The thermal power sector has been facing considerable stress due to a number of issues, most importantly, low demand from discoms. While there has been an absence of fresh power purchase agreements (PPAs) by discoms, in another setback for power producers, the Uttar Pradesh government recently cancelled the bids conducted in 2016 to procure 3,800 MW through long-term PPAs in favour of cheaper short-term power. With spot prices at below Rs 3 per unit, renewable energy tariffs falling to an all-time low and the availability of other procurement channels such as the Discovery of Efficient Electricity Price portal for meeting short-term power needs, the traditional long-term PPA model is being challenged. Industry experts discuss the implications of the shift away from long-term power procurement on stakeholders…

Is the electricity market moving away from long-term PPAs as discoms turn to short-term contracts? If so, what are the key drivers for this change?

Jayant Kawale

Jayant Kawale

While I have nothing in particular to say about the Uttar Pradesh decision to cancel bids, which I am sure is based on their assessment of the situation, in general, distribution utilities need to adopt a balanced approach and develop a basket of sources of power — baseload, intermediate and peak load, as well as long-term, medium-term and short-term power. It may actually be possible to get very competitive rates in today’s market for long-term or medium-term power. It is, however, certain that a procurement strategy based solely on short-term power purchase may end up causing a lot of damage to a discom if the power market were to take a turn and become more of a sellers’ market than it is today. Today’s “surplus” may suddenly turn out to be illusory, as it is the result of a number of factors, which may not continue to hold.

Ashok Khurana

Ashok Khurana

All distribution utilities require an optimal mix of long-term/medium-term/ short-term and spot market power procurement to meet their demand variations. Prior to the Eleventh Plan period, there was a huge scarcity of generation capacity and the power market was essentially a sellers’ market. Therefore, discoms always favoured long-term contracts to ensure security of supply to meet seasonal and peak load variations. At that time, the prevailing rates in the spot market ranged from Rs 7 to Rs 8 per unit.

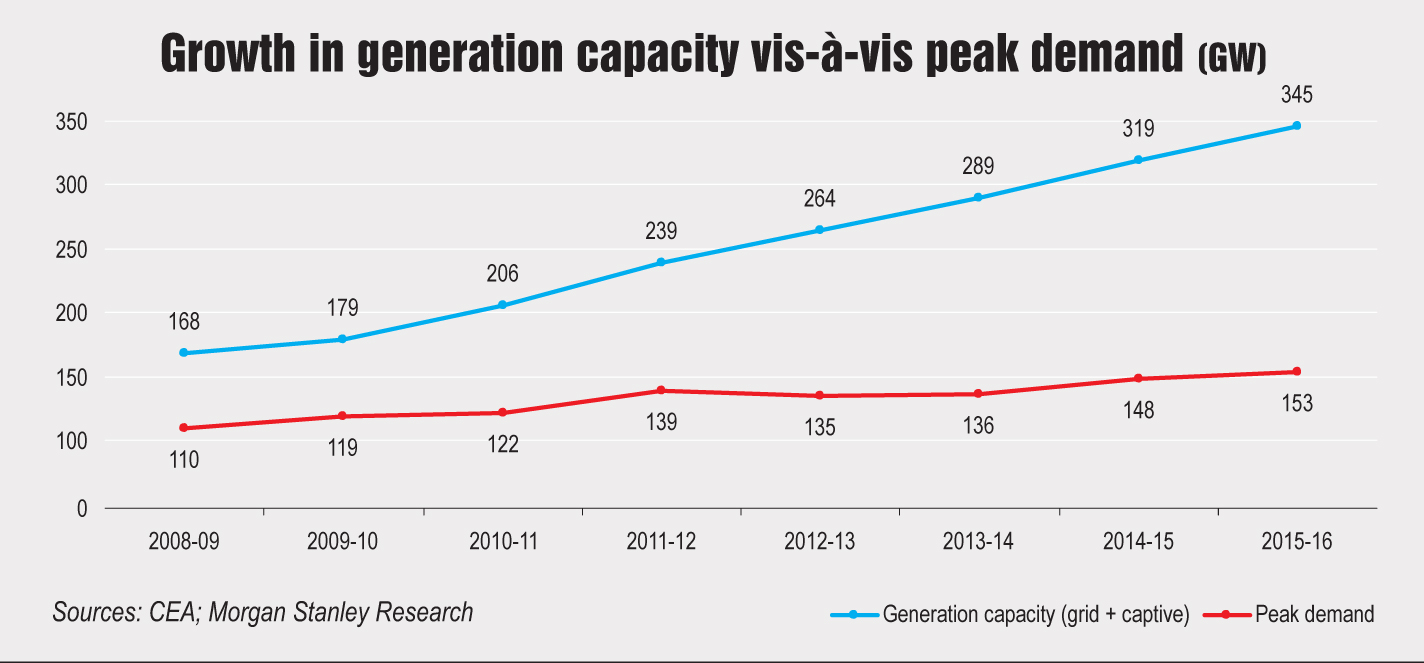

With capacity explosion in the Eleventh and Twelfth Plan periods, and demand not picking up as forecasted, the stipulation has changed dramatically (see graph).

