The situation today

The Indian power sector today is facing a strange conundrum where existing power plants are suffering from low utilisation rates (about 60 per cent) or are lying stranded either for want of fuel or power purchase agreements (PPAs); meanwhile, new renewable capacity and thermal capacity through PSUs is being added at a brisk pace.

Today, the grid-connected installed capacity in India stands at about 310 GW while peak power demand is only 170 GW. In addition, there is an estimated 60-90 GW of diesel generator (DG) set-based capacity installed by business establishments to provide standby power at prohibitive costs. As per the regulations set for the power sector, the projects are funded 70 per cent through debt, mainly from domestic financial institutions. The underutilisation of the existing assets affects the profitability of power companies and hampers their capacity to service their debt obligations, thereby increasing the risk of becoming non-performing assets (NPAs).

The large quantum of NPAs in the power sector has become a major potential challenge for lending institutions. Today, there is already an estimated 90 GW of grid-connected power capacity in the country that is stranded. Addressing this challenge will result in two major benefits for the country: it will give a boost to “Make in India”, thereby generating more employment, and ensure power to all.

Reasons for the situation

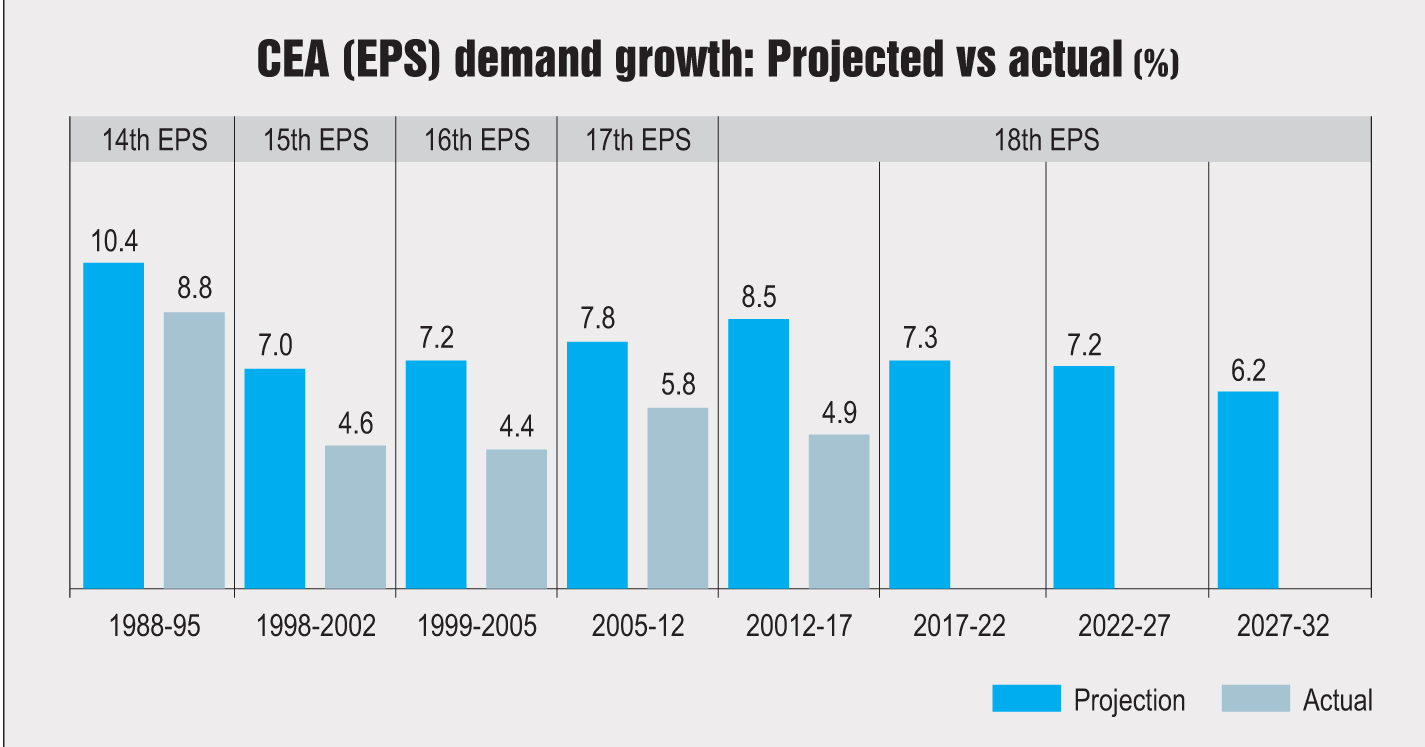

Power capacity addition in India is based on the five-year demand growth estimates prepared by the Central Electricity Authority (CEA). The CEA estimates are, in turn, based mainly on projections of the country’s GDP growth. Over the past few decades, the real growth in power demand has not matched up to the growth assumptions/CEA estimates. This can be due to factors such as less energy-intensive service sectors driving economic growth rather than the manufacturing sector. This is further exacerbated by the poor performance of distribution companies, which are plagued by high aggregate technical and commercial (AT&C) losses and resort to load- shedding rather than serving the latent demand due to poor recovery. This lack of sufficient offtake has led to large capacities of power plants not getting sufficient loads to serve. India’s per capita power consumption (1,010 kWh per annum) is very low compared to other countries such as China (4,000 kWh per annum) and developed countries (about 15,000 kWh per annum). Although efforts have been made to boost residential demand and the number of unelectrified villages has reduced to nearly half (6,175 as on December 31, 2016; Source: CEA) since the beginning of this financial year (11,344), a lot needs to be done on the industrial power consumption front. India has 60-90 GW of DG set capacity and about 60 GW of thermal generating capacity for captive, largely grid-connected generation, which has been set up by industries due to the absence or inadequacy of reliable grid-based power supply.

