The Indian grid has been growing in size and complexity over the years. Today, there is a national grid that operates on a single frequency, connecting all regions and enabling seamless power flow. Over the years, India’s interregional transmission capacity has been increasing to stand at more than 55,000 MW at present. The country also has a robust short-term electricity market, which has been growing over the years. All these factors have put additional pressures on the grid and led the operator to take measures for ensuring grid stability. The ancillary services market is a key tool in this regard. With the Central Electricity Regulatory Commission (CERC) set to notify a detailed procedure for ancillary services, stakeholders are gearing up for the same to be rolled out.

Power Line looks at the need for an ancillary services market in India, the suggested model for its deployment, its key challenges, and the benefits it is expected to provide to the grid operator…

Market overview

Simply put, the ancillary services market is a mechanism used by system operators to balance load and generation. A number of events can lead to a sudden power imbalance, which can be extremely detrimental to the grid. These include extreme weather, multiple generating units/transmission line outages and excessive loop flows leading to congestion. Ancillary services products include primary response or regulating reserve, spinning or operating reserve, demand response and voltage control. Global experience shows that these products are primarily market-driven. Ancillary service providers are paid assured charges for committing their capacity. In some countries, these services are anticipated by the system operator and commitment charges are factored into the annual revenue requirement. In this model, commitment charges are socialised, while energy charges are passed on to the specific entities responsible for invoking ancillary services.

Types of control

There are primarily three types of control that enable the system operator to balance generation with load. Primary control refers to the free governor mode of operation at generating stations, which enables action in 2-5 seconds, allowing frequency fluctuations to be smoothly controlled. In India, difficulties have been faced in the free or restricted governor mode of operation at power stations due to wide fluctuations in frequency. However, the Indian Electricity Grid Code mandates all thermal power stations with a capacity of 200 MW and above to be operated in restricted governor mode.

Secondary control, which is not deployed in India, refers to corrective action to bring the frequency back to 50 Hz. This is done through automatic generation control (AGC). A key requirement for AGC is that all generating stations above a certain size have to be under primary governor control. In addition, generating stations as well as state load despatch centres are required to have communication and control infrastructure for implementing AGC.

Tertiary control is required to manage large-scale system fluctuations. It helps in preventing large-scale grid outages.

CERC regulations

The CERC released its ancillary services regulations in August 2015, opting for a regulated model based on the unrequisitioned surplus of interstate generating stations (also known as tertiary reserves) rather than a market mechanism. Ancillary services are called Reserves Regulation Ancillary Services (RRAS). The tertiary reserves were non-existent at one point of time because of generation shortages. However, the significant increase in generation capacity over the past few years has made surplus reserves available in the system.

On whether the regulated model is the right approach, Anish De, partner, KPMG, says, “Making a market evolve on a full scale takes time. This mechanism provides a good starting point, provided that we transition to a full-scale market in a couple of years, which I think is the regulatory intent. The system does not create any legacy because you are not creating any capacity on this basis.” Highlighting this objective, S.K. Chatterjee, joint chief (regulatory affairs), CERC, says, “We have given the Power System Operation Corporation a directive to come up with a proposal on the market-based ancillary services mechanism by April 1, 2017. The CERC’s intent in rolling this out has also been articulated in a separate order on operationalising reserves. We are expecting that it should at least be there as a concept and precursor by March 2017.”

In its comments to the draft regulations, Statkraft Markets Private Limited, an inter-state trading licensee, mentioned, “The price for providing various services should be determined through market discovery rather than the regulated cost-plus route. Since these services are required for short periods but are extremely critical for maintaining and restoring grid functions, price determination should be based on the value-provided principle rather than cost plus. It is requested that the commission consider competitive market discovery as the mechanism for providing various ancillary services. A transparent mechanism similar to the spot market may be created for these services.”

Other industry experts feel that there is merit in first getting comfortable with the regulated model before moving to a market-based model. There are a number of nuances that need to be understood as far as the reserves are concerned. Nitin Zamre, managing director India, ICF International, says, “It is most appropriate to start in a regulated fashion because for a market-based mechanism, we need to have something on which investors can take a call. Under the market-based mechanism, the system operator is going to requisition this capacity as it is available in the market. Then, people have to start investing in it. For them to actually create that capacity, they have to have some comfort that the mechanism will work.”

The current regulations pertain only to one form of ancillary services: frequency control. The CERC defines the objective of RRAS as restoring frequency to the desired level and relieving congestion in the transmission network. However, industry experts feel that eventually all other services, including black start, will have to come up. “Initially, it will all be a combination of the regulation and market approaches, with the idea that regulation has to slowly and surely give way to more of a market approach. Some ancillary services are local services and might not have market feasibility, like voltage control, for instance,” says De.

In their comments on the draft regulations, many stakeholders have suggested that the definition of ancillary services be expanded to include all other services, including black start, voltage regulation and reactive power compensation. IL&FS Energy Development Company states, “With the passage of time, maintaining voltage and reactive power support and generation and transmission reserves in a regulated manner will become essential. At that time, separate regulations will be required to incentivise generators to provide these services. Including the other forms of ancillary services in the primary draft regulations will eliminate the complexity of introducing separate regulations.”

