Improving the financial and operational performance of state-owned power utilities remains a persistent challenge in the sector. While the debt levels of both distribution and generation utilities continue to exceed desirable thresholds, the distribution segment showed significant improvements in FY 2023, as per the Power Finance Corporation’s (PFC) latest report on the performance of state power utilities for 2022-23.

The all-India aggregate technical and commercial (AT&C) losses for distribution utilities was 15.3 per cent in FY 2023, lower than the 16.23 per cent in FY 2022. Payables for power purchases and billing efficiency showed an improvement as well. Transmission utilities showed profit growth and improved net worth, while generation utilities saw mixed results, with some registering losses despite overall industry profitability.

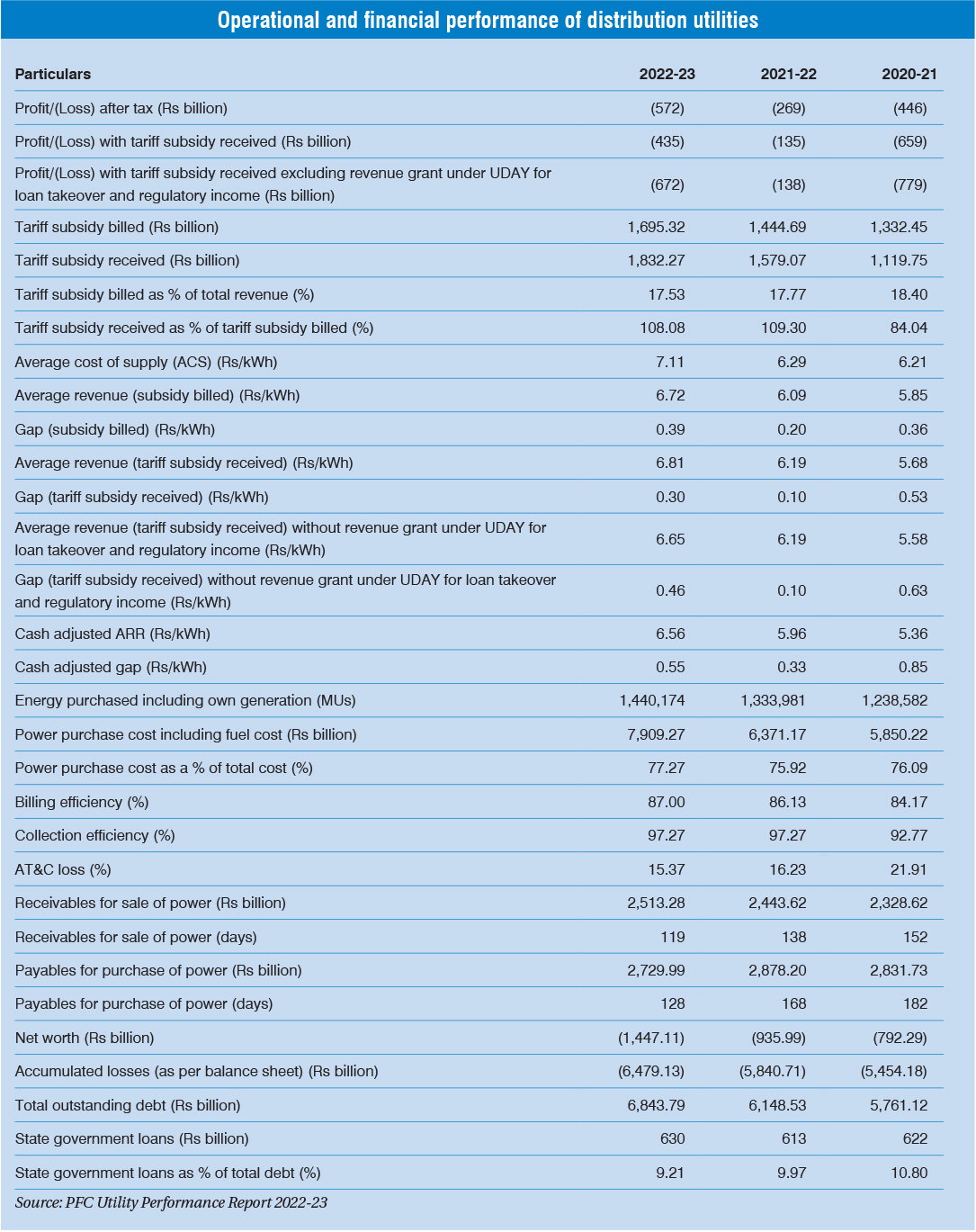

The report, which gives a detailed overview of key financial and operational metrics for these utilities, is based on a comprehensive survey encompassing 119 power utilities, including gencos, transcos and discoms, including power departments. The report is compiled based on audited/provisional annual accounts of the utilities. Of the 119 utilities, 104 have provided audited accounts and four have provided provisional accounts.

Power Line presents the key highlights of the report…

Performance of distribution utilities

Overall AT&C losses for distribution utilities improved from 16.23 per cent in 2021-22 to 15.37 per cent in 2022-23. Among the state sector utilities, Dakshin Gujarat Vij Company Limited (DGVCL) registered the least AT&C loss (1.68 per cent). Overall, 34 utilities had AT&C losses lower than the all-India national average. The top five among them were DGCVL (1.68), DNHDDPDCL (3.58), Torrent Power Surat (3.69), Brihanmumbai Electricity Supply and Transport Undertaking (BEST) (4.18) and Torrent Power Ahmedabad (4.04). At the other end of the spectrum were state utilities such as Arunachal PD (51.7), Nagaland PD (45.81), Jharkhand Bijli Vitran Nigam Limited (JBVNL) (30.28), Ladakh PD (30.33) and Sikkim PD (36.69), which had the highest AT&C losses.