Possible remedies to enhance power demand and gainfully deploy built-up assets

Minimise the use of DG sets

The government should consider imposing steep taxes on the oil used, as also standby DG set equipment. It should actively deter users of DG sets and levy penalties on them for falling back on

oil-based power supply as it is neither environmentally friendly nor is it contributing to creating a robust grid. Grid-based power, even at industrial tariffs, is cheaper than DG set-based power. Deterring DG set users in the strongest manner will help shift this customer base to the grid and put pressure on the distribution companies to perform and not default on power supply. This could include imposing penalties in the event that they do not supply power.

Allow reliability charge and make state discoms accountable

Power distribution companies need to be made more responsible and accountable for the supply of 24×7 electricity, at least to major consumers such as industries and commercial establishments, to give a boost to economic activity. The Ujwal Discom Assurance Yojana has greatly helped reduce the financial burden of discoms, which should allow them to be able to procure and sell sufficient power to industrial consumers. In order to ensure reliability of supply, regulations should be formulated for penalising discoms for disruption of supply to industrial consumers, which may be to the tune of 1.25-1.5 times the tariff charged to the consumer (alternatively, discoms should pay consumers about 0.85 times the cost of oil burnt by them in DG sets). In order to finance the discoms for such a framework, a small reliability charge (about 50 paise per kWh) may be allowed to be charged along with the tariffs, thereby offering discoms an incentive to procure and supply sufficient power (including arranging temporary alternative power supply in case it is required). This initiative will consolidate power demand in the national grid, making it strong and robust, and will bring the highest value to all stakeholders in the long term. After the implementation of such a mechanism, if the discoms still undertake load-shedding, the regulator, supported by the central and state governments, should take action by depriving such discoms of tax benefits/other benefits under various schemes, or even consider privatising the deviant discoms.

