The distribution segment is one of the most important yet among the weakest links in the electricity value chain. Over the years, the government has made several attempts to turn around this segment. But while it has pumped significant money into it through various programmes and tried to bail it out three times in less than 15 years, the segment continues to remain in the red.

The Electricity Act, 2003 laid the foundation for bringing in competition at the consumer end through the introduction of concepts like open access and parallel distribution licensees. However, the experience with both these concepts has not been quite successful. Almost 15 years after the passage of the Electricity Act, the distribution segment is still grappling with high aggregate technical and commercial losses triggered by rampant power thefts, technical issues, corruption involving suppliers and users, subsidised or free power, dilapidated networks, inadequate metering, lack of consumer orientation, and poor operational and financial management.

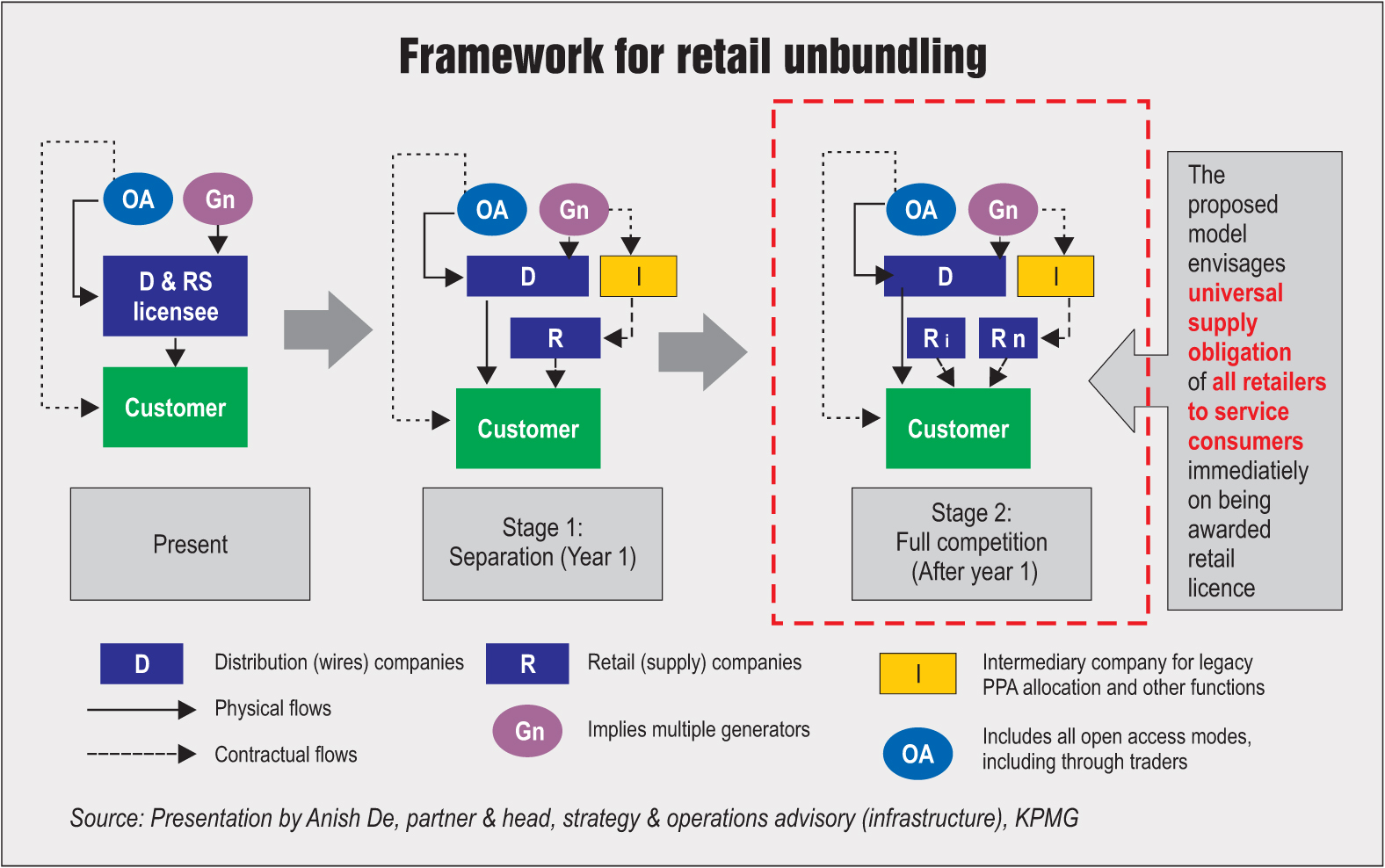

To resolve these issues and bring in competition in retail supply, the Electricity Amendment Bill, 2014 was introduced in the Lok Sabha in December 2014. The bill, among other things, proposes the separation of the carriage (wires) and content (retail) businesses. With this, the incumbent state utilities, which would be responsible for the wires business, can concentrate on system strengthening while new retailers can compete amongst themselves to provide consumer services. The separation is expected to empower consumers and allow them to buy electricity from a power company of their choice.

