India’s power generation sector has undergone remarkable growth and transformation over the past decade, driven by sustained policy interventions, rapid renewable energy adoption and continued reliance on conventional sources. As of July 2025, the country’s installed generation capacity stood at nearly 490 GW, with coal and lignite maintaining the largest share, while solar and wind have emerged as key contributors to the energy mix. The segment has diversified in fuel sources, while also recording steady capacity additions, with renewables growing at double-digit rates. At the same time, generation performance has been shaped by fluctuating demand, evolving fuel economics and regulatory shifts. Recent policy measures, such as GST rationalisation, revised emission norms and the launch of the Nuclear Energy Mission, underscore the government’s intent to balance sustainability with energy security.

An overview of the country’s power generation segment…

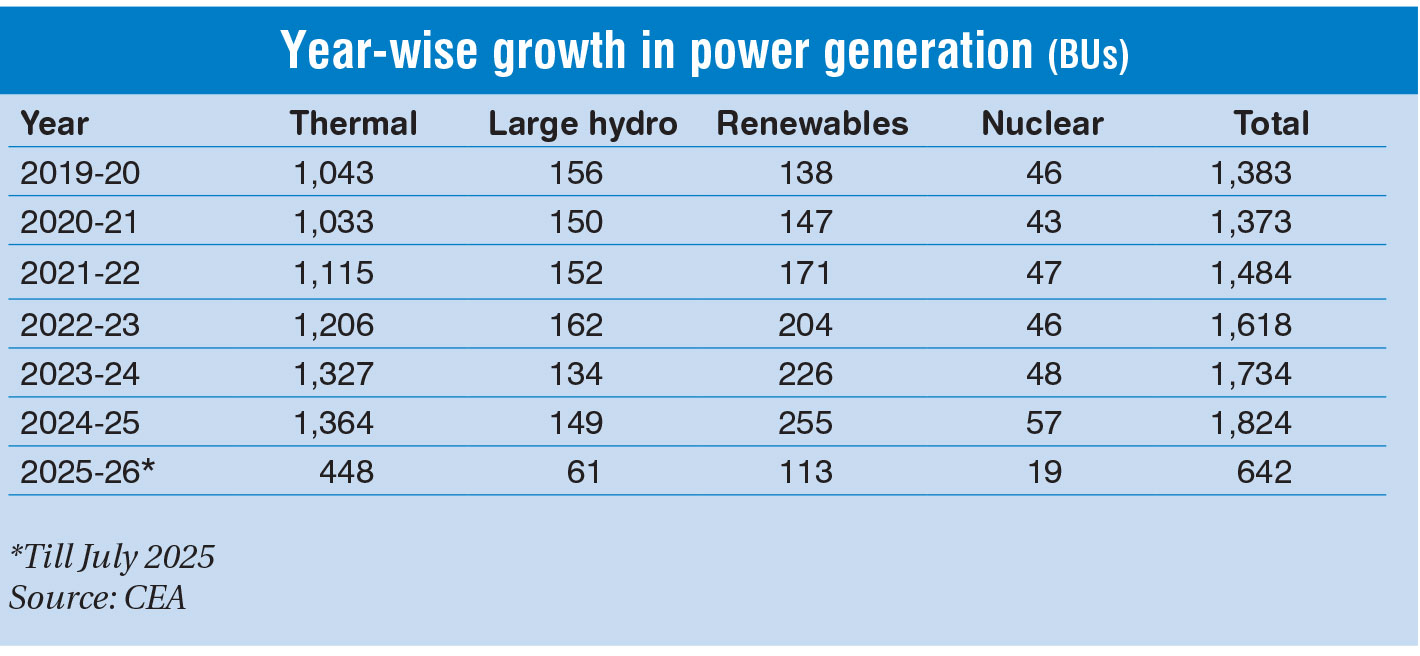

Segment growth and performance

As of July 2025, India’s total installed power capacity stood at 490 GW. Fuel-wise, coal- and lignite-based power had the highest share at 45.5 per cent, followed by solar at 24.3 per cent. Wind contributed 10.6 per cent of the capacity, followed by large hydro at 10.1 per cent, gas at 4.1 per cent, bioenergy at 2.4 per cent, nuclear at 1.8 per cent, small-hydro at 1 per cent, and diesel for the remaining 0.1 per cent. The share of renewables reached nearly 48.5 per cent, with the inclusion of large hydro (49,628.16 MW).

The installed capacity grew at a CAGR of 4.83 per cent between 2018-19 and 2024-25. While conventional power capacity has grown at a CAGR of 0.99 per cent over the past five years, renewable energy has grown at a CAGR of 10.47 per cent. In absolute terms, around 33,398.66 MW of net capacity was added in 2024-25, of which 3,875 MW was based on thermal power sources, 28,723.67 MW on renewables (including small hydro) and 799.99 MW on large hydro.

