")

The distribution segment continues to be the weakest link in the power sector. The poor financial and operational performance of the discoms characterised by high aggregate technical and commercial (AT&C) losses, mounting discom debt and high book losses continue to hamper the growth of this segment. Various policy measures have been under discussion to reform the segment, with the latest being various reforms proposed under the draft Electricity (Amendment) Bill, 2020 to promote private participation in the segment, ensure a cost-reflective tariff structure, and strengthen the payment security mechanism and regulatory framework. A look at the key trends and developments in the power distribution segment…

Operational performance

As per India Infrastructure Research, between 2014-15 and 2018-19, the total distribution line length grew at a compound annual growth rate (CAGR) of 4.11 per cent to reach 11.12 million ckt. km as of March 2019. The majority of the distribution line length (around 57 per cent) is at the low tension level, followed by 39 per cent at the 11 kV level and the remaining at the 33 kV level. Nearly 816 GVA of transformer capacity was operational at the 33 kV level and below, across 50 utilities in the country, as of March 2019. This has increased at a CAGR of 7.57 per cent. The total electricity consumers are estimated to be around 278 million as of March 2019, with the domestic category accounting for the largest share of consumers, at nearly 79 per cent of the total consumers. Further, during 2018-19, the total energy sales in the country stood at 926 billion units.

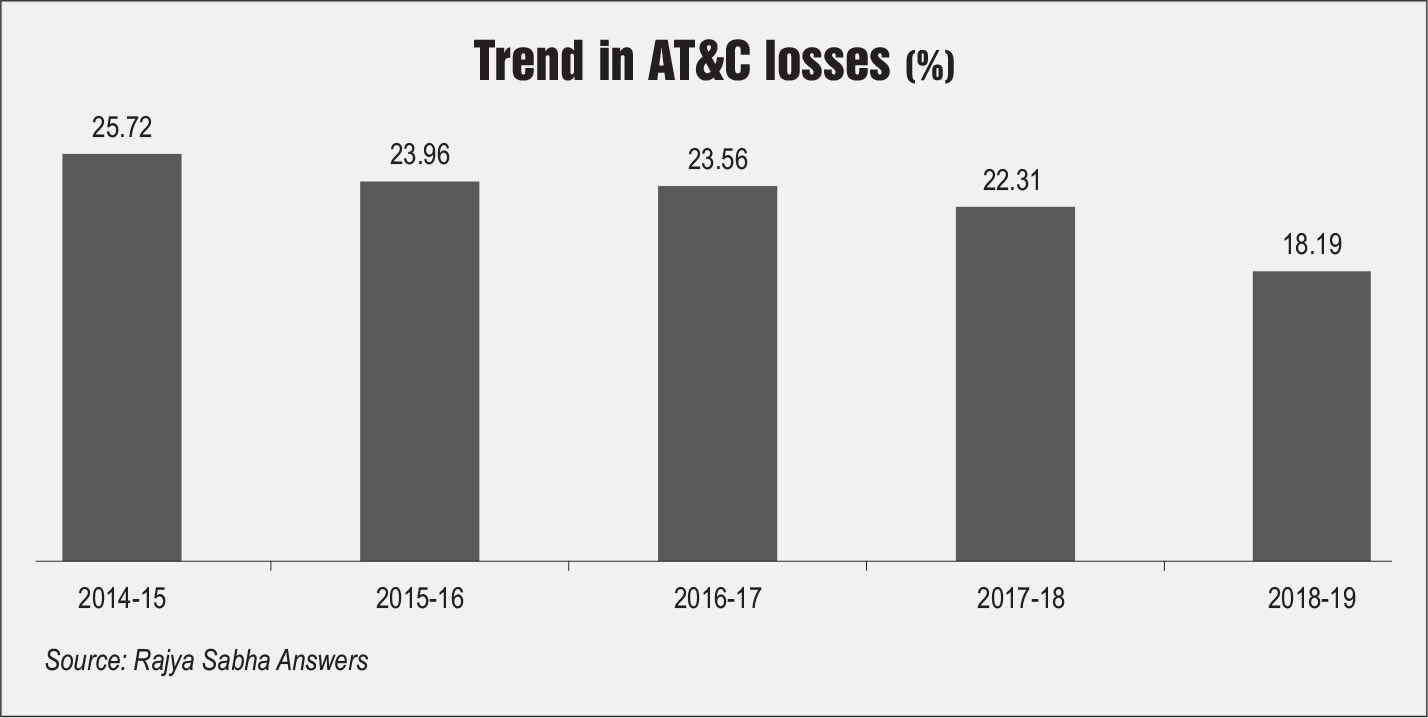

The all India AT&C losses witnessed a steady decline during the past five years, from 25.72 per cent in 2014-15 to 18.19 per cent in 2018-19. The AT&C losses are still higher than the target of 15 per cent set under the Ujwal Discom Assurance Yojana (UDAY). The progress in AT&C loss reduction has been skewed across states. While some states have managed to achieve the 15 per cent target, various others have AT&C losses of over 30 per cent (such as Meghalaya Power Distribution Corporation Limited and the Jammu & Kashmir Power Development Department). During 2018-19, states including Gujarat, Himachal Pradesh, Punjab, Andhra Pradesh, Uttarakhand, Kerala and Tripura have met their AT&C loss targets.

