India’s power trading segment has witnessed significant expansion, driven by increasing demand, technological advancements and policy reforms. The market has evolved over time, providing enhanced liquidity and greater flexibility for participants. The rise of real-time markets, green energy trading, and ancillary services has further strengthened the segment, supporting grid stability and renewable energy integration.

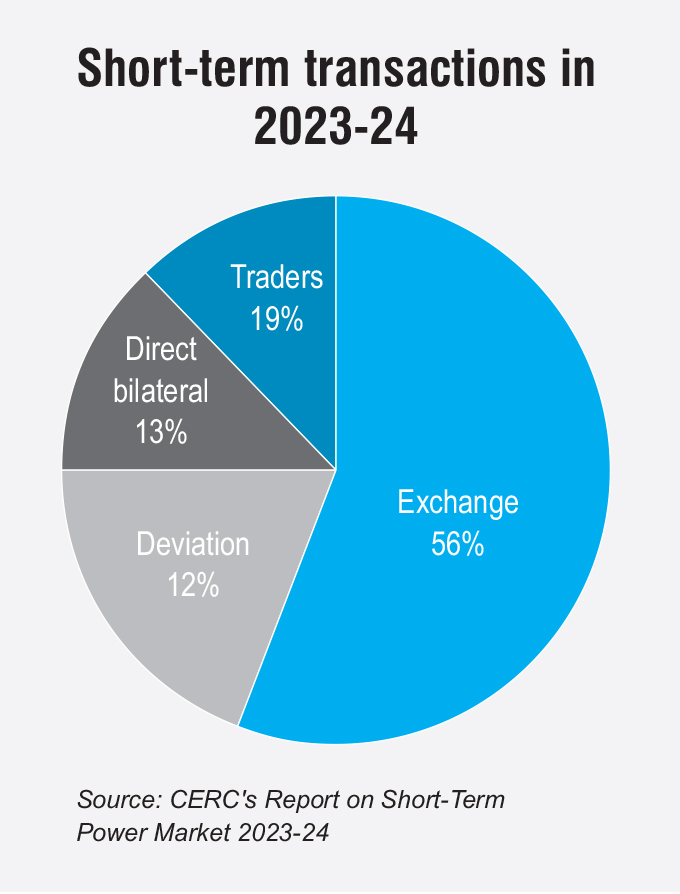

The total short-term electricity and deviation settlement mechanism (DSM) volume grew from 65.90 BUs during 2009-10 to a record high of 218.22 BUs during 2023-24. During this period, short-term electricity transactions expanded at a compound annual growth rate (CAGR) of 8.9 per cent, outpacing the total electricity generation growth rate of 6.0 per cent. The share of short-term transactions in the total electricity generation ranged between 8.9 per cent and 12.5 per cent.

The market size for bilateral trading (via traders) and power exchanges surged from Rs 1,762.2 billion during 2009-10 to Rs 10,072.9 billion during 2023-24, reflecting a CAGR of 13.3 per cent.