Meanwhile, the total recorded generation (including renewable energy sources) stood at 1,829 BUs in 2024-25, recording an increase of 5.2 per cent compared to 1,739 BUs in 2023-24. Renewable energy generation during 2024-25 (including large hydro) was around 403 BUs. In terms of fuel sources, thermal power accounted for the largest share of the generation mix at 75 per cent, followed by renewable sources at 22 per cent and nuclear power at approximately 3 per cent. The total generation grew at a CAGR of 3.93 per cent between 2018-19 and 2024-25. Thermal generation grew at 4.09 per cent and renewable energy generation at 12.36 per cent during this period. During 2025-26 (as of July 2025), total generation has been recorded at 532 BUs, a 4 per cent decline from 556 BUs in 2024-25.

On the operational performance front, the thermal plant load factor (PLF) declined to 69.45 per cent during 2024-25 from 68.74 per cent in 2023-24, led by healthy demand growth over the past four years and limited capacity addition in the coal-based power generation capacity. During 2024-25, the central sector recorded a PLF of 75.32 per cent, while the state sector recorded a PLF of 63.23 per cent. Meanwhile, the thermal PLF decreased from 67.72 per cent in July 2024 to 62.69 per cent in July 2025. In July 2025, the PLF of gas-based plants stood at 17 per cent.  Policy and regulatory developments

Policy and regulatory developments

Recently, in September 2025, the GST Council restructured rates to increase coal levy and reduce taxes on renewables. Coal, lignite and peat will now be taxed at 18 per cent, up from 5 per cent earlier. The GST rate on renewable energy devices and hydrogen-based technologies has been reduced to 5 per cent from 12 per cent. Additionally, the council has eliminated the Rs 400 per tonne compensation cess previously levied on coal. The capital cost of utility-scale solar projects, typically around Rs 35 million-Rs 40 million per MW, will now reduce by Rs 2 million-Rs 2.5 million per MW, while also lowering tariffs and easing the financial burden on discoms. Households and farmers will also benefit, with rooftop solar systems and solar pumps becoming cheaper.

In July 2025, the Ministry of Environment, Forest and Climate Change amended the flue gas desulphurisation norms for coal and lignite-based thermal plants. Units in and around the National Capital Region and large urban centres (Category A) must comply by December 2027, while those near critically polluted zones (Category B) have deadlines up to December 2028. Plants outside sensitive regions have been exempted, subject to meeting stack height requirements by December 2029.

In the nuclear sector, the Nuclear Energy Mission was launched under the Union Budget 2025, targeting 100 GW by 2047, anchored on private participation, small modular reactors and domestic manufacturing. In March 2025, Nuclear Power Corporation of India Limited (NPCIL) connected Unit 7 (700 MW) of the Rajasthan Atomic Power Project (RAPP) to the Northern Grid, marking the third 700 MW pressurised heavy water reactor after the Kakrapar Atomic Power Station (KAPS)-3 and KAPS-4. The twin unit, RAPP-8, is expected to be completed in 2025-26.

In May 2025, the Cabinet Committee on Economic Affairs approved the revised SHAKTI policy for granting fresh coal linkages to thermal power plants (TPPs) in the central/state/independent power producer (IPP) sectors. The revised policy highlights two key elements – Window I: coal linkage for central/state power generating stations at the notified price; and Window II: coal linkage for all power generating stations at a premium above the notified price. The amended policy aims to streamline the coal linking process, enable IPPs and private entities to expand thermal power capacity, and remove the requirement for power purchase agreements (PPAs) for electricity generated from coal acquired under Window II.

In April 2025, the Ministry of Power (MoP) proposed draft amendments to the model bidding documents for long-term power procurement from thermal power stations (TPSs) set up on a design-build-finance-operate-own basis, and invited public comments.

Meanwhile, to meet the surge in demand during the summer months, the MoP, under Section 11 of the Electricity Act, 2003, directed the entire gas-based power fleet in the country to be operational from May 26, 2025, to June 30, 2025, to ensure round-the-clock power supply during peak demand and high temperature conditions. A similar notification required imported coal-based power plants to run at full capacity until June 30, 2025.

New contract awards

Recently, several new contracts have been awarded in the thermal power segment. In September 2025, NPCIL awarded a significant order to Larsen & Toubro’s (L&T’s) heavy civil infrastructure vertical for the Kudankulam Nuclear Power Project Units 5 and 6 (2×1,000 MWe) in Tamil Nadu. In April 2025, NPCIL awarded a Rs 130 billion contract to Megha Engineering & Infrastructure Limited for the supply and construction of the 700 MW Kaiga Units 5 and 6 nuclear reactors in Karnataka.

