India’s green ammonia market has been buzzing with activity since the launch of the National Green Hydrogen Mission. The government-led initiative has rapidly gained significant momentum, attracting strong industry interest and catering to stakeholder expectations for clearer policies, faster scale-up and greater market stability. This growing enthusiasm has positioned the sector as one of the most dynamic to watch, driven by the launch of tenders, and the introduction of new guidelines and incentives.

Building on this momentum, the past month has seen several policy milestones. Most notably, the Solar Energy Corporation of India (SECI) announced the winners of its Mode-2A, Tranche I green ammonia auction. In total, 13 green ammonia projects were awarded under this tender, collectively targeting a capacity of 724,000 tonnes per annum (tpa) to be supplied to fertiliser plants. The auction design provides much-needed market certainty to producers through 10-year contracts, supported by production-linked incentives of Rs 8.82 per kg in the first year, which will be reduced to Rs 7.06 per kg and Rs 5.30 per kg in the subsequent two years.

Auctions at a glance: ACME’s dominance, competitive tariffs and a distributed demand ecosystem

The table and graphs summarise the key recent auctions. As shown in the table, several companies secured capacities to supply green ammonia to fertiliser manufacturers across India. Suryam International will supply 4,000 tpa of green ammonia to Madras Fertilisers in Chennai, Tamil Nadu. The capacity was secured at a tariff of Rs 50 per kg. Jakson Green won 85,000 tpa at Rs 50.75 per kg, which will be supplied to Coromandel International Limited (CIL) in Kakinada, Andhra Pradesh. Onix Renewable will supply 50,000 tpa of green ammonia to Gujarat Narmada Valley Fertilizers and Chemicals in Bharuch, Gujarat. The capacity was secured a tariff of Rs 52.50 per kg.

Oriana Power quoted Rs 52.25 per kg to secure 60,000 tpa, which will be supplied to Madhya Bharat Agro Products in Sagar, Madhya Pradesh. NTPC also secured 70,000 tpa at Rs 51.80 per kg, with supply directed to Krishana Phoschem in Meghnagar. In Karnataka, the consortium of SCC Infrastructure and InSolare Energy will supply 15,000 tpa to Mangalore Chemicals and Fertilisers. The capacity was secured a tariff of Rs 57.65 per kg. The consortium secured an additional 70,000 tpa at Rs 53.05 per kg, which will be supplied to Madhya Bharat Agro Products in Dhule, Maharashtra.

ACME Cleantech Solutions Private Limited emerged as the biggest winner across multiple lots. It won 100,000 tpa at a tariff of Rs 54.73 per kg, which will be supplied to Indian Farmers Fertiliser Cooperative Limited (IFFCO), Kandla, Gujarat. It also won 100,000 tpa at a bid of Rs 49.75 per kg for supply to IFFCO Paradeep, and 75,000 tpa at Rs 55.75 per kg for Paradeep Phosphates Limited in Odisha. In addition, it secured 50,000 tpa at Rs 51.89 per kg for supply to CIL in Visakhapatnam, Andhra Pradesh; 25,000 tpa at Rs 62.84 per kg to Paradeep Phosphates in Zuarinagar, Goa; and 20,000 tpa at Rs 64.74 per kg for Indorama India Private Limited in Haldia, West Bengal.