Power exchange segments and DSM

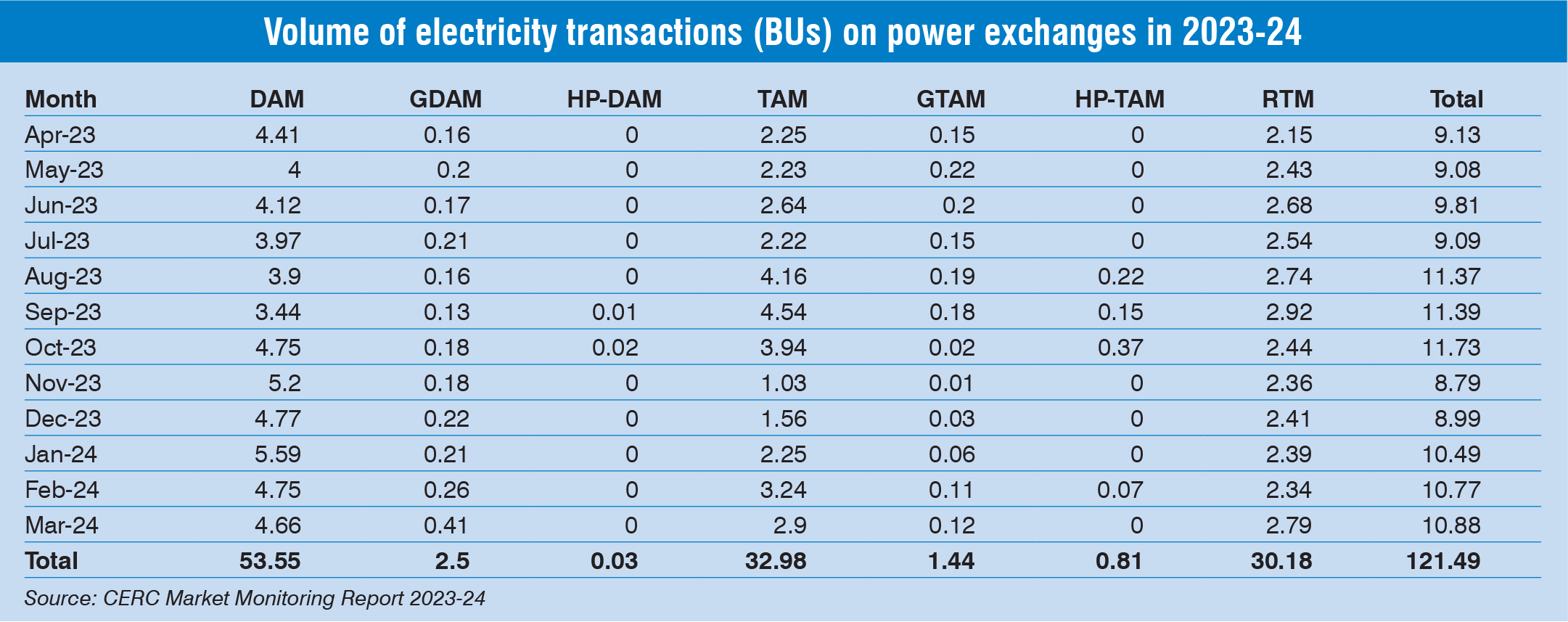

The volume of electricity transacted across all three power exchanges under various market segments grew from 7.19 BUs during 2009-10 to 121.49 BUs during 2023-24, registering a CAGR of 22.4 per cent. The share of electricity traded through power exchanges, as a percentage of the total volume of short-term transactions of electricity and DSM, increased from approximately 10.9 per cent during 2009-10 to 55.7 per cent during 2023-24.

During 2023-24, the weighted average price of electricity transacted through power exchanges stood at Rs 5.82 per kWh, while the price through trading licensees was Rs 7.33 per kWh. In comparison, the corresponding values during 2022-23 were Rs 6.25 per kWh and Rs 5.85 per kWh respectively.

The DSM volume recorded a 1.86 per cent increase in 2023-24 compared to the previous year. However, its share as a percentage of the total volume of short-term transactions of electricity and DSM continued to decline, falling from 39.2 per cent in 2009-10 to 12.3 per cent in 2023-24. Additionally, the DSM charge rose from Rs 5.39 per kWh in 2022-23 to Rs 5.73 per kWh in 2023-24.

Direct bilateral transactions between entities declined by approximately 7.6 per cent in volume in 2023-24 compared to 2022-23. However, their share as a percentage of the total short-term transactions and DSM volume increased from 9.4 per cent in 2009-10 to 13.3 per cent in 2023-24.

During 2023-24, transmission congestion had minimal impact on electricity transactions through power exchanges. The actual transacted volume was about 0.10 per cent lower than the unconstrained volume. Due to instances of congestion and market splitting, the total congestion amount collected during the year was Rs 25.20 billion. The unconstrained cleared volume and the actual transacted volume increased from 8.10 BUs and 7.09 BUs, respectively, during 2009-10 to 86.35 BUs and 86.26 BUs, respectively, during 2023-24.

Segment-wise trading

In the day-ahead market (DAM), a total volume of 53.55 BUs was transacted across the three power exchange platforms during 2023-24, an increase of 4.26 per cent over the previous year. The IEX accounted for a major share in DAM, with a trading volume of 53.38 BUs, while PXIL accounted for 0.079 BUs and HPX accounted for the remaining volume.

