")

The power distribution sector of India is a crucial link in the electricity supply value chain. It has been facing challenges such as unreliable power supply, high aggregate and technical (AT&C) losses, old and overloaded networks, low-cost recovery, and low consumer satisfaction. This has led to extensive financial stress on discoms, which has cascaded across the power sector value chain. The government has been giving greater attention to the distribution sector with various reform measures and rules for improving the financial viability of distribution utilities and enabling them to provide 24×7 reliable and quality power to consumers. Distribution infrastructure is essential to meet the load till 2030. As such, the Central Electricity Authority (CEA), in consultation with distribution utilities, has prepared a draft Distribution Perspective Plan till 2029-30. It accounts for the pan-Indian distribution infrastructure planned by discoms to meet the projected demand by 2029-30.

The plan outlines the development roadmap for the Indian electricity distribution sector. It leverages data from 70 major discoms and various smaller entities such as special economic zones, port trusts and steel plants. It considers the projected electricity demand from the 20th Electric Power Survey (EPS) and various other relevant factors. It also assesses the requirements for developing the distribution segment, aiming to provide consumers with 24×7 reliable and high quality electricity supply. By coordinating the activities of various planning agencies, it facilitates the optimal use of resources, ultimately serving the interests of consumers. The draft DPP aims to address the anticipated peak load growth projected in the 20th EPS for each discom, enhance distribution network reliability, lower AT&C losses to below 10 per cent, and improve system efficiency and consumer satisfaction. Additionally, embracing automation and smart metering, investigating capacity building and other reforms, assessing fund requirements, and identifying gaps are also on the plan’s priority list.

Draft distribution plan – All-India summary

According to the EPS, the peak electricity demand of the country is projected to rise to 334,811 MW in 2029-30, demonstrating a compound annual growth rate (CAGR) of 6.45 per cent from 2021-22 to 2029-30. The energy requirement can increase to 2,279,676 MUs, demonstrating a CAGR of 6.46 per cent during the same period. India’s power generation will nearly double (a 97 per cent increase) to 786 GW by 2030, with renewables skyrocketing by 214 per cent to account for a dominating 62.6 per cent of the mix, ensuring sufficient capacity to meet peak demand.

