By Asmita Pant, Assistant Vice-President, ICRA Limited

By Asmita Pant, Assistant Vice-President, ICRA Limited

Generation mix shifts

Coal-based generation continues to dominate India’s electricity mix, despite a gradual decline in its share over time. Coal’s share in all-India electricity generation remained between 70 per cent and 77 per cent until FY 2025 and declined to around 68 per cent in FY 2026. While coal’s share in installed capacity has fallen steadily, reaching about 44 per cent by late 2025 due to rapid renewable additions, higher utilisation levels ensure that coal remains the largest contributor to actual generation.

Looking ahead, coal is projected to maintain the highest share in electricity generation until at least 2030, albeit on a declining trend. Renewable energy’s share in the generation mix, which increased from low single digits a decade ago to around 14 per cent by FY 2025, is expected to rise to around 36 per cent by 2030. Correspondingly, coal’s share in generation is projected to decline to around 59 per cent by that time, based on assumed electricity demand growth of about 5 per cent annually. These projections remain sensitive to actual demand outcomes and the pace of renewable integration.

State-level trends highlight divergent generation mix profiles. Renewable-rich states such as Rajasthan and Gujarat have recorded a sharp reduction in coal’s share in generation over recent years, driven by strong solar and wind capacity additions. In contrast, states such as Uttar Pradesh, Maharashtra, Andhra Pradesh and West Bengal continue to rely predominantly on thermal power. These differences reflect variations in resource availability, grid integration challenges and procurement strategies, resulting in differing cost structures and tariff pressures across states.

Power procurement patterns underscore coal’s continuing importance. In FY 2026, most major states are expected to procure more than 65 per cent of their power from coal-based sources. States such as Madhya Pradesh and Uttar Pradesh exhibit particularly high dependence on coal, while even relatively diversified states such as Maharashtra and Andhra Pradesh source a majority of their power from thermal generation. The government is targeting about 80 GW of new coal-based capacity by 2035, necessitating an incremental pipeline of around 30 GW beyond existing under-construction capacity.

Limited additions in hydro and nuclear capacity have further reinforced coal’s role as the primary baseload source in many regions.

Implications for tariffs

Implications for tariffs

A key factor shaping the outlook for costs and tariffs is the sharp increase in capital costs for new coal-based power projects. Capital costs, which were earlier in the range of Rs 50 million-Rs 70 million per MW and subsequently Rs 80 million-Rs 100 million per MW, have now risen to around Rs 100-120 million per MW for several recent projects. This escalation reflects higher equipment costs, compliance requirements and execution challenges, and has materially increased the cost of generation from new thermal assets.

Based on current assumptions, the levellised cost of generation for new coal-based projects is estimated at around Rs 6 per unit, with sensitivity to plant load factor (PLF) and capital cost. A significant portion of this tariff, around 65-70 per cent, comprises fixed charges, with the remaining accounted for by energy charges. As a result, lower PLFs increase the per-unit cost burden by spreading fixed costs over a smaller volume of generation, adding pressure on discom power purchase costs.