Currently, there are 180-190 GW worth of long-term contracts and the baseload ranges from 130 GW to 135 GW. Coupled with this, we have idle capacity of about 14,000 MW and an aggressively growing renewables sector. With this, the market clearing price has come down to approximately Rs 2.65 per unit. In the last decade, we have moved from a sellers’ market to a buyers’ market. In this scenario, it makes a lot of commercial sense for discoms to buy from the spot market to meet demand variations, if any.

The key drivers for this changed scenario are:

- The exponential increase in thermal capacity and a mismatch between demand and supply.

- An accelerated increase in renewable energy capacity addition to meet the COP 21 targets, and the drastically falling renewable energy prices (almost achieving grid parity).

- Tepid growth in demand, especially in the commercial/industrial segment.

- The inadequate purchasing capacity of intermediaries between generators and consumers.

Sabyasachi Majumdar

Sabyasachi Majumdar

Electricity demand in the country increased at a compound annual growth rate (CAGR) of 4.7 per cent during the period 2009-10 to 2016-17, while thermal power generation capacity increased at a CAGR of 11.4 per cent. As a result, the utilisation of thermal power generation capacity witnessed a significant decline, from 77.5 per cent in 2009-10 to 60 per cent in 2016-17. The subdued growth in electricity demand can be attributed to the weak financial health of state-owned distribution utilities, which constrained their paying capacity, as well as to the muted demand growth from the industrial segment. As a result, the overall progress in signing long-term PPAs through competitive bidding by state-owned discoms remained slow, with discoms in only two states signing PPAs with independent power producers (IPPs) in the past four years. As per ICRA estimates, about 26 GW of capacity in the private IPP segment (both commissioned and under-construction) does not have long-term PPAs, increasing their risk profile. This has, in turn, led to the lack of fresh investments in the thermal power segment by the private sector.

The thermal segment is also facing competition from the renewable energy segment, given the policy focus on increasing the share of renewable energy-based generation in the overall electricity mix and the significant decline in power tariffs for wind and solar power projects in the recent past. Also, prices in the short-term market have remained favourable for discoms, having declined over the past two to three years due to a significant increase in the power generation capacity, improvement in inter-regional transmission capacity for transferring electricity from power-surplus regions to those with high levels of energy deficit and the introduction of the reverse auction-based e-bidding mechanism for short-term power procurement in April 2016.

Although discoms are signing long-term PPAs with central and state-owned power generation companies at cost-plus tariffs, they are not floating tenders for long-term PPAs through competitive bidding. Rather, the discoms seem to prefer short- and medium-term PPAs up to five years instead of committing to tariffs under 25-year PPAs in view of the subdued demand growth, falling renewable energy tariffs and lower costs as agreed under the Ujwal Discom Assurance Yojana (UDAY). While this may lower the cost of procurement in the near term, discoms will not have long-term supply security and will remain exposed to volume and tariff risks in the electricity market when demand picks up.

Going forward, the signing of longer-term PPAs by discoms would depend upon the improvement in their financial profile under UDAY, demand recovery from the industrial segment and progress in the implementation of village electrification and 24×7 electricity programmes.

Chandan Mishra

Chandan Mishra

The electricity market is in the midst of massive disruption with various conflicting influencers — competing generation options and cost competitiveness of technologies, emergence of renewables, demand growth and the ability of discoms to pay, tariff-related issues and the availability of open access, sourcing based on the demand curve, etc. This is impacting the earlier model of contracting power. It is also shaking up the traditional models of long-term PPAs, wherein projects were set up to cater to the demand (with no differentiation across base or peak) of specific states or regions, and the requisite transmission network had to be built. It needed long-term certainty for project financing based on the available financing products from lenders, which was offered by the regulatory regime and the subsequent competitive bidding framework.

With the development and availability of appropriate generation capacity at competitive rates, power exchanges, financial products, transmission infrastructure and interconnected grid, utilities have the flexibility to source power for a stipulated period to meet specific demand. Power sourcing contracts now have an appropriate mix to meet the emerging demand curve. Thus, discoms have been extremely judicious in sourcing power from exchanges.

Kuljit Singh

Kuljit Singh

The current move by the state electricity boards to source more power through short-term contracts is purely opportunistic as there are several thermal and hydro projects without PPAs that have no option but to sell at whatever rate is available in the market. However, this opportunity is largely due to the benign power demand-supply situation in India, which has been created by a combination of load shedding by discoms, and slow growth in demand vis-à-vis growth in supply. Further, developers are willing to supply at rock-bottom rates in short-term markets as they believe that after a few years the demand-supply imbalance will correct and prices will rise to levels wherein developers will be able to not only recover historical losses but also charge good tariffs.