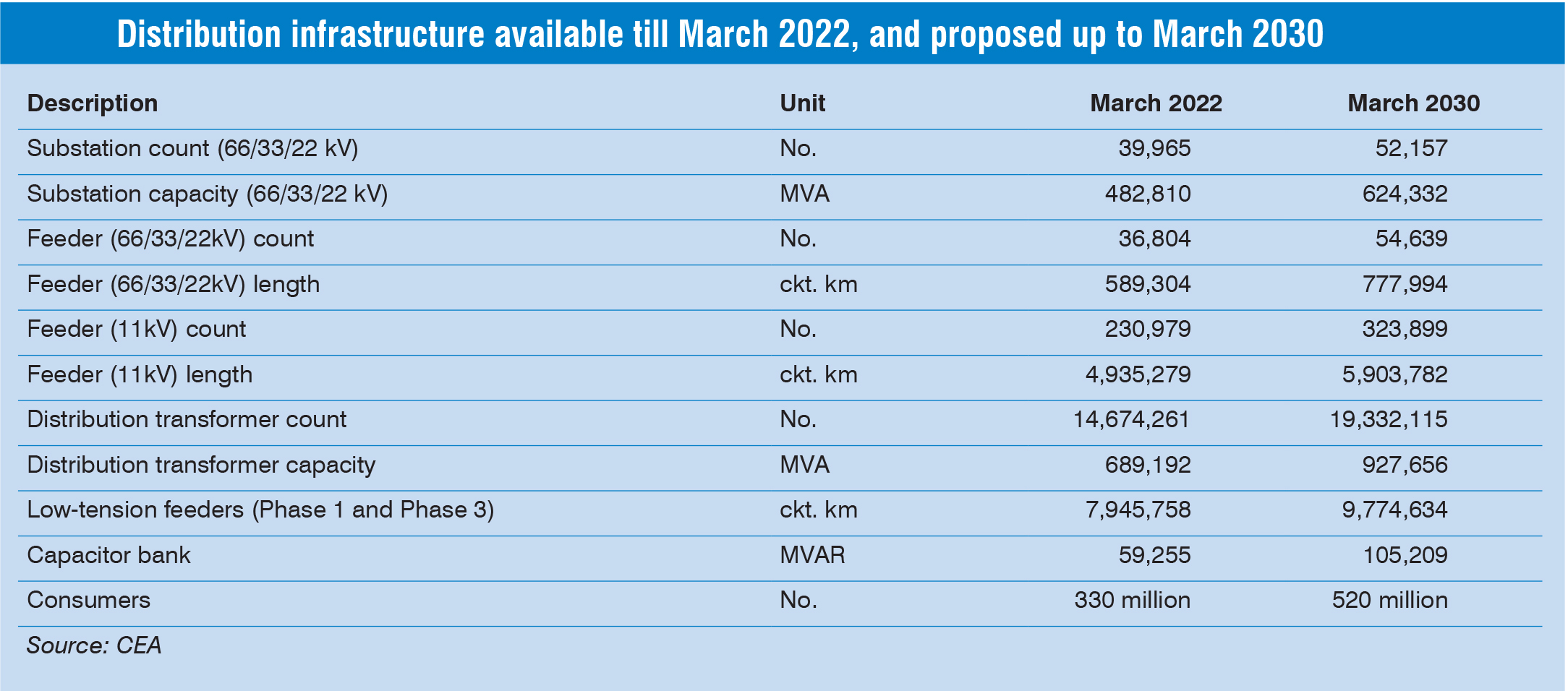

66 kV/33 kV/22 kV substations: As of March 31, 2022, the total number of power substations (66/11 kV, 33/11 kV and 22/11 kV) in the country was 39,965, with a total installed capacity of 482,810 MVA. This is expected to increase to 624,332 MVA by 2029-30, marking an increase of 29.31 per cent. During 2022-23 to 2029-30, it is envisaged that another 12,192 substations will be added with a total capacity of 141,522 MVA. State-wise, the maximum capacity addition in terms of MVA during 2022-30 is planned in Gujarat (27,342 MVA), while the maximum addition in terms of number of substations is planned in Uttar Pradesh (1,804 substations).

66 kV/33 kV/22 kV feeders: In March 2030, 66 kV/33 kV/22 kV feeders are projected to increase to 54,639 from 36,804 in March 2022. As of March 2022, the total length of the feeder infrastructure was 5,89,304 circuit kilometre (ckt. km), which is estimated to grow by 188,690 ckm by March 2030, marking an increase of 32 per cent. The total projected installed feeder line will be at 777,994 ckt. km in March 2030. State-wise, the maximum feeder addition is planned in Karnataka (3,102 feeders), and the maximum length addition in Uttar Pradesh (34,674 ckt. km).

11 kV feeders: As of March 31, 2022, the country had 230,979, 11 kV feeders with a combined length of 4,935,279 ckm. The plan aims to add 92,920 new 11 kV feeders with a total length of 968,503 ckt. km between 2022-23 and 2029-30. This will bring the total number of 11 kV feeders to around 323,899 and increase the overall network length to approximately 5,903,782 ckt. km – a 19.62 per cent increase from 2022. Rajasthan leads the pack with the highest planned feeder addition in 2030 (12,048 feeders or 165,838 ckt. km),

11 kV feeders: As of March 31, 2022, the country had 230,979, 11 kV feeders with a combined length of 4,935,279 ckm. The plan aims to add 92,920 new 11 kV feeders with a total length of 968,503 ckt. km between 2022-23 and 2029-30. This will bring the total number of 11 kV feeders to around 323,899 and increase the overall network length to approximately 5,903,782 ckt. km – a 19.62 per cent increase from 2022. Rajasthan leads the pack with the highest planned feeder addition in 2030 (12,048 feeders or 165,838 ckt. km),

Distribution transformers (33/0.4 kV, 22/0.4 kV, 11/0.4 kV): As of March 31, 2022, India had 1.47 million distribution transformers (DTs) with a combined capacity of 6.89 million MVA. Its electricity distribution network is planning an addition of 46.5 million new DTs between 2022-23 and 2029-30. This represents a substantial 34.6 per cent increase in DT capacity, bringing the total to a staggering 9.28 million MVA by the end of the decade. The maximum DT capacity addition during 2022-30 is planned in Maharashtra (47,094 MVA), and the maximum DT addition in terms of numbers in Gujarat (765,927 DTs). LT feeders (400 V/230 V): As of March 31, 2022, India’s low tension (LT) power grid consisted of 22,31,495 km of single-phase lines and 57,14,263 km of three-phase lines. The plan aims to add nearly 5 million km of single-phase lines and over 12.6 million km of three-phase lines by 2030. This will result in a total LT network length of approximately 97.7 million km, with three-phase lines constituting the majority (around 69 per cent) of the infrastructure. The maximum feeder addition during 2022-30 is planned in Uttar Pradesh.

HT/LT ratio: India’s power distribution network is facing a declining HT/LT ratio, a key indicator of technical losses and voltage stability. As of March 31, 2022, the national ratio stood at 0.62. It is expected to dip further to 0.6 by 2030. A higher ratio, ideally 1 or above, signifies lower losses and better voltage for consumers.

Punjab has emerged as a leader with a projected HT/LT ratio of 1.87 by 2030, showcasing the benefits of this approach. Other states such as Arunachal Pradesh, Gujarat, Haryana, Madhya Pradesh, Mizoram and Rajasthan are also expected to cross the crucial ratio of 1.

Capacitors: As of March 31, 2022, the country had a total capacity of 59,255 MVAr. The ambitious plan aims to add nearly 46,000 MVAr of capacitors by 2030, marking a remarkable 77.6 per cent increase. This nationwide effort will bring the total capacity to approximately 105,209 MVAr. In state-wise additions, Rajasthan leads the way, with the largest planned capacitor expansion.