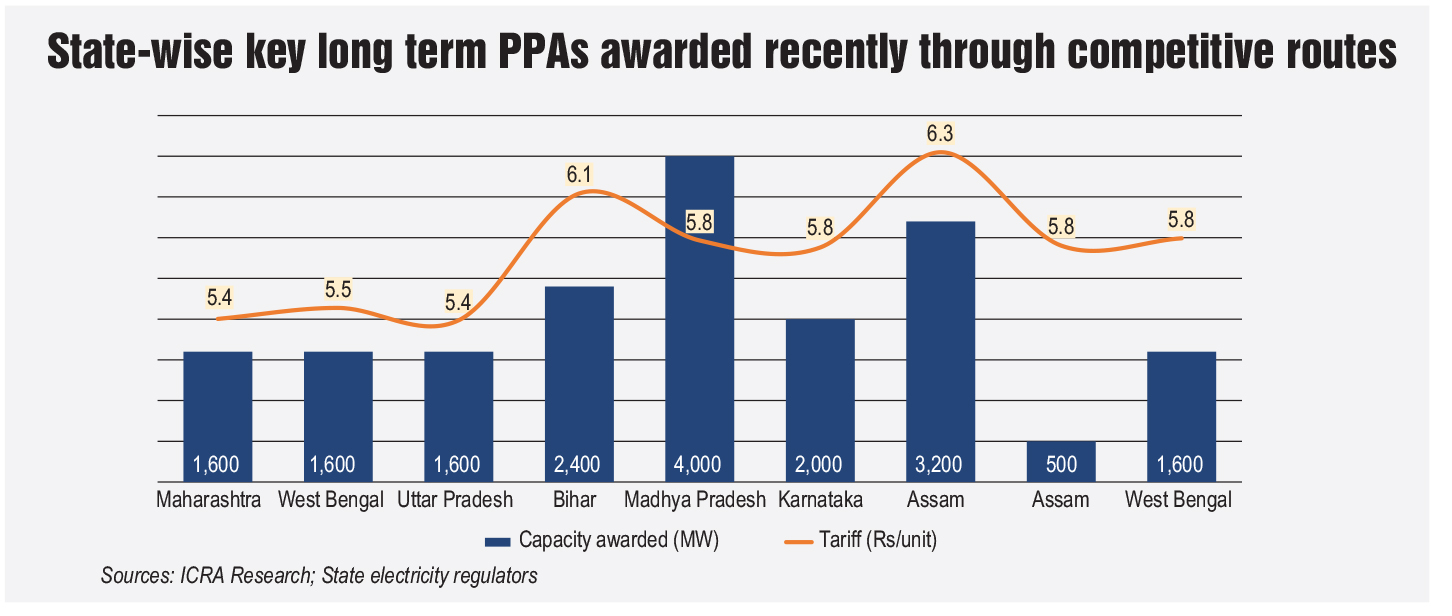

These higher generation costs have translated into elevated tariffs discovered in recent procurement processes. After nearly a decade of limited activity, long-term thermal power purchase agreement (PPA) bidding has revived. Several states, including Maharashtra, West Bengal, Uttar Pradesh, Bihar and Madhya Pradesh, have awarded long-term PPAs through competitive routes. Tariffs discovered in these bids have generally ranged between Rs 5.4 and Rs 6.3 per unit, with contract tenors extending up to 25 years. Around 18-19 GW of long-term thermal capacity has been awarded so far, with additional bids under consideration.