As with most reforms, there has been significant opposition to the bill from various quarters, particularly the states, discoms and unions. A major challenge has been, and will continue to be, building a consensus with the states, which is necessary given that electricity features on the concurrent list.

To understand the views of various stakeholders and suggest changes, the bill was referred to the Parliamentary Standing Committee on Energy, which presented its report in the Lok Sabha in May 2015. The centre has also been holding discussions with the states to reach a consensus on the proposed amendments. The government had hoped to introduce the bill in the 2016 winter session of Parliament and then in 2017, but it is, in fact, yet to be placed in Parliament. Now, the Ministry of Power (MoP) is preparing a new draft bill, which will be placed before the cabinet for its approval and subsequently presented in the upcoming budget session of Parliament.

R.K. Singh, minister of state (independent charge), MoP, has also reiterated the government’s intent to introduce multiple supply licensees in the content business based on market principles, and continue with carriage as a regulated activity. “Consumers will be able to change their power suppliers just like they can in telecom. The service efficiency of suppliers will improve and it may also result in the disappearance of electricity theft.”

Industry structure under the new regime

The Electricity Amendment Bill, 2014 envisages a single distribution company in each supply area, multiple supply licensees as well as an intermediary company (IC) to be formed for the allocation of existing power purchase agreements (PPAs). Besides the responsibility of PPA allocation to various supply companies, the bill gives the central government the flexibility to define other responsibilities for the ICs. To protect the interests of consumers, the tariff for the retail sale of electricity is proposed to be capped through the regulator and one of the supply licensees is proposed to be a government-controlled company. The existing distribution licensees may continue till their term ends.

A transfer scheme has to be drawn up by the state governments for the segregation of the content and carriage businesses within a specified period. Based on the roll-out plan finalised by the state and central governments, the roles and responsibilities of the three entities – the discom, the supply licensees and ICs – could be enumerated. The central government has emphasised that adequate checks and balances should be provided in the detailed transfer scheme to safeguard consumer interests. “The transfer scheme is the key to protecting the interests of the stakeholders involved. In the absence of a standard approach, the adoption of this reform will get delayed as the states will individually evaluate the options,” says Kameswara Rao, partner, energy, utilities and mining, PricewaterhouseCoopers (PwC).

The existing provisions of Sections 12, 14 and 15 of the Electricity Act have been proposed to be amended to include electricity supply as a separate licensed activity, among other things. Distribution businesses, being monopolistic in nature, will serve as common carriers and operate as a regulated activity. Currently, due to huge financial losses and overhead expenses, discoms tend to neglect upgradation of their networks, which adversely impacts their efficiency. With the separation, distribution licensees will be responsible for the development, and maintenance of the distribution network, which will be a pass-through based on the performance standards set by the regulators. Meanwhile, system operators (currently, the state load despatch centres) can focus on technical and operational efficiencies as well as market operations, and retail suppliers can focus on power procurement, consumer interface and services. Depending on the final legislation, metering-related activities could be handled by the distributor, the supplier or a separate metering company. “The functional separation of wires and supply will require planners and regulators to rework many of the operating standards, responsibilities and performance measures. Further, he explains that having given up the supply responsibility, the discoms will focus on upgrading their networks to improve reliability, reducing thefts and leakages, and investing in innovation in smart meters, charging stations for electric vehicles and digital payments.

Issues and challenges

Issues and challenges

Competition in retail supply has been successful in several countries such as the UK, Australia and the US. While India can draw lessons from these success stories, the actual segregation process could be quite complex considering the many contentious issues in the Indian context. According to S.K. Soonee, adviser, POSOCO, who has been involved in the content-carriage separation process at the interstate transmission level for over a decade, “The stakeholders and authorities are still grappling with several regulatory, administrative and implementation issues related to access, transmission pricing and planning.” While Rao agrees that this reform is far more complex than the earlier structural unbundling because the functions of distribution and retail supply are far more intertwined, he adds that we have the benefit of several years of experience in open access, which can be used to implement this reform.

