India’s transmission network is expanding rapidly to meet the country’s increasing power demand and align with the growing power generation capacity. In recent years, this expansion has been characterised not only by the physical growth of the transmission network, but also by the adoption of higher transmission voltages and advanced technologies for bulk power transmission.

Furthermore, there is a growing emphasis on transmission network planning and operations to enhance grid resilience and flexibility. The expansion of the transmission system is crucial for addressing the country’s rising electricity demand and facilitating the integration of renewable energy sources. A robust transmission infrastructure is critical for efficiently transmitting power over long distances, maintaining grid stability and ensuring an uninterrupted electricity supply.

Size and growth

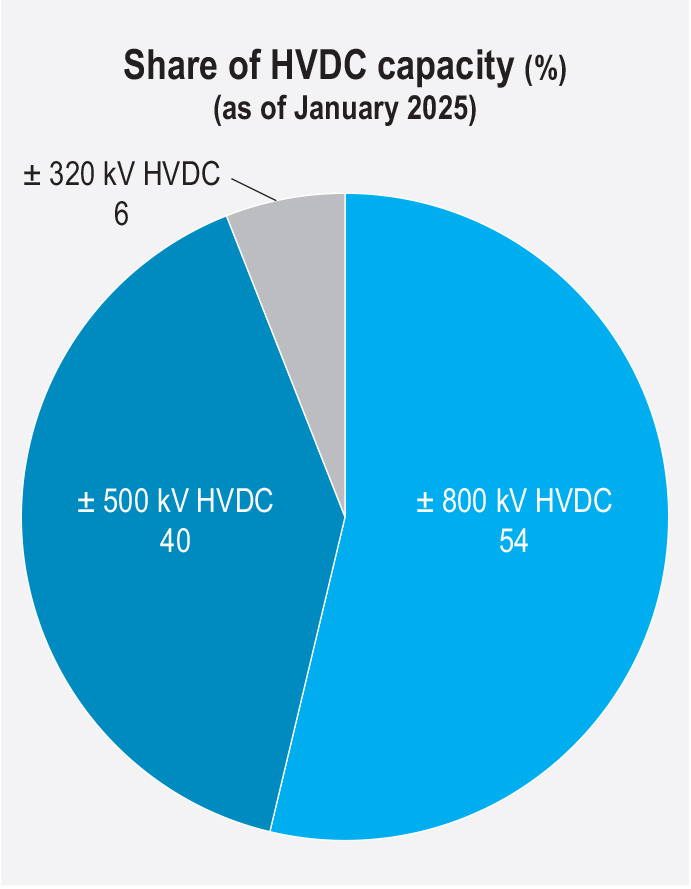

As of January 2025, the total length of transmission lines at the 220 kV and above levels stood at 491,871 ckt km, comprising 56,333 ckt km at the 765 kV level, 206,182 ckt km at the 400 kV level and 209,981 ckt km at the 230/220 kV level. At the high voltage direct current (HVDC) level, line length stood at 9,655 ckt km at the ±800 kV level, 9,432 ckt km at the ±500 kV level and 288 ckt km at the ± 320 kV level.

The total transmission line capacity addition during 2023-24 was 14,203 ckt km. In 2024-25, as of January 2025, 6,327 ckt km of line length has been added.

Further, the country’s total interregional capacity stood at 118,740 MW as of January 2025. Meanwhile, the total transformation capacity stood at 1,269 GVA, comprising 306,700 MVA at the 765 kV level, 481,213 MVA at the 400 kV level and 481,167 MVA at the 230/220 kV level. HVDC capacity currently stands at 18,000 MW at the ±800 kV level, 13,500 MW at the ±500 kV level and 2,000 MW at the ±320 kV level. The total transformation capacity addition during 2023-24 was 70,728 MVA, while for 2024-25, it stood at 51,500 MVA as of January 2025.

In order to fast-track the development of the country’s transmission network, tariff-based competitive bidding (TBCB) was introduced in 2006. As of January 2025, 135 interstate transmission system (ISTS) projects have been bid out to public and private players since 2009 under the TBCB mechanism. Of these, 60 projects have been commissioned. In terms of player-wise allocations, 61 projects were secured by Power Grid Corporation of India Limited (Powergrid) and 74 by private players. The key private players in the transmission segment are Sterlite Power Transmission Limited, Adani Energy Solutions Limited, IndiGrid, ReNew Transmission Ventures Private Limited, Apraava Energy Private Limited, Resurgent Power, Sekura Energy, G R Infraprojects as well as recent entrants including Techno Electric, Reliance Industries Limited and DRAIPL.

Emerging trends

Transmission utilities are increasingly adopting predictive maintenance strategies, and leveraging data analytics to assess equipment health and make proactive, informed decisions. Advanced technology solutions, such as drones equipped with thermal imaging, high resolution video and corona cameras, are being deployed for real-time monitoring of transmission lines, substations and reactors. These tools enable utilities to detect grid vulnerabilities swiftly and efficiently, offering a faster, more cost-effective alternative to traditional ground-based inspections.

Aerial surveillance and remote inspection technologies are now being integrated with artificial intelligence (AI) to develop intelligent digital twins–accurate digital replicas of transmission lines and towers that enhance maintenance and record-keeping. For instance, Powergrid has introduced digital applications, such as PG DARPAN, for routine patrolling and network assessments, enabling real-time monitoring to improve patrol efficiency, geographical mapping, automated reporting, defect cataloguing, rectification tracking, and resource planning. Another initiative, Asset Management through AI in Transmission, utilises image processing to identify over 30 types of defects with more than 95 per cent accuracy.