In April 2025, NTPC Limited awarded an order worth Rs 382 million to GE Power India Limited for the supply of generator parts for its Talcher site. In March 2025, NTPC awarded L&T a contract for the supply and installation of the main plant package, including boilers and turbines, for 3×800 MW ultra-supercritical units at Stage-II of the Nabinagar super TPP. In February 2025, NTPC and Madhya Pradesh Power Generating Company Limited (MPPGCL) awarded GE Power a Rs 403.38 million contract for steam turbine parts at Talcher, along with boiler panel services. In November 2024, NTPC issued a “limited notice to proceed” to L&T Energy CarbonLite Solutions for the main plant packages of the 2×800 MW Gadarwara Stage-II and 3×800 MW Nabinagar Stage-II TPPs in Madhya Pradesh and Bihar, respectively.

In February 2025, Damodar Valley Corporation issued a Rs 62 billion letter of intent (LoI) to Bharat Heavy Electricals Limited (BHEL) for the steam generator island package of the 2×660 MW Raghunathpur TPS Phase II in West Bengal. In February 2025, Maharashtra State Power Generation Company Limited issued a letter of award (LoA) worth Rs 80 billion to BHEL for the 2×660 MW Koradi TPS boiler, turbine and generator (BTG) package. In February 2025, Singareni Collieries Company Limited awarded an LoI to BHEL for the engineering, procurement and construction package of the 1×800 MW Singareni TPP Stage-II in Mancherial, Telangana.

In December 2024, MPPGCL awarded GE Power a Rs 182.7 million follow-on order for boiler parts at the Sanjay Gandhi Power Station, extending an October 2024 order worth Rs 209 million. In September 2025, MB Power (Madhya Pradesh) Limited issued a Rs 26 billion LoI to BHEL for supplying BTG equipment for the 1×800 MW Anuppur TPP in Madhya Pradesh. In September 2025, Mahan Energen Limited awarded a Rs 3.71 billion order to Power Mech Projects Limited for the execution of civil works at the 2×800 MW Mahan Phase III project in Singrauli, Madhya Pradesh. In August 2025, Adani Power Limited (APL) awarded an over Rs 150 billion contract to L&T for setting up eight 800 MW thermal power units, totalling 6,400 MW. In December 2024, APL awarded a Rs 5.1 billion contract to Power Mech Projects Limited for mechanical works at the 2×800 MW Raipur Phase II ultra-supercritical TPP in Raikheda, Chhattisgarh.

New PPAs and project announcements

In June 2025, DVC signed a PPA to supply 300 MW of round-the-clock power from its upcoming 2×800 MW Koderma TPP Phase II to Karnataka’s five discoms. In November 2024, DVC signed PPAs with Gujarat Urja Vikas Nigam Limited to supply a total of 559 MW – 359 MW from the 800 MW Durgapur TPP expansion in West Bengal and 200 MW from the 2×800 MW Koderma TPP expansion in Jharkhand.

In September 2025, APL received an additional 800 MW LoA from Madhya Pradesh Power Management Company Limited (MPPMCL) under the greenshoe option for a new ultra-supercritical TPP in Anuppur, Madhya Pradesh, bringing the total awarded capacity to 1,600 MW at Rs 5.838 per kWh, with an investment of around Rs 210 billion. In August 2025, APL announced a 2,400 MW greenfield ultra-supercritical TPP in Bhagalpur, Bihar, under an LoI from Bihar State Power Generation Company Limited to supply power to North and South Bihar discoms at Rs 6.075 per kWh. In May 2025, APL signed a power supply agreement with Uttar Pradesh Power Corporation Limited to despatch power from its upcoming ultra-supercritical coal-fired power plant in Mirzapur, Uttar Pradesh.

In August 2025, Torrent Power Limited secured a 1,600 MW LoA from MPPMCL for a greenfield ultra-supercritical TPP in Madhya Pradesh, comprising 2×800 MW units, to supply power under a 25-year PPA at Rs 5.82 per unit, with an investment of around Rs 220 billion.

In April 2025, JSW Energy Limited commenced the construction of its 1,600 MW ultra-supercritical TPP in Salboni, West Bengal, a Rs 160 billion greenfield project under a 25-year PPA with West Bengal State Electricity Distribution Company Limited.

Several new thermal projects have been announced in the past few months, with states inviting tenders to set up new coal-based power plants. In September 2025, the West Bengal government announced plans for a 660 MW supercritical TPP at Durgapur under a public-private partnership (PPP) model, with regulatory approval sought and a global tender to be floated. In August 2025, Tamil Nadu Power Generation Corporation Limited announced its plans to revive the stranded 660 MW Ennore TPS expansion project in PPP mode. In June 2025, the Assam government announced plans to establish a 3,400 MW TPP in the Bilashipara area of Dhubri district.