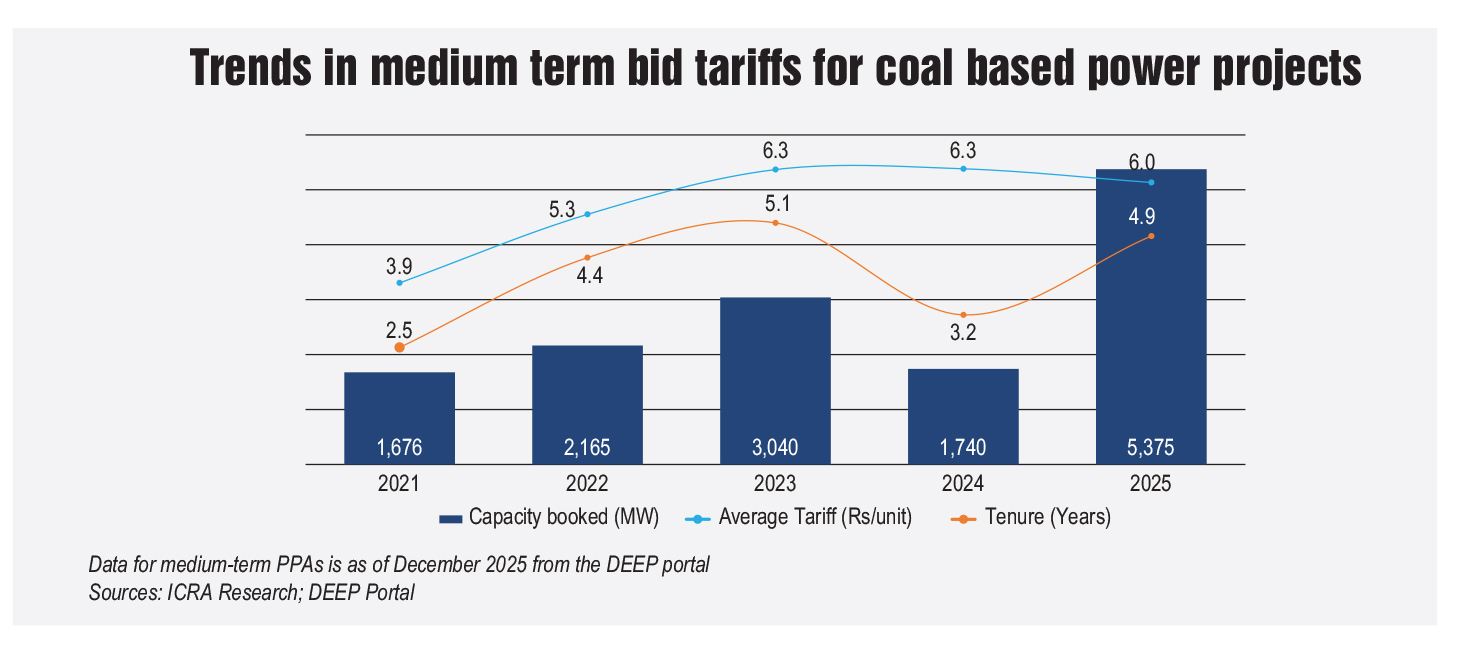

Medium-term procurement has also gained momentum. Medium-term PPAs, typically with tenors of three to five years, have seen tariff discovery close to Rs 6 per unit on average. Capacity booked under medium-term contracts has increased steadily over recent years, reflecting both discom efforts to secure supply amid adequacy concerns and generator preference to reduce exposure to volatile merchant markets.

In contrast, short-term market tariffs have softened. Spot power prices on the Indian Energy Exchange have shown a steady decline since FY 2024, following elevated levels during periods of strong demand and high coal prices earlier. During FY 2026 (to date), average spot tariffs declined to around Rs 3.5-Rs 3.8 per unit across market segments. While these prices remain above long-term historical averages, they indicate easing supply-side pressures and improved fuel availability.

In contrast, short-term market tariffs have softened. Spot power prices on the Indian Energy Exchange have shown a steady decline since FY 2024, following elevated levels during periods of strong demand and high coal prices earlier. During FY 2026 (to date), average spot tariffs declined to around Rs 3.5-Rs 3.8 per unit across market segments. While these prices remain above long-term historical averages, they indicate easing supply-side pressures and improved fuel availability.

Comparisons with alternative supply options such as round-the-clock renewable energy, firm and despatchable renewable energy and peak renewable solutions show that these options have demonstrated superior tariff competitiveness relative to new coal-based generation. However, the operational flexibility and system reliability offered by coal-based plants continue to differentiate thermal power, particularly in the absence of large-scale energy storage deployment. Until storage solutions scale up meaningfully, thermal power is expected to remain critical for meeting adequacy requirements.

Capacity pipeline, risks and supportive factors

Capacity addition trends point to a significant build-out under way. Over 50 GW of thermal capacity is currently under construction, including projects led by central public sector undertakings, state utilities, private independent power producers and stressed assets under revival. Public sector entities continue to dominate the under-construction pipeline, although private sector participation has increased in recent years. The government’s longer-term plans envisage around 80 GW of new coal-based capacity by 2035, implying an incremental pipeline of about 30 GW beyond existing under-construction capacity.

Estimates suggest that at an electricity demand growth of around 7-7.5 per cent annually, existing and under-construction capacity may be sufficient to meet requirements, assuming thermal PLFs of around 70 per cent. Higher demand growth or lower utilisation levels would necessitate additional capacity additions. As a result, future procurement activity remains closely linked to actual demand outcomes and utilisation trends.

Several risks continue to shape the outlook for coal-based projects and associated tariff outcomes. Prospects for new PPAs remain sensitive to demand growth and the pace at which renewables plus energy storage solutions emerge. Financing challenges persist amid environmental, social and governance considerations. Execution risks related to land acquisition, approvals, contractor quality and equipment availability remain relevant, particularly given domestic sourcing requirements for eligibility in PPA bids. Investments required to comply with emission norms and reduce water usage also add to cost pressures.

At the same time, certain supportive factors have improved the near-term outlook. Domestic coal availability has strengthened, coal stock positions have improved and imported coal prices have eased, contributing to fuel cost stabilisation. Reforms under the revised SHAKTI policy have streamlined coal allocation mechanisms, improving flexibility and access. Regulatory changes to emission norms, including location-based classification and exemptions for certain categories of plants, have reduced compliance-related capex for a large part of the installed base.

Another positive development has been the improvement in payment discipline. Monitoring mechanisms and liquidity support measures have shortened settlement cycles, strengthening cash flows for generators. However, state distribution utilities continue to face financial stress due to high aggregate technical and commercial losses, non-cost-reflective tariffs, heavy debt burdens and delays in subsidy releases. These factors continue to pose counterparty risk and influence procurement and tariff decisions.

Overall, the cost and tariff outlook for India’s power sector reflects a phase of transition and recalibration. Rising capital costs for thermal projects, higher tariffs discovered in long- and medium-term PPAs, and the continued need for reliable baseload capacity suggest that power procurement costs will remain elevated. The trajectory of retail tariffs will depend on demand growth, discom financial health, procurement strategies and the pace at which cost-effective and flexible alternatives to coal-based generation become operational.