SCADA and RT-DAS: Supervisory control and data acquisition (SCADA) coverage will jump from 2,377 substations in 127 towns to 13,553 in 1,393 by 2030. Real-time monitoring capabilities will also be significantly expanded through real-time data acquisition systems (RT-DAS), covering 17,384 substations across 1,096 towns in 2030, from 3,867 substation in 894 towns in March 2022.

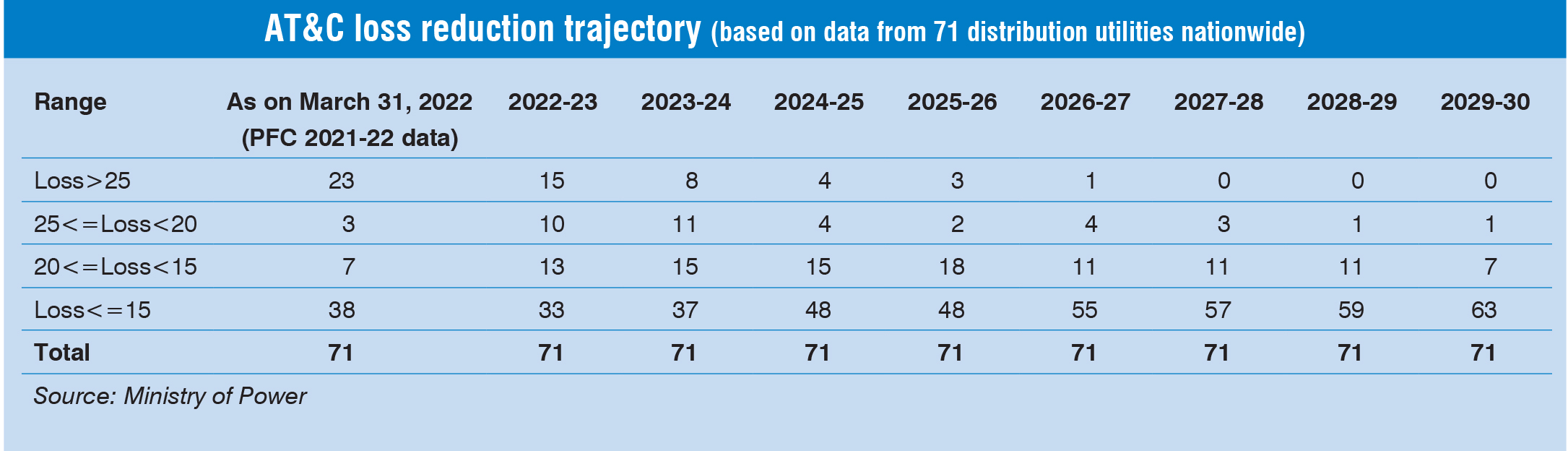

AT&C losses

Aggregate technical and commercial (AT&C) losses serve as a measure of both the technical and the financial efficiency of distribution utilities. It displays the combined total of technical and commercial losses. The central government is actively pushing states to decrease their AT&C losses through the Revamped Distribution Sector Scheme (RDSS), which aims to reduce these losses to the national range of 12-15 per cent and close the gap between the average cost of supply and the aggregate revenue requirement by fiscal year 2024-25.

Estimated fund requirement and availability

Estimated fund requirement and availability

Based on the details received from utilities, about Rs 4.28 trillion will be required for upgradation of distribution infrastructure during 2022-27, of which about Rs 1.89 trillion will be available to discoms, including funds sanctioned under the RDSS. The available funds will be around 44 per cent of the total investment required up to 2027.

Conclusion

Having achieved nationwide household electrification, the state governments are now focused on delivering 24×7 reliable and high quality power to all consumers while simultaneously striving to bring down AT&C losses to under 15 per cent. To support this objective, the central government is offering financial assistance through this RDSS.

However, in order to reduce AT&C losses further, utilities need to concentrate on reducing technical losses. Improving the HT/LT ratio can reduce technical losses while improving the voltage profile at the consumer end. The HT/LT ratio can be increased either by adopting high voltage distribution systems or increasing the HT line length. The use of IT in the distribution segment would also enable automated energy accounting and auditing, and play a major role in reducing AT&C losses and providing reliable power supply to consumers. Access to consumption data and outage data, and the speedy redressal of complaints would also improve consumer satisfaction.

India’s distribution segment faces challenges but there are also ambitious plans to build a robust future. With a projected rise in peak demand, the infrastructure expansion outlined in the draft distribution plan is intended to ensure sufficient capacity, with a heavy reliance on renewables. Moreover, the plan focuses on best practices for operations and maintenance, improvement in system capacity and resilience, better demand-side management, tariff structures, human resources, consumer services metering, loss reduction, safety, adoption of new technology, smart distribution, and capacity building, which can play a pivotal role in making the segment more sustainable and viable.

Muskan Aggarwal