Is this model desirable in the long run? What are the implications of such a model for discoms, generators and financiers?

Ashok Khurana

The desirability of any model always depends on the ground realities. It can be expected that a demand-supply equilibrium would be reached in the next four to five years owing to the following factors:

- 30 per cent of households are unelectrified and 500 million people are dependent on solid biomass for cooking.

- The per capita energy consumption is less than one-third of global average.

- Reduction in the additional capacity installation pipeline.

- Demand to pick up with growth in the economy through initiatives such as Make in India, Smart Cities Mission and 24×7 Power for All.

Thereafter, the discoms would start their power procurement plans afresh and, having learnt from past experience, they would not depend entirely on long-term power procurement as during the time of scarcity. This is likely to lead to the discovery of a fresh balanced equation between long-term/ medium-term/short-term and spot market power procurement, depending on each distribution utility’s area-specific requirements. Stress in the sector is expected to continue for the next four to five years, and we would see a phase of consolidation. All these idle/stalled capacities are viable if seen in the long term, once the period of demand-supply mismatch is over. Therefore, it behoves all stakeholders – developers, bankers, distribution utilities and the government – to chalk out a strategy for mitigating the adverse impact of this mismatch in the medium term.

Sabyasachi Majumdar

Developers and financiers would want to have tariff certainty over a longer period for recovery of their investments, given the long gestation period of thermal power projects and the high quantum of debt involved. However, in the current scenario of shorter-term PPAs, financiers may have to come up with innovative lending products to fund power projects having PPAs of 5-10 years, instead of 25 years. Thermal power generators should also look to diversify their customer profile and have a mix of discoms and industrial customers and also a mix of PPAs, that is, short-term, medium-term and long-term PPAs.

Chandan Mishra

Market players have to adjust to the new paradigm and respond to the requirements of the discoms, which is opportunistic. If financial products are developed to meet this market design and generation capacities are built, it will be a sustainable model.

It has significant implications for market players because market volatility may disrupt operations and increase costs. It has to be taken into account that generation capacity addition for baseload stations takes more than four years. It has implications for all players in various respects:

- Discoms: Uncertainty of availability and price over a longer period; and the possibility of losing out on cheaper power from suppliers post 12-15 years of operation. So discoms need to have an appropriate mix of contracts for operating optimally.

- Generators: Planning, scheduling, efficiently operating, and securing financing.

- Financiers: To develop products necessary for financing projects with a duration shorter than the loan duration.

Kuljit Singh

Having a mix of long-term PPAs and short-term contracts is not bad in itself. However, what is not good is that government-owned discoms are exploiting the situation by completely doing away with long-term PPA procurement. While this does provide short-term benefits to discoms, in the medium to long term, this may lead to great hardships for consumers and discoms. As private developers continue to incur losses or receive poor returns, the development of new coal- and gas-fired power stations and hydropower stations has come to a virtual standstill in the private sector (financiers and developers simply do not have the courage to invest more money in the power sector). It may be noted that it is primarily due to the huge capacities being set up by private players that India has reached a seemingly benign demand-supply situation. If the development of new projects by the private sector comes to a virtual standstill, India may again revert to a period of significant power supply shortfall. However, discoms are currently not so bothered, as they seem to be swayed by government projections that suggest that new capacity additions are not required for the next five years or so, and by the tariff success being seen in recent wind and solar auctions. But this may ultimately backfire as the demand-supply situation corrects (new thermal capacity in India takes around five to six years to commission) and the discoms discover that, in the absence of cost-efficient storage solutions, wind and solar can end up creating large and unpredictable deficits. Hence, the government may be well-advised to encourage discoms to start locking in some part of their incremental requirements under the new long-term PPAs.

However, this may be done in a staggered manner so that the discoms can lock in the best possible rates. Further, with a large number of distressed projects in the thermal power sector, there is a possibility in the near term that the capital structure of these projects will be written down (through debt and equity haircuts via various routes including NCLT). Hence, if at this point of time discoms come up with long-term PPA bids, they may be able to capture the tariff reduction that may arise in the system due to the above-referred debt and equity haircuts.

As far as financiers and developers are concerned, since they have already invested billions of dollars in setting up capacity, they have no option but to wait for and follow whatever strategic policy initiatives are framed by discoms with respect to long-term PPA procurement. In a nutshell, financiers and developers are really not the decision makers in determining the fate of the power sector. The fate of the generation sector will be determined by government-owned, operationally inefficient and commercially unsavvy discoms.

(Note: The views expressed by Kuljit Singh are his personal views and do not represent those of his company.)