Transformers are vital and costly elements of the grid, serving a pivotal function in maintaining uninterrupted electricity transmission over extensive distances. The rising demand for transformers is being propelled predominantly by the expansion of the transmission and distribution sector. The transformer market demand will witness a transformative surge driven by India’s ballooning power demand, a manufacturing push and electrification, along with the green energy transition (500 GW by 2030), which has triggered a revival of transmission and distribution capex activity. The capex envisaged in the power transmission segment alone is expected to be Rs 4.75 trillion by 2027, as per the Central Electricity Authority’s draft National Electricity Plan (Volume II).

Transformers are vital and costly elements of the grid, serving a pivotal function in maintaining uninterrupted electricity transmission over extensive distances. The rising demand for transformers is being propelled predominantly by the expansion of the transmission and distribution sector. The transformer market demand will witness a transformative surge driven by India’s ballooning power demand, a manufacturing push and electrification, along with the green energy transition (500 GW by 2030), which has triggered a revival of transmission and distribution capex activity. The capex envisaged in the power transmission segment alone is expected to be Rs 4.75 trillion by 2027, as per the Central Electricity Authority’s draft National Electricity Plan (Volume II).

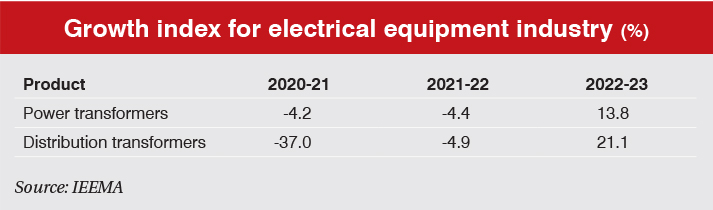

As per the Indian Electrical and Electronics Manufactures’ Association’s (IEEMA) estimates, during 2022-23, the power and distribution transformer segments showed a consistent growth of 14 per cent and 21 per cent respectively on the back of renewed domestic demand. In addition, India is being seen as a preferred transformer supplier for the US and European markets amidst ongoing tensions in Ukraine and Russia.

Size and growth of India’s grid

India’s alternating current (AC) transformation capacity has steadily increased over the years, reaching 1,217.58 GVA across the 220-765 kV levels in March 2024. Between 2018-19 and 2023-24, the AC transformation capacity demonstrated a compound annual growth rate (CAGR) of 6.8 per cent.

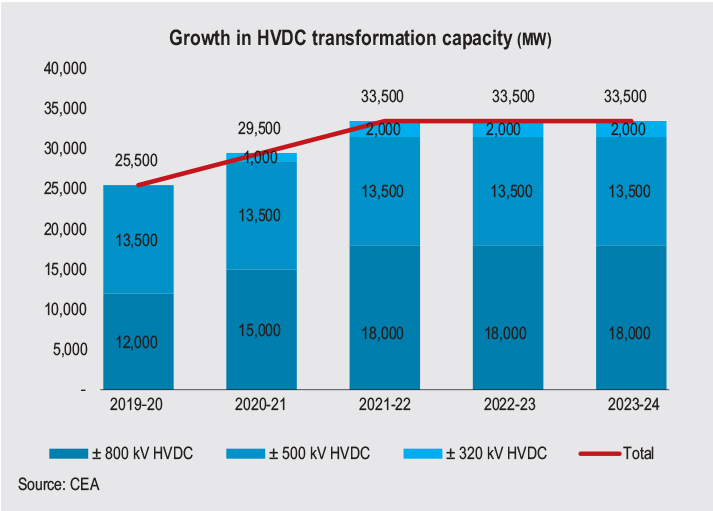

In addition, the high voltage direct current (HVDC) transformation capacity stands at 33,500 MW, of which the majority, 54 per cent, is at the ± 800 kV level; while 40 per cent is at the ± 500 kV level and the remaining 6 per cent at the ± 320 kV level. Between 2018-19 and 2023-24, the HVDC transformation capacity experienced a CAGR of 8.3 per cent.

In the distribution segment, as per India Infrastructure Research, as of March 2022, nearly 902 GVA of transformer capacity is operational at the 33 kV level and below, across 46 utilities in the country. Between 2017-18 and 2021-22, transformer capacity witnessed a CAGR of 7.6 per cent.

Key demand drivers for transformers

Government policy initiatives: Government initiatives have been instrumental in shaping the trajectory of the transformer market in India. Programmes such as the Green Energy Corridors (GEC) initiative and the Revamped Distribution Sector Scheme have been pivotal in bolstering electrification, upgrading transmission infrastructure and ensuring last-mile connectivity. About 19.4 GW of renewable energy capacity is planned to be integrated into the intra-state system under the GEC-II scheme. These initiatives not only stimulate demand for transformers, but also catalyse investments in modernisation and capacity enhancement across the power sector value chain.

Renewable energy integration: The installed renewable generation capacity posted an impressive CAGR of 14.58 per cent between financial years 2016 and 2023. The country has ambitious renewable energy targets of integrating 500 GW of renewable energy by 2030. As per the Central Electricity Authority’s report on “Transmission System for Integration of over 500 GW Renewable Energy Capacity by 2030”, 50,890 ckt. km of interstate transmission system-connected transmission lines and 433,575 MVA of substation capacity are required for integrating additional wind and solar capacities by 2030. Much of this new leg of transmission capex is for long-distance renewable energy connectivity of over 220 kV voltage levels. This transition will necessitate the deployment of advanced transformers capable of efficiently managing the intermittent nature of renewable power generation. As the country moves towards its renewable energy goals, the demand for transformers equipped with smart grid technologies, phase-shifting capabilities and voltage regulation features is expected to soar, reshaping market dynamics.