Taking on board all the stakeholders would be a major challenge. The National Coordination Committee of Electricity Employees and Engineers, a broad-based platform of unions and national federations of electricity workers and engineers, has been vociferously campaigning against the bill. It has been holding regional and state-level meetings to mobilise consumers against the bill. Shailendra Dubey, chairman, All India Power Engineers Federation, claims that the bill seeks to privatise the profits and nationalise the losses in the power sector based on the premise that carriage-content separation will lead to an exodus of high-paying and profitable consumers to the private licensees.

Clearly, the transition has to be handled sensitively. “It is essential that there is a structured communication plan that articulates the disruptions that the discoms face in the content business and why the proposed framework is beneficial for the discoms and their employees, most of whom are involved in the carriage of electricity, not the content,” says Anish De, partner and head, strategy and operations advisory (infrastructure), KPMG.

Although the new draft amendment bill is being finalised by the power ministry, some of the issues were discussed and agreed upon by the standing committee in its report. Several issues have been discussed in the Forum of Regulators (FoR) report on “Roll Out Plan for Introduction of Competition in Retail Sale of Electricity”, prepared by PwC.

One of the key issues relates to the treatment of financial losses. The existing regulatory assets of the discoms would be transferred to the IC, which would then amortise these either by collecting a universal charge (UC) or through financial support from the state government. Other unrecognised losses in the discoms’ books would either be allocated to existing companies or support sought from the state for cleaning up the balance sheets. De insists that clear treatment would be required for financial baggage. “The accumulated financial losses are very large in several places and without financial restructuring and parking elsewhere, such separation and competition would be difficult in many places.” Clearly, before venturing into the new regime, it would be prudent to liquidate the regulatory assets. This has been recommended by the standing committee as well.

Technical and commercial loss allocation has to be undertaken between the distribution and retail supply businesses. The existing metering infrastructure till the distribution transformer level will have to be upgraded by the distribution licensee to accurately calculate the loss levels and assist in balancing and settlement between the multiple retail supply companies. De says that reconciliation between the wholesale (15-minute block) and retail (up to two months) transactions will be a challenge in case of non-availability of time-of-day metering. Separately, the responsibility for electricity theft must be fixed up front on either the network operator or the supplier.

In terms of the time frame for rolling out retail supply competition, the bill initially proposed implementation in one go, as a period of one year was provided following the passage of the bill. However, the government has been open to increasing this period to two to five years. Recently, the government has stated that the timeframe would be left open to the states.

The FoR report proposes a three-stage implementation process to ensure a smooth transition. This comprises functional segregation of discoms by defining new functional entities, including their roles and responsibilities in the first stage (one to two years); preparation for competition through the creation of a level playing field for all by removing entry barriers such as cross-subsidy reduction, upgradation of metering and loss allocation in the second stage (two to three years); and the onset of competition where new retail supply licences would be given and the market opened up for competition in phases for a defined set of consumers (ongoing activity till all consumers are open to competition).

De agrees that implementation has to be phased. It should start with a manageable set of customers and then be extended to all others within three to four years. Rao feels that it should be possible to truly offer customer choice once the performance standards and cross-subsidy regulations are codified. This can be done in 12-18 months, if undertaken on a national basis.

To allay discom fears regarding cherry-picking of consumers by the supply licensee, the standing committee suggests that clear norms should be laid down to ensure equitable apportionment of consumers based on the status of consumers, the direct and cross-subsidies being paid to them, and the technical and commercial losses. The specification of conditions of the licence must not be left to the discretion of the appropriate state electricity regulatory commission (SERC) as envisaged initially to restrict any arbitrary power of the commission. Rao agrees that the principles for the determination of cross-subsidies should be articulated clearly in the law itself to minimise the state-level regulatory risk. “This is a serious matter as supply companies will inherit a large financial gap as the prevailing tariffs of residential and farm consumers do not cover the cost of supply,” he says. Some of the possible solutions for reducing the current levels of cross-subsidies, are annual tariff hikes, using a UC, limiting subsidies to wheeling charges and direct subsidy from the government. Further, instead of leaving the choice of selecting the area to the private supply licensee, areas where supply licensees could be allowed must be progressively notified.

The provision of a last resort supply licensee must not be restricted to the government supply licensee. The universal supply obligation (USO) must be mandatory for all licensees in their respective areas as well as in areas that may be assigned to them to ensure a level playing field for all licensees.

Another contentious issue is whether simply charging a fee would be sufficient for recovering the huge investments in distribution lines and the high maintenance costs. Therefore, an appropriate decision needs to be taken on whether additional charges need to be levied for availing of distribution network services.