The billing efficiency improved from 86.13 per cent in 2021-22 to 87 per cent in 2022-23. The top five utilities with the highest billing efficiency as per the report were the Goa PD (99.07), DGVCL (98.37), DNHDDPDCL (98.38), Torrent Power Surat (96.83) and Torrent Power Ahmedabad (96.26).

The aggregate losses for distribution utilities increased from Rs 269.47 billion in 2021-22 to Rs 572.23 billion in 2022-23. Based on PFC’s data, the states with the highest loss levels were Uttar Pradesh with an aggregate loss of Rs 155 billion, followed by Telangana at Rs 111 billion and Tamil Nadu at Rs 91.92 billion. Meanwhile, the state utilities that reported the highest profits were Andhra Pradesh with a profit of Rs 17.36 billion, followed by Haryana at Rs 9.75 billion

Meanwhile, aggregate losses on tariff subsidies received, excluding regulatory income and revenue grants under the Ujwal Discom Assurance Yojana (UDAY) for loan takeover, increased substantially from Rs 137.66 billion in 2021-22 to Rs 671.89 billion in 2022-23.

The gross energy sold by distribution utilities was 1,206.7 BUs in 2022-23, registering a year-on-year increase of 8.68 per cent. The highest energy sales were reported by the states of Maharashtra (131.22 BUs), Uttar Pradesh (108.41 BUs), Gujarat (104.07 BUs) and Tamil Nadu (87.91 BUs).

Revenue from operations, including billed tariff subsidies, increased by 17.84 per cent from Rs 7,430.13 billion in 2021-22 to Rs 8,755.78 billion in 2022-23. The top revenue-earning discoms for 2022-23 were Maharashtra State Electricity Distribution Company Limited (MSEDCL) (Rs 1,129.33 billion), Tamil Nadu Generation and Distribution Corporation (TANGEDCO) (Rs 824 billion), Punjab State Power Corporation Limited (Rs 393.14 billion), West Bengal State Electricity Distribution Company Limited (WBSEDCL) (Rs 315.88 billion) and Telangana State Southern Power Distribution Company Limited (TSSPDCL) (Rs 342.55 billion).