The regulations define two kinds of ancillary services: “regulation up” and “regulation down”. Regulation up implies an increase in generation while regulation down implies a decrease in generation by the ancillary service provider. The increase and decrease in generation will both be within the technical limit and time frame for responding to a change in system frequency or system congestion.

As far as the incentives for generators (ancillary services providers) are concerned, the present regulations provide for a mark-up on the fixed cost, which will be determined by the CERC in the case of regulation up (that is, when power is injected into the grid by the generator). As per Chatterjee, “In January, we had floated a draft order for determining the mark-up for the delivery of regulation up services, which proposed a mark-up price of 50 paise per unit, and sought comments. We are analysing the comments we received and the CERC will release the order shortly.”

In the case of regulation down, when the generator is asked to back down, it will pay back 75 per cent of the variable charges to the regional deviation pool account. So, there is a 25 per cent incentive for the generator in this case. Once the market structure takes over, this mechanism has the potential to become quite remunerative for ancillary services providers. “This is the observation in the rest of the world: as long as you are an efficient and flexible generator, you get value out of the ancillary services market,” says De.

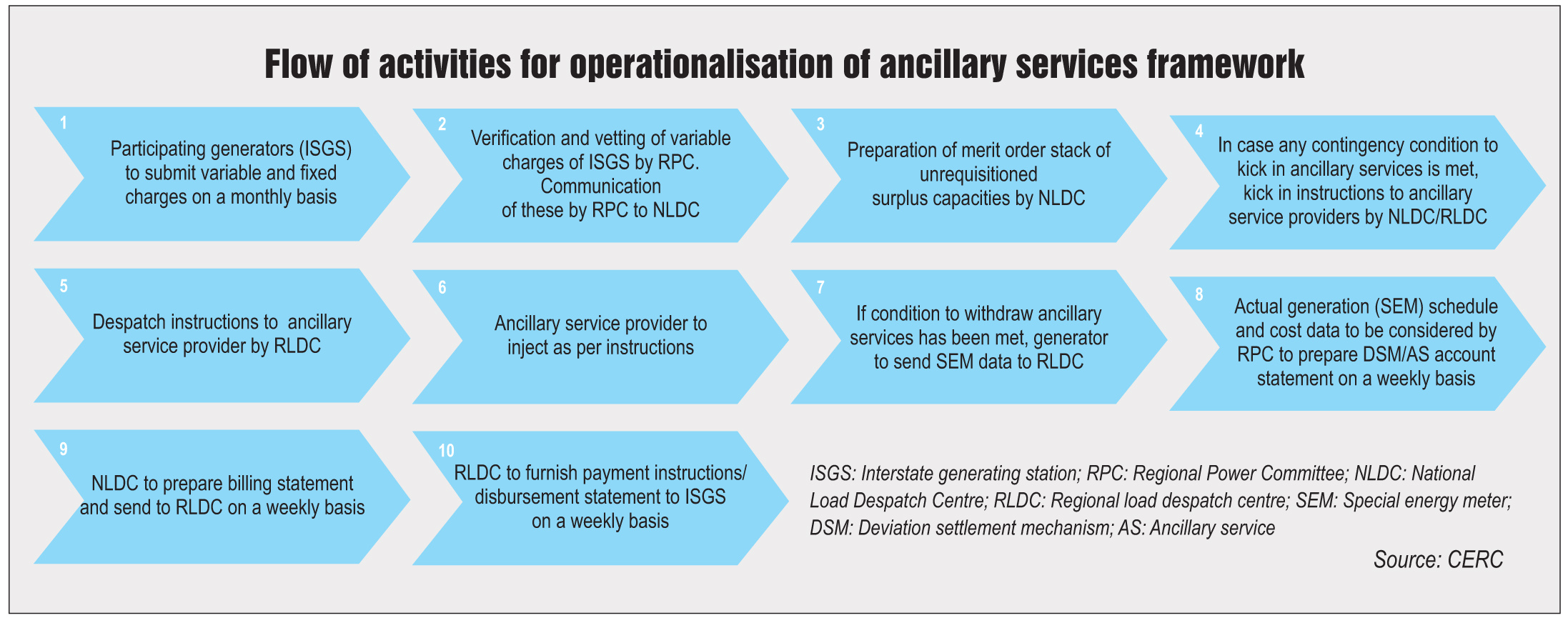

Operational mechanism

POSOCO has worked out a draft detailed procedure for ancillary services operations, which was submitted to the CERC for approval in November 2015. “We will approve the detailed procedure shortly, which is when the actual implementation of ancillary services will begin,” says Chatterjee. As a capacity building measure, POSOCO has held six workshops, one in every region, for detailed interactions with all stakeholders.

Generating stations providing ancillary services will be directed to do so on the basis of the merit order stack for unrequisitioned capacity, which will be prepared by the nodal agency. For regulation up, the stack will be in the order of the lowest to the highest variable cost in each time block, and the other way round in the case of regulation down. The ramp up or ramp down rate, response times, transmission congestion and other such parameters will also be taken into account.