The real-time market (RTM) saw an increase in the volume transacted during 2023-24, growing to 30.18 BUs from 24.18 BUs during 2022-23, an increase of 24.81 per cent. The IEX accounted for a major share in RTM, with a trading volume of 30.12 BUs, while PXIL accounted for 0.027 BUs and HPX accounted for 0.026 BUs.

The term-ahead market (TAM) recorded a volume of 32.98 BUs in 2023-24, an increase of 53.32 per cent compared to 21.51 BUs in 2022-23. In the green TAM, an aggregate volume of 1.44 BUs was transacted during 2023-24 across the three power exchange platforms compared to 2.56 BUs in 2022-23.

The green day-ahead market (GDAM) witnessed a total transaction volume of 2.50 BUs traded on the IEX, while no transactions took place on PXIL and HPX. The total volume of electricity transacted in power exchanges under the GDAM during 2022-23 was 3.817 BUs.

During 2023-24, a total volume of 1.44 BUs was transacted in the GTAM on the three power exchange platforms, a 65.63 per cent decrease over the aggregate volume of 4.19 BUs transacted in the previous year.

Traders

Traders

The volume of electricity transacted through traders grew from 26.72 BUs in 2009-10 to 41.02 BUs in 2023-24, at a CAGR of 3.1 per cent. The share of electricity transacted through traders as a percentage of the total short-term transactions and DSM volume decreased from 40.5 per cent during 2009-10 to 18.8 per cent during 2023-24.

In 2023-24, 4 per cent of the trader transactions occurred at prices below Rs 5 per kWh, while 91 per cent were below Rs 9 per kWh. Of the total electricity procured through bilateral transactions, 85.8 per cent was on a round-the-clock (RTC) basis, 13.9 per cent in off-peak periods, and 0.4 per cent during peak hours. Peak-hour electricity was the most expensive at Rs 9.62 per kWh, compared to Rs 7.37 per kWh for RTC and Rs 7.23 per kWh for off-peak periods. The weighted average trading margin in 2023-24 was ₹0.029 per kWh, aligning with the CERC Trading License Regulations, 2020.

The number of active traders increased from 15 in 2008-09 to 39 in 2023-24. The Herfindahl-Hirschman Index (HHI) for the trader-based short-term transactions rose from 0.1630 to 0.1721, indicating a moderate market concentration. In 2023-24, the top five traders by market share were PTC India Limited (32.66 per cent), NTPC Vidyut Vyapar Nigam Limited (17.21 per cent), Adani Enterprises Limited (11.03 per cent), Tata Power Trading Company Limited (10.30 per cent), and Arunachal Pradesh Power Corporation Private Limited (7.54 per cent).

Trading in certificates

In 2023-24, a total of 13.85 million renewable energy certificates (RECs) were traded on the power exchanges and through trading licensees. With the introduction of new regulations in 2022, the distinction between solar and non-solar RECs has been removed, and a multiplier-based system has been introduced. A new “REC” contract was made available for trading on the power exchanges from December 2022, and transactions through trading licensees were also permitted.

The market clearing volume of RECs saw a significant rise from 2.63 million in 2022-23 (December 2022 to March 2023) to 11.66 million in 2023-24. The market clearing price of these RECs dropped from Rs 1,000 per MWh to Rs 442 per MWh during the same period.

Similarly, the volume of RECs transacted through trading licensees surged from 0.09 million in 2022-23 to 2.19 million in 2023-24, while the weighted average price declined from Rs 925 per MWh to Rs 452 per MWh.

Open access consumer participation

In power exchanges, open access industrial consumers procured 11.03 BUs of electricity through collective transactions, accounting for 12.8 per cent of the total volume transacted across the DAM, GDAM, HP-DAM and RTM during 2023-24. The number of open access (OA) consumers at both the IEX and PXIL witnessed substantial growth, increasing from 825 and 170, respectively, in 2010-11, to 5,244 and 825 in 2023-24. At HPX, which commenced operations in July 2022, the number of OA consumers rose from 239 in 2022-23 to 265 in 2023-24.

Regarding electricity prices, the weighted average price of electricity procured by OA consumers at the IEX stood at Rs 3.76 per kWh, lower than the overall weighted average price of electricity transacted through IEX (Rs 5.10 per kWh). Similarly, at PXIL, OA consumers paid a weighted average price of Rs 7.39 per kWh, lower than the overall market price of Rs 10.23 per kWh during 2023-24. At HPX, the weighted average price of electricity purchased by OA consumers was Rs 10.00 per kWh, slightly exceeding the overall market price of Rs 9.98 per kWh during 2022-23.