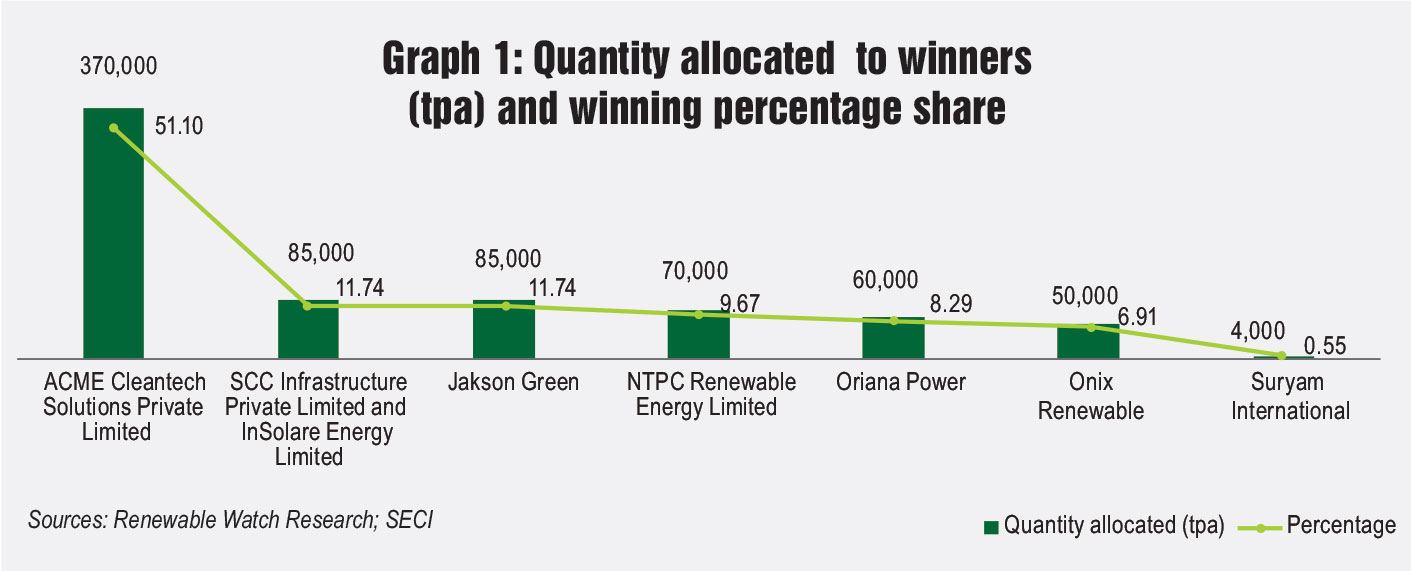

ACME has won the highest cumulative capacity, winning 370,000 tpa across six different auctions (Graph 1). It accounts for more than half of the entire allocation (51.1 per cent). The next largest players are Jakson Green (winning 85,000 tpa) and a joint venture of SCC Infrastructure and InSolare Energy (a total capacity of 85,000 tpa across two auctions). Each winner accounts for 11.7 per cent of the entire allocation. Other winners include NTPC Renewable Energy Limited (9.7 per cent), Oriana Power (8.2 per cent), Onix Renewable Limited (6.9 per cent) and Suryam International (0.6 per cent).

The auction results revealed a wide tariff band, ranging from Rs 49.75 per kg to Rs 64.74 per kg (see graph 2). Notably, ACME secured both the lowest and highest tariffs across the auctions. The company won a landmark bid to supply 100,000 TPA of green ammonia to IFFCO at Paradeep, Odisha, at the lowest discovered tariff of Rs 49.75 per kg. While, ACME also won the auction to supply 20,000 TPA of green ammonia to Indorama India Private Limited in Haldia, West Bengal, at the highest tariff of Rs 64.74 per kg.

In terms of supply volumes, ACME will deliver the largest annual quantity – 100,000 tpa of green ammonia each to IFFCO’s plants in Paradeep and Kandla. Meanwhile, Suryam International will supply the smallest annual quantity – 4,000 tpa – to Madras Fertilisers Limited in Chennai.

Overall, the auctions highlight a few key trends. The first is market concentration, with ACME emerging as the dominant player, but with growing participation by other developers. The second is tariff diversity, reflecting differences in technology costs, logistics, geography and project sizes. The third is demand readiness, with fertiliser companies laying the foundation for large-scale offtake. Moreover, the projects are geographically spread across India’s key fertiliser hubs, highlighting the push to create a distributed green ammonia ecosystem aligned with regional demand centres.

From price discovery to global leadership: Green ammonia auctions set new benchmarks, strengthen supply security, unlock hydrogen-linked growth and export potential

The success of these consecutive auctions highlights India’s growing price competitiveness in the global green ammonia space and reflects industry confidence in the Indian green ammonia market. The record low prices have reignited momentum in the green ammonia sector. This has been made possible by India’s exceptionally low renewable energy costs and supportive regulatory framework. Beyond cost advantages, these price gains have clear strategic implications.