A virtual ancillary entity, which has been defined in the regulations, will participate in the regional deviation pool and act as a counterparty for the schedule prepared for the despatch of RRAS providers.

Implementation challenges

While ancillary services are seen as a solution for grid disturbances, there are certain challenges in their implementation. “In ancillary services, you need to have a very active engagement with the market. Today, we have a separate system operator and market operator. Since the ancillary services market is really close to real time, the issue is whether it is the market operator or the system operator that runs the market. What is the interplay between the two?” says De. He continues, “Another challenge is the cost of energy in the ancillary services market because responding to real-time energy needs will be very different from the energy market. In such a scenario, the regulator should ideally not intervene without any justification. But this is not always easy.”

Commenting on the different roles played by the short-term power market and the ancillary services market, Zamre says, “The power market is going to be more transient, opportunistic and dynamic. In my view, the ancillary market, at least initially, will lock in capacity that can be used as ancillary services. So, the ancillary services market is not going to be a day-ahead market, unlike the power market. It will have to involve the procurement of capacity. This will require investments and that the system is kept ready for whenever it is required. Some of the capacity that is part of the power market today may shift to the ancillary market because it is better and provides more certainty, especially for the recovery of fixed costs.”

The trigger levels for the kicking in of ancillary services are also seen as a challenge. Commenting on this, Chatterjee says, “This is the first time that ancillary services are being implemented in India. So, the trigger levels will definitely be a big challenge. The detailed procedure defines various trigger points such as under what circumstances will POSOCO begin ancillary services. This is going to be the biggest test.” Another anticipated challenge is the complexity caused by the co-existence of the deviation settlement mechanism (DSM) and the ancillary services mechanism. In its comments on the draft regulations, Statkraft had mentioned, “The proposed coexistence of two real-time instruments – the DSM and ancillary services operations – could lead to more complexity, higher administrative costs and potential indirect costs due to the loss of coordination. It could also impede the implementation of a more thorough and well-functioning ancillary services market.”

Moreover, there are concerns that the introduction of ancillary services could lead to free-riding behaviour among utilities. Since the cost of these services will be socialised among all utilities, it could lower the cost of indiscipline for an entity overdrawing from the grid. However, some experts point out that the presence of DSM will ensure checks and balances. “The cost of grid stability has to and should be socialised because everybody is equally benefiting from the stable grid,” points out Chatterjee. It is also felt that there is greater awareness among utilities at present than a few years back. The whole aim of ancillary services is to ensure orderliness in the market and all utilities must learn to balance their portfolios. Ancillary services get activated only when there is a slight asymmetry for a short duration of time.

Another concern that has been pointed out is whether sufficient ancillary reserves will be available when actually needed, since only interstate generating stations are currently under its ambit. It has been suggested that plants in the country that do not have power purchase agreements (PPAs) or do not wish to sign long-term PPAs should also be included in the market to provide ancillary services. This will ensure that sufficient generation resources are available even on days when eligible generators do not have unrequisitioned capacity. As per industry experts, we currently have 2,000-3,000 MW of unrequisitioned capacity at all times, which sometimes goes as high as 5,000 MW. However, there could be some periods when this capacity goes down completely. Such a situation will highlight the need to consciously keep reserves with some generators.

It is largely felt that with the high growth in capacity addition, we may have enough reserves for a while to come. The key lies in maintaining spinning reserves rather than cold reserves. According to Zamre, “While the installed capacity is 288 GW, the highest peak capacity met is 150-160 GW. So, a huge capacity is available, even if one makes allowances for hydro, renewables, etc. A systematic understanding of this capacity is important. I am sure there will be a role played by the capacity that is today stranded – both coal based as well as gas based. All this needs to be understood very well by the system operator for this capacity to be accessed and used.”

The ramp up rate is another big issue and will be an important factor in providing ancillary services, it will be one of the decisive flexibility parameters and plants with higher flexibility will be rewarded.

Expanding the scope of ancillary services will require a concerted effort from all stakeholders. “Ancillary services should certainly grow into a bigger market, but the pace of this growth depends on how strictly system operators enforce grid stability. These are like insurance mechanisms, which must be present for unforeseen circumstances. Today, our systems, especially at the state level, are simply not in a position to look at something like an insurance mechanism,” says Zamre.

The first few months are expected to result in important lessons, which will be incorporated to improve the process. “We are starting with baby steps. There is scope for enlarging the spectrum we have accepted in the final order. We are going to ask POSOCO to come back with its operational experience in six months,” comments Chatterjee.

Conclusion

After a long wait, the country is finally taking the first step towards creating an ancillary services market. In developed countries, ancillary services have been introduced with all other aspects like adequacy; universal service obligation; quality of power; primary, secondary and tertiary controls; and reserves in place. In India, on the other hand, such developments are all taking place together. Moreover, the rapid growth of renewable energy is posing its own challenges for the grid. These unique situations and the requirements posed by them will drive and shape the ancillary services market in the years to come.