the project area, covering the affected zones. The guidelines recommend necessary remedial measures for slope stabilisation prior to construction, during construction, and post-commissioning of HPPs.

In April 2023, the MoP finalised the guidelines for pumped storage HPPs. It provides recommendations for the PSP market, PSP policies, and safe PSP development. It includes aspects such as the monetisation of ancillary PSP services to meet critical electricity market measures; reimbursement of the state GST tax, or exemption of fees on land acquisition for off-river PSPs; removal of an upfront premium for project allocation; and the identification and safe development of exhausted mines for prospective PSP sites.

Key project updates

Key project updates

In June 2023, NHPC Limited achieved a major milestone in the Subansiri Lower hydroelectric project, reaching the dam’s top elevation of level 210 metres in all blocks. Despite construction delays from 2011 to 2019 due to local protests, over 90 per cent of the project is completed. The remaining work on radial gates was planned to be finished post-monsoon, and electricity generation is expected to start by the end of 2023-24. The project aims to generate 7,500 million units of power annually.

Further, NHPC Limited is moving ahead with the development of the 2,880 MW Dibang Multipurpose Project in Arunachal Pradesh, which will be the largest HPP in the country. In addition, the state government has allotted the 1,800 MW Kamala HEP to NHPC. Internationally, it has signed an MoU for three projects in Nepal – West Seti HEP (750 MW), SR-6 HEP (450 MW) and Phukot Karnali HEP (480 MW).

In July 2023, the Arunachal Pradesh government allotted five hydro projects totalling 5,097 MW to SJVN Limited. The allocated projects are the Etalin HEP (3,097 MW), Attunli HEP (680 MW), Emini HEP (500 MW), Amulin HEP (420 MW) and Mihumdon HEP (400 MW). The development of these projects will involve an investment of over Rs 500 billion.

The pumped storage segment is rapidly growing, gaining importance for system flexibility and being considered a cost-effective large-scale storage technology. Several MoUs have been signed to set up PSPs in the past year. These include the MoU signed between the Uttarakhand government and JSW Energy to establish two PSPs with a combined capacity of 1,500 MW in Almora over the next six years; an MoU between Tata Power and the Maharashtra government for two 2,800 MW PSPs; and an MoU between NHPC Limited and Andhra Pradesh Power Generation Corporation Limited for two PSPs.

Regarding cross-border HEPs, in June 2023, SJVN Limited signed a project development agreement for the 669 MW Lower Arun HEP to be located in the Sankhuwasabha and Bhojpur districts of Nepal. The project will be constructed in five years at a cost of Rs 57.92 billion with a levellised tariff of Rs 4.99 per unit. In addition, SJVN is also executing the 900 MW Arun-3 HEP (which is at an advanced stage of construction) and the 490 MW Arun-4 HEP. In June 2023, NHPC Limited and Nepal’s Vidhyut Utpadan Company Limited signed an MoU for the development of the 480 MW Phukot Karnali HEP in Nepal. The project will harness the flow from the Karnali river for power generation, feeding the generated power into Nepal’s integrated power system. The average annual generation of the project will be about 2,448 GWh.

Small-hydro plants

India possesses a significant small-hydro power (SHP) potential of about 19,749 MW, but less than 20 per cent of this capacity has been utilised, primarily due to challenges in remote site locations and the associated costs of transmission infrastructure. The total installed SHP capacity stands at 4,986.75 MW as of November 2023. The total generation from SHP plants in 2021-22 was 10,463.55 GWh, constituting 6.12 per cent of the total power generated.

Despite shorter construction periods, the capital cost of small-hydro projects often exceeds initial estimates. The levellised tariff for SHP projects, operating at a 45 per cent plant load factor, remains relatively high, ranging between Rs 4.50 and Rs 5 per kWh. States are urged to expedite clearances, streamline procedures, and prioritise the quick development of readily available sites to optimise the SHP potential.