Cost economics of coal-based power projects

The capital cost of coal-based power projects has risen sharply over the years. Until 2017, the cost was around Rs 50 million-Rs 70 million per MW for operational projects and Rs 80 million-Rs 100 million per MW for under-construction projects. However, new projects announced by NTPC indicate costs exceeding Rs 120 million per MW. This escalation in capex is expected to put upward pressure on the cost of generation (CoG) for new coal-based projects. Furthermore, given the scale and complexity of these projects, execution delays beyond scheduled timelines remain a significant risk.

Following the recovery in electricity demand post-2021, medium-term supply from coal-based power projects has seen increased interest. Bids on the Discovery of Efficient Electricity Price portal over the past two-and-a-half years have aggregated to 6.4 GW for medium-term PPAs with tenures of four to five years, primarily driven by discoms in Haryana, Tamil Nadu and Uttar Pradesh. Average tariffs discovered in these bids have steadily increased from Rs 3.9 per unit in 2021 to over Rs 5 per unit in 2022, and further to over Rs 6 per unit in 2023. This increase reflects higher demand for coal-based power, coupled with limited fresh capacity addition in the private sector.

The CoG from new coal-based power projects is now estimated at over Rs 6 per unit, based on the proposed capital cost per MW of over Rs 120 million. Within the overall CoG, capacity charges account for 55-65 per cent, while the remaining can be attributed to fuel costs. Consequently, the CoG for new coal-based projects remains relatively high compared to the average power purchase cost, placing upward pressure on both the overall cost of supply and retail electricity tariffs.

Issues and challenges

The thermal power sector is facing multiple challenges, with flexible operation being the most significant. Traditional TPPs are designed for a steady, baseload generation, making frequent ramping up or down to match variable demand or integrate renewable energy difficult. This inflexibility often leads to inefficiencies, higher fuel consumption and increased equipment wear and tear.

The prospects for coal-based power projects remain closely tied to demand growth and the rising adoption of renewables and energy storage solutions. The viability of new PPAs largely depends on these factors, making the market outlook highly sensitive to shifts in the energy mix. At the same time, coal-based projects are prone to execution delays and cost overruns due to challenges such as land acquisition, regulatory approvals and contractor quality. Limited domestic equipment suppliers, coupled with mandatory local sourcing requirements for PPA eligibility, further constrain project timelines.

A large number of thermal plants are underutilised, resulting in stranded or stressed projects and significant financial losses. Ensuring a steady supply of coal is another major concern, as mining and transport disruptions, especially during the monsoon season, can reduce coal stock at plants and increase the risk of power shortages and blackouts.

Financial challenges add to the woes of the sector. Delayed payments from state discoms remain a persistent issue, with outstanding dues to independent power producers reaching Rs 583.21 billion as of September 25, 2025, according to the PRAAPTI portal. The weak financial health of many discoms affects PPA viability and timely payments. Financing coal-based projects has also become increasingly difficult amid growing environmental, social and governance concerns, which influence investor appetite and funding terms.

Moreover, TPPs face rising costs due to environmental compliance requirements, including emission norms and water usage reduction measures. Escalating capital costs and fuel prices contribute to high generation costs, further adding to the economic and sustainability challenges of coal-based power generation.

Outlook

To address these challenges, the thermal power sector requires a focused and well-planned approach. Ensuring a steady coal supply will be critical and can be achieved by diversifying sources, strengthening logistics and maintaining larger stockpiles to withstand disruptions. The sector must also adopt smarter investment practices and maximise the utilisation of existing assets.

Additionally, India’s power generation capacity is projected to reach 874 GW by 2031-32, with a target of adding at least 80,000 MW of thermal capacity. Of this, 28,020 MW is under construction, 19,200 MW has been awarded and 36,320 MW is in the planning stage. In addition, 13,997.5 MW of hydro and 8,000 MW of pumped storage projects (PSPs) are under construction, with another 24,225.5 MW of hydro and 50,760 MW of PSPs in the planning stage. Further, 7,300 MW of nuclear capacity is under construction and 7,000 MW is under various stages of planning and approval. In renewables, 147,160 MW is under construction and 79,270 MW is in the planning stage. Storage is also being scaled up, with 522.6 MW of battery energy storage systems under construction and 14,242.29 MW in the planning stages. The sector major, NTPC also has a significant project pipeline. The company has earmarked a total capex of Rs 559.2 billion for 2025-26 to add 11.8 GW of generation capacity, including 3.5 GW of thermal power.

India’s power generation segment is poised for accelerated expansion in the coming years, with capacity projected to rise significantly. While thermal power will continue to play a dominant role in ensuring baseload supply, renewable energy, supported by large hydro, pumped storage and emerging technologies such as battery storage, will drive the sector’s decarbonisation journey. Moving ahead, ongoing reforms in taxation, coal allocation and emission compliance, coupled with large-scale project awards across thermal, nuclear and renewable segments, are reshaping the industry landscape.

Akanksha Chandrakar