Urgent correction of the cross-subsidy regime distortion

The average industrial power tariff in almost all the states today is higher than the industrial tariff charged in most developed countries. This is clearly not aligned to the government’s push towards “Make in India” and is, in fact, working to actually discourage making in India. In order to make industrial tariffs more cost competitive, cross-subsidy should be removed. Industry accounts for about 50 per cent of the total power demand in India and this one correction can substantially shift power demand back to the distribution companies and also send the right economic signals to all categories of consumers. Low-end domestic consumers may be cross-

subsidised by higher-end residential consumers or commercial consumers. The agricultural subsidy may be funded through high-end residential and commercial customers. This can be done through supplying power to even low-end consumers at the cost of supply and providing the subsidy through direct benefit transfer to the needy consumers’ linked bank accounts. The fund for cross-subsidy can be formed by accumulating the cross-subsidy surcharge into a corpus that is used for the disbursement of direct benefit transfers. This can help minimise leakage and reduce the misuse of subsidised power. By leaving industrial consumers out of the burden of cross-subsidising and keeping industrial tariffs as close to the cost of supply as possible, Indian manufacturing can be made greatly cost competitive with respect to global players. This can help bring more industries under the Make in India initiative, thereby creating more job opportunities and leading to the utilisation of India’s demographic dividend.

Incentivise incremental industrial consumption through tax sops

The current tariff constitutes an element of about 20 per cent as taxes charged as pass-through on the fuel side as well as on spares, service charges, etc. In order to incentivise job creation and “Make in India”, each category of industry can be incentivised to add capacity and expand its production and market activities. This can be done through a scheme in which all production units at more than, say, 20-25 per cent of the previous year would get 10-15 per cent discount as “credits” in industrial tariffs, to be funded through the goods and services tax or a specific corpus created for a boost in industrial production. This will help enhance the demand profile, as also improve competitiveness through economies of scale and create more jobs.

Supply-side initiatives: Re-evaluation of capacity addition programmes

In order to ensure that the existing generation capacity gets fully utilised and the existing PPAs are honoured, fresh capacity addition needs to be re-evaluated. There needs to be a hiatus on the setting up of new planned thermal capacity till such time this evaluation is completed. There are a large number of assets that are either under execution or have been executed but are stressed/ stranded due to a lack of PPAs or reliable fuel supply, or both. Meanwhile, large capacity additions have been planned by power sector PSUs. Nearly 50 GW of thermal capacity is currently under execution, mainly by PSUs. A large portion of the new capacity is expected to supply power at prices above Rs 4 per kWh, whereas the existing assets, with sub-Rs 3.50 per kWh generation, are lying stressed or are stranded. The PSUs get coal linkages and PPAs for these new projects, which should be held back as they are economically inefficient. Also, in light of the global climate change commitments, the efficiency of generating stations needs to be considered.

Expeditious retirement of old, inefficient generating sets

Old inefficient assets of nearly 35 GW capacity need to be retired and their fuel linkages and PPAs transferred to more efficient generating stations. The government should encourage consolidation in the sector, including PSUs acquiring stranded assets (instead of building new capacity), so that efficiencies are brought in. This would also create opportunities for growth in a sector that is otherwise facing lack of gainful deployment of new and efficient generating sets.

Reassess the pace of renewable capacity addition

The target for renewables may also be reassessed to identify the capacity that would be needed vis-à-vis the expected demand for power in the coming future, and what would be the most efficient way to meet the demand using renewables. A tapering down of growth projections in renewable generation may be necessary to ensure a smooth transition in the country’s power mix.

PPA or privatisation of the distribution supply business

Power is available at near variable cost on a short-term basis on the power exchanges, but this is not being lifted by the discoms. Meanwhile, load-shedding is often resorted to for curtailing demand. Efficiency needs to be brought into the distribution business in order to ensure that the lowest possible price of power is offered to consumers. A way to do that can be through reforms that allow the introduction of competition in the distribution supply business, which is controlled by state-owned entities in most places. As observed in the case of Delhi, reforms in the distribution business, allowing private players to bring in professional management, have led to efficiency in discom operations, as demonstrated by the lowering of technical and commercial losses and ultimately benefiting consumers. The bane of distribution companies is AT&C losses. Unless these are brought down all over the country, tariffs cannot be lowered.

The above suggested steps to revive growth in power demand and utilise the installed capacity are imperative for ensuring that generating stations do not become NPAs and help drive the engine of the Indian economy.

The above suggested steps to revive growth in power demand and utilise the installed capacity are imperative for ensuring that generating stations do not become NPAs and help drive the engine of the Indian economy.