Cross-border trade

Cross-border trade

India imports electricity from Bhutan and exports power to Bangladesh, Nepal and Myanmar. While the country was a net importer of electricity from 2013-14 to 2015-16, it has remained a net exporter since 2016-17. Cross-border electricity trade in the DAM at the IEX commenced in 2021-22, with Nepal joining on April 17, 2021, followed by Bhutan on January 1, 2022. Additionally, cross-border trade in the RTM at the IEX began in October 2023.

In July 2023, the Central Electricity Authority (CEA) introduced amendments to facilitate cross-border power transfers through the RTM segment of Indian power exchanges. Under this amendment, Indian power traders can trade on behalf of entities from neighbouring countries in the DAM, RTM, or both, subject to approval from the designated authority. This is permitted up to a specified quantum (MW) and duration, provided the entity belongs to a country that has signed a power sector cooperation agreement with India and the generating asset being traded is owned or controlled by that country.

As per POSOCO’s cross-border trading data for 2024-25 (till February 2025), India imported electricity from Bhutan and Nepal, with net imports of 5,325.83 MUs and 2,131.41 MUs respectively. Conversely, India is a net exporter of electricity to Bangladesh, exporting 7,385.92 MUs. Similarly, India exports a small amount of electricity to Myanmar, totalling 8.36 MUs, with no imports.

Recent developments

Recent developments

In November 2024, the amendments to the Late Payment Surcharge and Related Matters Rules, 2022, were issued to strengthen payment security through letters of credit, escrow accounts, and advance payments, ensuring power scheduling only upon the clearance of dues. These amendments also regulate un-requisitioned surplus power, mandating its sale in the DAM and RTM before fixed charge recovery.

In the same month, in a key step towards carbon markets, the CERC issued the draft CERC (Terms and Conditions for Purchase and Sale of Carbon Credit Certificates) Regulations, 2024. As per the draft, the Bureau of Energy Efficiency will administer carbon credit certificates (CCCs) and ensure compliance, while the Grid Controller of India will manage the registry. The CCCs will be traded in compliance and offset markets, with power exchanges requiring approval from the CERC.

In January 2025, the CERC issued the draft CERC (Cross Border Trade of Electricity) (Second Amendment) Regulations, 2024, under the Electricity Act, 2003. The draft introduced key amendments to the 2019 regulations to streamline processes, in alignment with the general network access (GNA) principles for cross-border electricity trade.

In October 2024, the CERC issued a draft order addressing price discovery concerns in the day-ahead contingency (DAC) contracts and anomalies in the term-ahead market (TAM) operations. The key proposals included streamlining TAM contracts to prevent market fragmentation, shifting DAC price discovery from continuous matching to an auction model, and withdrawing intra-day contracts due to low liquidity. The Central Electricity Authority (CEA) has further recommended optimising TAM trading windows and enhancing DAC transparency to improve market competitiveness.

Outlook

The country’s power demand rose 6.75 per cent year-on-year in February, marking a sharp rebound from recent sluggish growth. The average tariffs in the DAM of the IEX remained steady at Rs 4.4 per unit in March 2025, maintaining the same level seen in January and February 2025. However, the spot power tariffs are expected to increase over the next few months amid the expected growth in electricity demand with the onset of the summer season and are anticipated to remain in the range of Rs 4.5 per unit to Rs 5.0 per unit in FY2026, with the recovery in demand growth to 5.5 to 6.0 per cent, as per ICRA.

India aims to improve the RTM to support its renewable energy targets. A key development in this effort is the proposed introduction of the green RTM, a platform for real-time trading of renewable energy. By enabling efficient balancing of renewable energy generation with demand, the green RTM will help stabilise the grid and facilitate the transition to a sustainable energy future.

The power trading segment in India is witnessing strong growth, but challenges such as price volatility, discom financial instability and transmission constraints persist. Addressing these issues requires better grid infrastructure, stricter payment discipline, and regulatory support to ensure market stability. The rise of distributed energy resources, including rooftop solar, battery storage, and virtual power plants, will enhance market liquidity and flexibility.

Aastha Sharma