The Arunachal Pradesh government has launched an ambitious plan to build 50 mini HPPs for the electrification of remote villages. These 50 micro, mini, and SHP projects of 10-100 kW capacity will be built at an estimated cost of Rs 2 billion under the Golden Jubilee Border Village Illumination Programme and will be implemented in a phased manner. Under Phase I, 17 projects with an installed capacity of 1,255 kW have been initiated, entailing an estimated cost of Rs 0.5 billion.

Future outlook

Future outlook

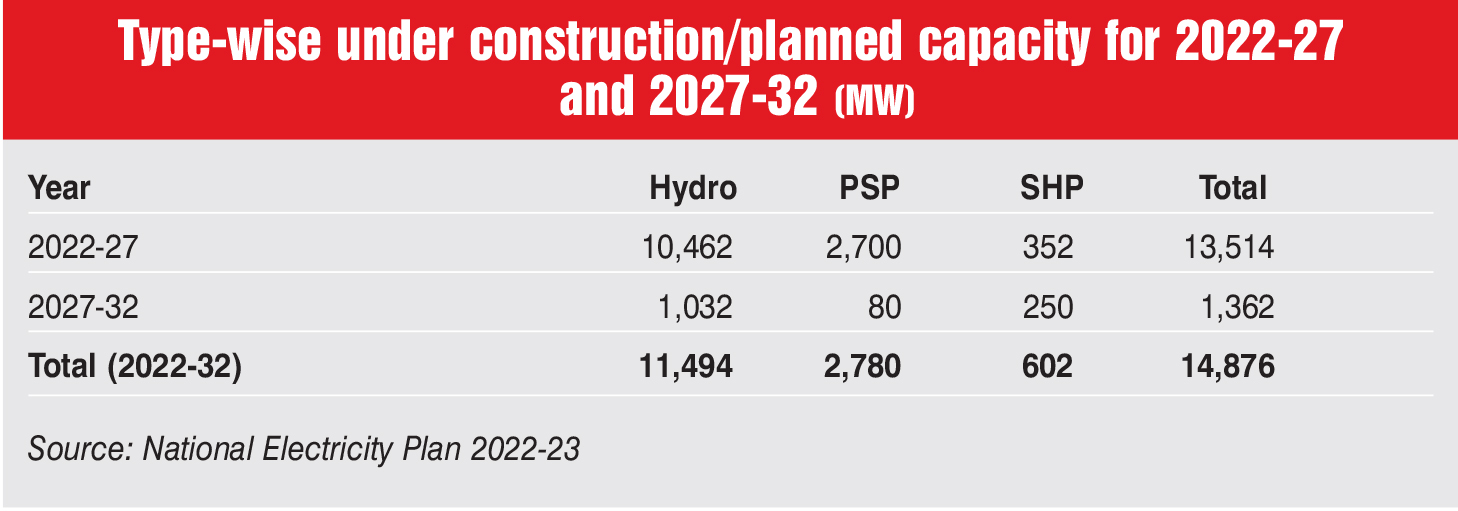

The outlook for hydropower in India is promising, with a projected 70 per cent increase in installed capacity by 2030 and nearly tripled capacity by 2047. The public sector is anticipated to maintain its dominance, contributing 78 per cent to new projects, while the private sector is expected to contribute 22 per cent. States play a crucial role, accounting for 44 per cent of the upcoming projects. According to the National Electricity Plan 2023, large hydro is expected to contribute approximately 17 per cent to the country’s projected renewable energy capacity (over 344 GW) by 2026-27. In the medium term (2022-27), 10,814 MW of conventional hydro projects and 2,700 MW of PSPs are expected, followed by 9,982 MW of conventional hydro and 19,240 MW of PSP capacity additions in 2027-32.

Issues and challenges

India faces multifaceted challenges in harnessing its hydropower potential. There are geological concerns around the seismic vulnerability of the north-eastern and himalayan regions, with seismic activity in Zone 5 posing a significant risk. Environmental challenges arise from dam construction, altering river flow patterns, causing habitat disruptions, and leading to biodiversity loss. Resettlement issues encompass involuntary displacements, inadequate rehabilitation efforts, and anti-dam activities hindering land acquisition. Net, net, overcoming obstacles requires streamlined regulatory procedures, compensation for grid services, proper geological planning, and financial incentives.