Goods and services tax (GST), set to be rolled out from July 1, 2017, brings a host of changes in the taxing regime for the power sector. Reduction in tax on coal, higher tax on boiler, turbine and generation (BTG), and tax on renewable energy equipment are the key changes for the power sector under GST. Broadly, these would impact the project cost, generation cost, etc. Power Line looks at the overall impact of GST on the power sector…

Impact on power generation

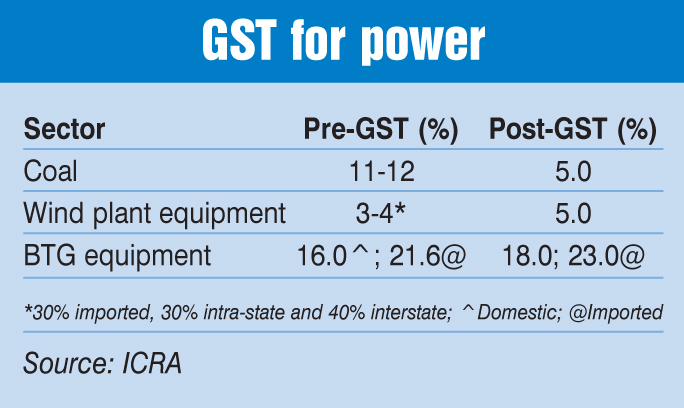

One of the distinctive features of the new tax regime impacting the power sector is lowering of the tax rate on coal. Coal has been placed in the 5 per cent slab, as against an effective tax rate of 11 per cent to 11.5 per cent for domestic coal under the current regime. Roughly, the effective domestic coal price is likely to decrease by Rs 100-Rs 150 per tonne. Imported coal will also be charged basic customs duty which will increase the cost of imported coal.

Looking at the other charges on coal under GST, a cess of Rs 400 per tonne currently levied as clean energy cess will be levied as state compensation tax, which would be utilised to compensate states for loss of revenue post-GST. Another change under GST is the tax increase on BTG and balance of plant (BoP) systems, which would result in an increase in the capital cost of new plants. This equipment has been placed in the 18 per cent slab under GST, as against the current 16 per cent tax rate. Further, imported equipment will be charged around 23 per cent as against the current 21.6 per cent.

Overall, GST is expected to provide relief in the cost of power generation owing to a reduction in coal tax, despite higher tax rates on BTG. As per ICRA’s research estimates, the variable cost of generation is expected to decline by 3-4 paise per unit for domestic coal, and increase by 7 paise per unit for imported coal. Another expected benefit from the lowering of tax on coal is a short-term trigger in coal demand which is expected to reduce mounting pithead stock at Coal India Limited.

Impact on renewable energy

GST places solar and wind power equipment in the 5 per cent slab, as against zero taxation for solar and 3-4 per cent for wind in the pre-GST regime. In the solar power segment, GST is expected to increase the capital cost of projects by 4-6 per cent. As per ICRA estimates, GST on solar power projects would increase the levellised cost of generation by 11-12 paise per unit. Meanwhile, for under-construction solar projects, the capital cost burden would increase and this would be allowed to the developers under change in law. As solar tariffs have nosedived in recent months, pass-through of high cost incidence would be critical. On the other hand, it is believed that a huge decline in equipment prices offers a sufficient buffer for developers to withstand high tax rates. For the wind power segment, GST is expected to result in a marginally negative impact due to an increase in capital cost. A higher tax rate on wind turbine generators, as against various concessional rates and tax exemptions enjoyed so far, is expected to increase the cost of wind projects by around 4 per cent, assuming 30 per cent imported components, as per ICRA estimates.

Impact on other segments

GST provides service tax exemption on transmission and distribution of power. Although this would prevent an increase in the cost of power to the end-user, transcos and discoms will not be able to claim input credit, and the cascading effect of taxation may linger in these segments. Another important aspect for the discoms under GST is that lowering the tax rate for coal will bring down the cost of power. However, as the discoms are already in losses, it is uncertain whether the cost reductions will be passed on to the end-consumer. For equipment manufacturers and technology providers, there would be no change from the existing taxation scenario in the case of offshore procurement of goods and services as well as onshore input services. On the other hand, for onshore procurement, companies would be eligible for full input tax credit, as against no credit for central sales tax and value added tax. Besides this, for outward supply of service, electrical equipment would be taxed at 18 per cent under GST (as against 16 per cent in the pre-GST regime) and technology providers would be charged 18 per cent as against the pre-GST rate of 15 per cent. Meanwhile, EPC contracts have been placed in the 18 per cent taxation slab, as against the prevailing tax rate of 22 per cent.

Conclusion

One of the issues with the imposition of GST in the energy sector is the exclusion of electricity duty from GST. This exemption breaks the credit chain, leading to a cascading of taxes and an increase in the tax incidence on the end-consumer. Besides this, to ensure smooth GST roll-out, it is essential to ensure that all stakeholders are allowed necessary compensations under change in law and that contract enforcements are undertaken in a transparent and timely manner. In conclusion, GST would bring changes in the energy sector in the short term as the stakeholders would take time to adjust to the new normal. In medium to long term, it would benefit the sector by eliminating cascading taxes and enhancing transparency.