To support the reliable integration of renewable energy, renewable energy management centres (REMCs) have been set up at both state and national levels. The REMCs are strategically co-located with load despatch centres across various regions. A total of 11 REMCs have been established at locations including the National Load Despatch Centre in Delhi, the Northern Regional Load Despatch Centre in Delhi, and state-level centres in Andhra Pradesh, Gujarat, Rajasthan, Maharashtra, Karnataka and Tamil Nadu. Additionally, regional centres have been set up at WRLDC in Mumbai and SRLDC in Bengaluru. Currently, these REMCs oversee 62.5 GW of renewable energy capacity, monitoring data from 654 pooling stations across India. Their responsibilities include forecasting renewable generation, handling imbalances, and scheduling power from solar and wind plants. Furthermore, they provide real-time situational awareness, enabling better decision-making for grid operators.

Transmission expansion plans

Transmission expansion plans

In October 2024, the Central Electricity Authority released the National Electricity Plan (NEP) – Transmission, outlining the transmission network requirements up to 2031-32. The NEP projects an investment of over Rs 9 trillion during 2022-32 in inter and intra-state transmission networks. The plan aligns with the revised (draft) Electric Power Survey, which projects a peak demand of 296 GW by 2026-27 and 388 GW by 2031-32.

As per the NEP, during the 2022-27 period, almost 114,687 ckt km of transmission lines and 776,330 MVA of transformation capacity will be added at an investment of Rs 4,252.22 billion. In the subsequent period, 2027-32, the addition of 76,787 ckt km of transmission lines and 497,855 MVA of transformation capacity are expected at an investment of Rs 4,909.2 billion.

In addition, 1,000 MW of HVDC bipole capacity is expected to be added during the 2022-27 period while almost 32,250 MW is expected to be added during 2027-32. By the end of 2031-32, the total transmission line length is estimated to reach 648,190 ckt km, with a transformation capacity of 2,345,135 MVA. Furthermore, HVDC bipole capacity, including back-to-back systems, is expected to increase to 66,750 MW by the end of 2031-32.

The planned addition of interregional transmission capacity during 2022-27 is 30,690 MW. Several interregional transmission corridors are planned for this period, with 24,600 MW of interregional transmission capacity expected to be added. This expansion will increase the total interregional transmission capacity to approximately 167,540 MW by the end of 2031-32.

Significant plans are also under way for evacuating green power. Under the Green Energy corridor (GEC) scheme, Phase I of the ISTS was completed in 2020, enabling the evacuation of 6 GW of renewable energy. Intra-state transmission systems (InSTS) are under implementation in eight renewable-rich states – Andhra Pradesh, Gujarat, Himachal Pradesh, Karnataka, Madhya Pradesh, Maharashtra, Rajasthan and Tamil Nadu – connecting 18.72 GW of renewable energy to the grid. While most of the projects are nearing completion, some states have been granted extensions until 2024-25 due to delays in land acquisition and clearances. The InSTS GEC-II scheme aims to add 10,750 ckt km of intra-state transmission lines and 27,500 MVA of substations, with an outlay of Rs 120.31 billion. The GEC-II transmission schemes will be implemented by seven states – Gujarat, Himachal Pradesh, Karnataka, Kerala, Rajasthan, Tamil Nadu and Uttar Pradesh – for the evacuation of approximately 20 GW of renewable energy. Currently, the state transmission utilities are preparing the packages and are in the process of issuing tenders for implementing the projects. The scheduled commissioning for projects under Phase II is March 2026.

Also, as per initial estimates by the Ministry of New and Renewable Energy (MNRE), additional electricity demand from green hydrogen/green ammonia production is projected to reach 70.5 GW by 2031-32. The planned transmission system will be implemented in a phased manner, in line with the development of green hydrogen/green ammonia manufacturing hubs.

The electricity demand of the Andaman & Nicobar Islands is mainly met through diesel generator sets, supplemented by small-scale renewable energy sources such as solar and wind power. As per the NEP, the Andaman & Nicobar Islands are planned to be connected to the mainland via HVDC undersea cables. This ±320 kV, 250 MW HVDC (VSC-based) interconnection, spanning 1,150 km, will be the first of its kind in the country. The estimated cost of this transmission project is approximately Rs 151.2 billion. This interconnection aims to help the islands’ transition to green energy by 2028-29.

Issues and challenges

India’s power transmission sector faces several challenges that impact its growth. Right-of-way constraints and land acquisition hurdles remain key bottlenecks, causing project delays and cost escalations. Acquiring land for transmission corridors is a complex and time-consuming process, often met with resistance from local communities and environmental concerns.

Further, the huge renewable energy capacity addition presents significant challenges. Low gestation period of renewables vis-à-vis transmission is a key challenge. Long UHV/EHV lines are needed to evacuate bulk intermittent/variable power to the grid.

To address the variability of renewable energy sources, various technology initiatives are being taken such as the deployment of VSC-based HVDC, storage and FACTS devices, and synchronous condensers.

There is also a strong focus on the development and integration of energy storage devices, including batteries and pumped hydro, into the grid. To incorporate the latest international best practices in transmission planning, the CEA has updated and released the Manual on Transmission

Planning Criteria.

Addressing these challenges is crucial to ensuring a reliable and efficient transmission network, which is essential for meeting India’s growing energy needs and facilitating its transition to clean energy sources.

Ambitious plans are shaping the future of the sector, with significant capital investments allocated to expanding transmission infrastructure and improving interconnectivity. Moving forward, these efforts aim to strengthen India’s energy resilience, support the seamless integration of renewable energy, and drive India toward a sustainable energy future.

Akanksha Chandrakar