Global price benchmarking: The lowest price discovered in the auction, Rs 49.75 per kg, is around 12 per cent higher (assuming an average exchange rate of Rs 86) than the current grey ammonia prices in India ($515 per mt, or Rs 44.29 per kg). Equally notable is the comparison with global trends: the Mode 2A discovery is nearly half the tariff seen in H2Global’s green ammonia auction in 2024, which closed at Rs 100.28 per kg ($1,153 per mt). By delivering such cost competitiveness, India has effectively set a new global benchmark in green ammonia pricing, strengthening its position as an early mover in shaping the market.

Supply security implications: As per the Central Electricity Authority’s report, titled “Economic Feasibility of Green Ammonia Use in India’s Fertiliser Sector”, released in November 2024, India consumes around 6.3 million metric tonnes per annum (mmtpa) of embedded ammonia and around 2.3 mmtpa of direct imports. Hence, the 724,000 tpa secured through these auctions covers roughly 31.5 per cent of the direct import shortfall and about 8.4 per cent of the broader import-dependent requirement. By replacing imported volumes with domestically produced renewables-based ammonia, the country can cut carbon intensity, reduce foreign exchange outflows, and protect itself from global price shocks and geopolitical risks. While these auctions were designed for the fertiliser sector, their success can be replicated in refineries, steel and other hard-to-abate industries.

Hydrogen linkages and renewable demand: Green ammonia production has a direct multiplier effect on India’s green hydrogen ecosystem as hydrogen is the key feedstock for ammonia. As highlighted in a report by Bloomberg NEF, producing 1 tonne of ammonia requires around 0.176 tonnes of hydrogen. This means that the 724,000 tonnes of green ammonia contracted through the recent auctions will demand roughly 127,400 tonnes of green hydrogen every year. Meeting this demand will, in turn, drive additional renewable power demand, creating a strong case for accelerated renewable capacity deployment. Importantly, the green ammonia produced will displace conventional grey ammonia, which relies on natural gas, thereby reducing both carbon emissions and import dependence.

Export opportunities: India’s competitive pricing also enhances its potential as an export hub, particularly for Europe, Japan and South Korea – markets where demand for low-carbon ammonia is expected to surge. Compliance with the European Union’s carbon border adjustment mechanism could further enhance the competitiveness of Indian exports.

Beyond price discovery: India’s green ammonia success hinges on execution, scalability and long-term sustainability

While the auction results mark an important milestone in India’s green ammonia journey, the headline numbers tell only part of the story. Fertilisers in India are heavily subsidised, which means the government, rather than farmers, will bear most of the additional cost of shifting from grey to green ammonia. Moreover, these low tariffs have been possible largely because subsidies are helping developers cut costs. Additionally, these projects are at a nascent stage, and their ability to deliver at scale remains untested. The real challenge for India, therefore, is not just about achieving record bids but ensuring that these projects are built and operated efficiently, and remain financially sustainable in the long run.

Overall, while the discovered price is attractive, the total allocated volume of 724,000 tpa remains modest compared to India’s overall ammonia demand of 25.5 mmtpa. According to CEEW’s estimates, this includes 17-19 mmtpa of ammonia for the production of fertilisers such as urea, diammonium phosphate and other complex fertilisers. India also indirectly consumes ammonia embedded in fertiliser imports, estimated at 6.3 mmt in 2022-23.

This underlines the need to rapidly scale up in future tranches. Going forward, India must shift its focus from price discovery to rapid execution. This includes fast-tracking financial closures, renewable tie-ups and development of infrastructure such as pipelines, storage hubs and port facilities. Equally important is securing long-term demand through fertiliser offtake agreements, blending mandates, and adoption in sectors such as shipping and steel. On the policy side, low-cost financing, carbon credit integration and fiscal incentives will strengthen project viability. Parallel investments in electrolyser manufacturing and research and development can further reduce costs.

Net, net, while the policy momentum is encouraging, the real test will lie in how quickly India can translate these ambitious bids into operational projects at scale. If executed well, India could not only achieve self-reliance in ammonia but also emerge as a global hub for green ammonia exports.