To ensure fair and non-discriminatory functioning of the IC, it is suggested that certain guidelines be formulated, particularly since the creation of such a company by unbundling of the distribution function could result in additional transaction costs without any value to consumers. Further, if the dynamic allocation of PPAs is permitted, it could lead to a single window for the purchase of electricity.

Rao explains that in theory, competition benefits are greater if more PPAs can be transferred to the wholesale market, wherein energy is auctioned every half-hour rather than being fixed for 25 years. “In practice, this can happen only over a period of time as signed PPAs will be honoured to their full term. Further, for the wholesale market to generate real efficiency gains, similar deregulation and competition in coal supply is needed,” he says.

Yet another aspect, a crucial one, relates to consumers and includes issues regarding meter installation, billing, disconnections and grievance redressal. The standing committee feels that these issues need to be resolved in a broad manner early on, and can then be fine-tuned by the states based on local conditions. A mechanism may be proposed for giving consumers a choice of supply licensee, transfer of system from one to another based on the choice of consumer and the cost involved in such transfer. For instance, De points to the issue of security deposit maintenance and its treatment for consumers desiring to switch. “As per the present construct, security deposits need to be maintained by consumers with both the network and supply companies, and it is non-transferable.” Another related issue is the ease of consumer interface. “Should consumers have a single-point interface with the supplier or should they be required to interface with the distributor as well?”

The creation and maintenance of a consumer database must be undertaken by the distribution licensee to begin with and shared with retail suppliers for consumers under their respective jurisdictions. Independent and neutral access must be ensured for all retail suppliers. According to De, an assessment should be made whether a separate registry needs to be created for metering information and customer data to aid switching.

An important aspect for ensuring consumer protection and 24×7 supply in a competitive regime would be the stipulation of maintenance of adequate reserve margins for suppliers. The treatment of franchisees is also an important aspect. Franchisees appointed by licensees to undertake distribution or supply on behalf of the respective licensees would not be required to seek permission from the SERCs. One concern is how to make franchisees accountable to customers. In addition, there needs to be greater clarity on how the separation will be handled in the case of private sector licensees.

There are other issues that need to be addressed as well. Given that renewable energy is growing rapidly, De believes that interfacing the carriage and content separation with aspects like gross and net metering needs to be considered. He also questions the practicality and effectiveness of having a government-owned licensee in each supply area and the continuation of state ownership of wires. On the latter point, he says that this has not been done elsewhere in the world where network and supply functions were unbundled.

Impact of retail competition

According to the FoR report, the key objectives of retail supply competition are providing consumers with a choice, improving power access and availability, ensuring efficient power procurement, and improving efficiency and loss reduction. Consumers can derive several benefits from retail competition such as lower tariffs, the introduction of innovative products (like green power, seasonal supply, demand response, etc.), efficiency in services, and increased use of cheaper and cleaner sources of electricity.

“The benefits of reform will flow swiftly, viz. power plants will improve utilisation, the manufacturing sector will get cheaper power and avoid spending capital on captive plants, smaller consumers will get improved service, and the discoms will gain from growing sales,” says Rao.

The likely issues that may hinder these benefits from reaching the consumers are little scope for differentiation since electricity is a homogenous product, network congestion that would limit the retail suppliers’ service ability despite procuring power from the cheapest sources; and switching costs for consumers.

The way forward

While the content of the bill is yet to be finalised, it is hoped that it will provide solutions to several of the above issues. Further, while the timing of the legislation is uncertain, it may be a good idea to functionally segregate the distribution and supply wings of discoms and prepare the ground for greater efficiency. Eventually, the introduction of competition in retail supply is inevitable for ensuring operational efficiency, commercial viability as well as consumer orientation in distribution. “This is a fundamental reform. The transition from an era of energy-deficient and centralised production to that of energy-surplus and distributed generation has not percolated down to the consumers,” says Rao.

According to De, “Once out of the realm of antiquated systems and practices, the segment can become a magnet for innovation. In such a paradigm, consumers will be more discerning, choosing their own rate plans, deciding on when to consume based on visible, real-term price signals, sometimes selling electricity back to the grid from their self-generation and storage facilities, remotely managing consumption, feeding back precious information to system managers and operators – the possibilities are infinite.” “The key question at this stage is not the objective of separation, but how to attain the end-goals of efficiency and customer service through such measures.”

The focus now should be on handling the implementation issues and building a consensus with the states. If all goes well and the bill is enacted in the budget session as anticipated, it would be a watershed moment for the electricity sector. While consumers may have to wait for at least four to five years to actually be able to choose between suppliers, the foundation for the beginning of a new regime would have been laid.