EV charging networks and data centres: Strong demand from high-growth end markets, such as data centres and EV charging networks, is expected to place additional stress on grid capacity and resiliency, and require new, modern transformers.

Railways: The Indian Railways is moving towards high speed trains, which has led to increased demand for transformers between the 66 kV and 133 kV voltage levels. The faster roll-out of high speed trains, metros and freight corridors is expected to contribute to the significant transformer demand in India over the next few years.

Transformer technology trends

Transformer technology trends

Technological innovations are revolutionising the transformer landscape, driving efficiency gains, reliability improvements and enhanced grid resilience. As the demand for electricity continues to rise, the extra high voltage and ultra high voltage power transformer market is expected to witness further growth in the coming years. These transformers play a crucial role in transmitting electricity over long distances with minimal losses, making them essential for efficient power distribution networks. HVDC transformers are pivotal for efficient long-distance power transmission, converting AC to DC in converter stations and facilitating seamless integration of renewable energy. Coupling transformers with flexible AC transmission systems enables precise control and bidirectional power flow between grids and devices such as static synchronous compensators, improving system efficiency and stability.

Meanwhile, smart transformers, leveraging internet of things, artificial intelligence and predictive analytics, enable real-time monitoring, remote diagnostics and proactive maintenance, optimising asset performance and minimising downtime. Additionally, advancements in insulation materials, cooling systems and design optimisation techniques are paving the way for compact, energy-efficient transformers capable of withstanding diverse operating conditions.

Energy efficiency has emerged as a key priority for utilities and industries seeking to mitigate environmental impact and optimise operational costs. Energy-efficient transformers, including amorphous core transformers and eco-friendly ester-filled transformers, are gaining traction owing to their superior performance, reduced losses and lower carbon footprint. Furthermore, initiatives promoting eco-friendly practices, such as the adoption of biodegradable insulating fluids and environmentally sustainable manufacturing processes, are reshaping industry norms and consumer preferences. Ester-filled transformers offer enhanced fire safety and environmental benefits over mineral oil-filled ones, while dry-type transformers, using air or gas insulation, ensure reliability and safety with minimal maintenance.

Distribution transformers, autotransformers, amorphous core transformers and mobile transformers cater to diverse needs, ensuring reliable power supply, energy conservation and rapid deployment in emergencies. It is also expected that steel mills using glass furnaces will transition to arc furnace transformers because of pollution regulations, contributing to higher demand for suppliers.

The advent of digitalisation and automation is ushering in a new era of transformer management, characterised by data-driven insights, predictive maintenance strategies and autonomous operation. Advanced monitoring systems, supervisory control and data acquisition integration, and cloud-based platforms enable utilities to harness vast amounts of operational data to optimise asset utilisation, enhance grid stability and streamline maintenance workflows. Moreover, the proliferation of distributed energy resources and microgrids necessitates agile, adaptive transformers capable of dynamically managing bidirectional power flows and voltage fluctuations.

Issues and challenges

Various existing transformers are nearing the end of their operational lifespans, leading to concerns regarding reliability, efficiency and safety. Additionally, the insufficient capacity of transformers to handle growing electricity demand exacerbates grid congestion and compromises power quality. Addressing these issues necessitates significant investments in transformer refurbishment and replacement, as well as capacity expansion, posing financial and logistical challenges for utilities and stakeholders. Traditional transformers often lack advanced monitoring and control capabilities essential for optimising grid operations, integrating renewable energy sources and mitigating power disruptions. Embracing innovation in transformer design, materials and digitalisation is imperative to enhance efficiency, reliability and resilience. However, transitioning to smart transformers and digital solutions requires substantial investments, technical expertise and regulatory support. Moreover, the transformer industry in the country faces vulnerabilities stemming from supply chain disruptions, and dependencies on imported components and raw materials. Diversifying supply sources can enhance supply chain resilience and reduce dependency on imports, fostering greater self-reliance and sustainability. Further, regulatory and policy uncertainties pose significant challenges to the transformer market, impacting investment decisions, market dynamics and technological advancements. Inconsistent policies, regulatory bottlenecks and delays in project approval create ambiguity and hinder industry development.

Outlook

According to market experts, the transformer industry is flushed with orders and the demand outlook is positive vis-a-vis end use in various industries such as railways and renewables. The pent-up demand from industrial expansions backed by a rise in capex is leading to higher consumption of power in India, in turn leading to improved order books for transformer manufacturers.

The transformer market in India is poised for robust growth, driven by a confluence of demand drivers, technological innovations and policy imperatives.

The government’s continued focus on infrastructure development, coupled with investments in smart grid technologies and renewable energy integration, will fuel demand for advanced transformers across the utility, industrial, and commercial segments.

Overall, the transformer market in India is undergoing a paradigm shift, driven by transformative trends and disruptive technologies. As the country embarks on its journey towards a sustainable, electrified future, the role of transformers emerges as critical enablers of energy transition and grid modernisation. By embracing innovation, fostering collaboration, and aligning with best practices, the transformer industry is poised to emerge as a key player, powering growth and sustainability, going forward.