Tariff subsidy billed by distribution utilities increased from Rs 1,444.69 billion in 2021-22 to Rs 1,695.32 billion in 2022-23. As a percentage of total revenue, tariff subsidy billed by the utilities decreased marginally from 17.77 per cent in 2021-22 to 17.53 per cent in 2022-23. Tariff subsidy released by the state governments as a percentage of tariff subsidy billed by distribution utilities continues to be above 100 per cent at 108.08 per cent in 2022-23.

The gap in tariff subsidy billed widened from Rs 0.20 per kWh in 2021-22 to Re 0.39 per kWh in 2022-23. The gap in tariff subsidy received, excluding regulatory income and revenue grant under UDAY for loan takeover, reduced from Re 0.10 per kWh in 2021-22 to Re 0.46 per kWh in 2022-23.

The cash-adjusted gap also fell from Re 0.33 per kWh in 2021-22 to Rs 0.55 per kWh in 2022-23. Receivables for the sale of power (number of days) improved from 138 days as of March 31, 2022, to 119 days as of March 31, 2023.

Payables for the purchase of power (number of days) improved from 168 days as of March 31, 2022, to 128 days as of March 31, 2023. The state utilities with the lowest payables, with 0 days payable for power purchase, were DGVCL, Madhya Gujarat Vij Company Limited (MGVCL), Paschim Gujarat Vij Company Limited (PGVCL), Uttar Gujarat Vij Company Limited (UGVCL) and Kanpur Electricity Supply Company Limited (KESCO).

Distribution utilities’ net worth continues to be negative at Rs 1,447.11 billion as of March 31, 2023. Total borrowings increased from Rs 6,148.53 billion as of March 31, 2022, to Rs 6,843.79 billion as of March 31, 2023.

Performance of generation utilities

As per PFC’s report, the losses of generation utilities increased from Rs 1.01 billion in 2021-22 to Rs 16.88 billion in 2022-23. However, 16 out of 20 generation utilities registered profit in 2022-23. The loss-making gencos were Rajasthan Rajya Vidyut Utpadan Nigam Limited (Rs 62.78 billion), Maharashtra State Power Generation Company (Rs 7.96 billion), Meghalaya Power Generation Corporation Limited (Rs 0.95 billion) and Jharkhand Urja Utpadan Nigam Limited (Rs 0.06 billion).

Net worth for generation utilities decreased from Rs 1,174.95 billion as of March 31, 2022, to Rs 1,072 billion as of March 31, 2023.

Performance of transmission utilities

Performance of transmission utilities

Profit of transmission utilities increased from Rs 38.35 billion in 2021-22 to Rs 55.48 billion in 2022-23. Notably, 16 out of 19 transmission utilities registered profit in 2022-23. The transcos that reported the highest increase in profits over 2021-22 were Gujarat Energy Transmission Corporation Limited (Rs 12.57 billion) Maharashtra State Electricity Transmission Company (Rs 10.37 billion), Karnataka Power Transmission Corporation (Rs 7.23 billion) and Transmission Corporation of Andhra Pradesh (Rs 6.19 billion).

The net worth of transmission utilities increased from Rs 996.8 billion as of March 31, 2022, to Rs 1,019.25 billion as of March 31, 2023.

Performance of trading utilities

Losses of trading utilities increased from Rs 73.72 billion in 2021-22 to Rs 153.05 billion in 2022-23. Uttar Pradesh Power Corporation Limited incurred a loss of Rs 145.72 billion, while the Grid Corporation of Odisha incurred a loss of Rs 7.78 billion in 2022-23.

Net worth of trading utilities decreased from Rs 765.98 billion as of March 31, 2022, to Rs 727.58 billion as of March 31, 2023.

Conclusion

PFC’s comprehensive report is a government initiative to shed light on the health of the power sector. In March 2024, it released the 12th edition of the annual integrated ratings of discoms as well.

Net, net, as the PFC report shows, state-owned power utilities are facing challenges in improving financial and operational performance, particularly distribution utilities. Despite increased energy sales and revenue, there has been a significant rise in aggregate losses, driven partly by escalating tariff subsidies. Addressing these challenges will require comprehensive strategies to manage debt levels, optimise revenue streams and enhance operational efficiency across all segments of the power sector.