The discoms’ average cost of supply (ACS)-average revenue realised (ARR) gap has reduced from Re 0.59 per unit in 2015-16 to Re 0.27 per unit in 2018-19. A total of 20 states witnessed a reduction in the ACS-ARR gap between 2015-16 and 2018-19. The gap ranged from Rs-1.21 per unit (Puducherry) to Rs 2.13 per unit (Jammu & Kashmir) in 2018-19.

Financial performance

Financial performance

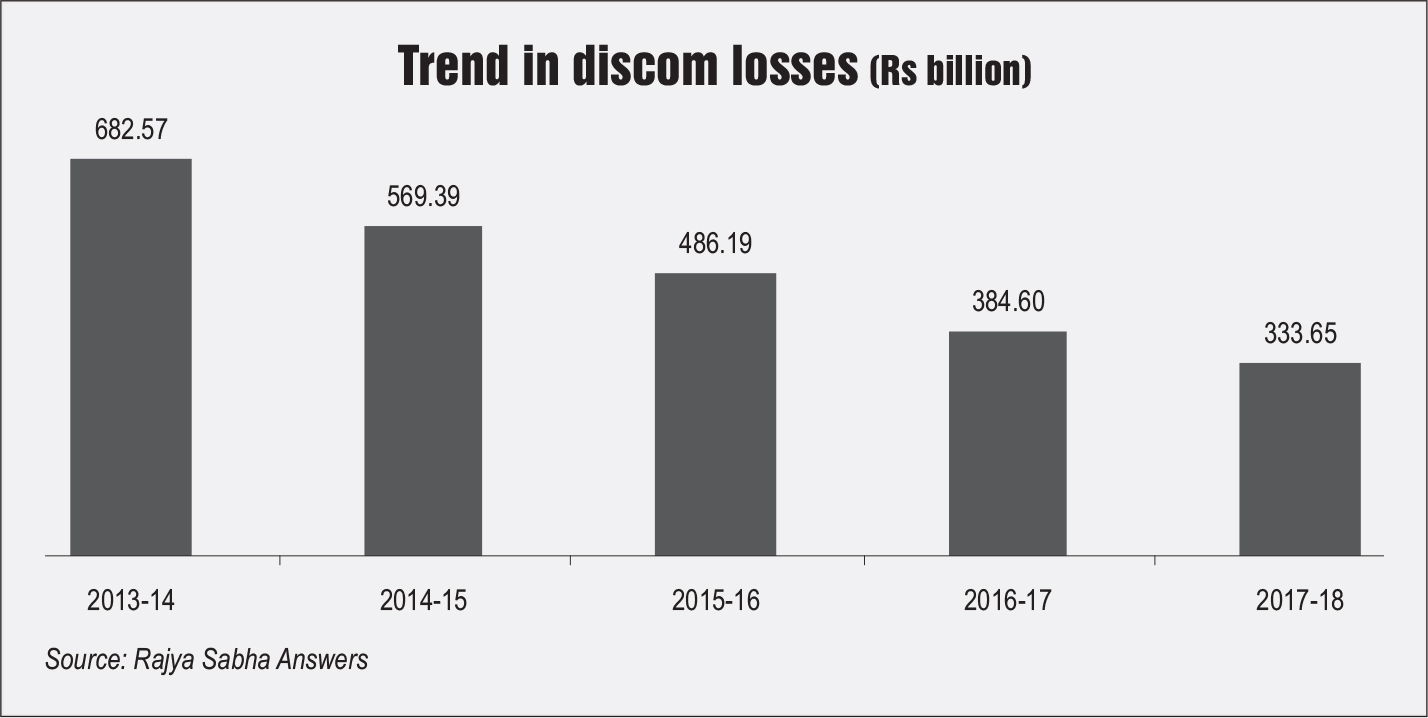

Discom losses witnessed a significant decline between 2013-14 and 2017-18. As per the latest information furnished by the Ministry of Power (MoP) in the Rajya Sabha question-answer session, discom losses have declined from Rs 682 billion to Rs 333 billion. The decline in discom losses could be attributed largely to debt restructuring done under UDAY, reduction in AT&C losses and an increase in tariff rates.

With regard to the discoms’ outstanding debt, as per the latest information furnished by the MoP in the Rajya Sabha question-answer session, the debt level of discoms has increased. The pre-UDAY debt level of 16 UDAY states, which signed the comprehensive MoUs with the central government, was Rs 3.24 trillion as of September 30, 2015. The outstanding loans at the end of 2018-19 stood at Rs 3.5 trillion, of which Rs 633.55 billion was the amount of loan balance to be converted into grants by the states.

The discoms’ outstanding dues to generators have more than doubled from Rs 380 billion in September 2018 to over Rs 800 billion as of February 2020, as per data from the PRAAPTI (Payment ratification and analysis in power procurement for bringing transparency in invoicing of generators) portal. As of February 2020, about Rs 319 billion of the total dues were pending with central public sector undertakings, Rs 212 billion with state gencos, Rs 204 billion with independent power producers, and Rs 70 billion with renewable energy generators.

Recent developments

Recent developments

Relief measures for Covid-19: The nationwide lockdown due to Covid-19 has led to a significant decline in power demand from the commercial and industrial (C&I) segment as well as delays in payment of electricity bills, which is expected to worsen the overall liquidity position of discoms. The Covid-19 lockdown has caused a massive drop in electricity demand of around 20-22 per cent. There has been a sharp decline in the electricity consumed by C&I consumers as well as the railways. Since these consumers cross-subsidise domestic and agricultural consumers, the revenue loss is even more significant.

In view of this, the MoP has directed the payment security mechanism to be maintained by discoms with gencos for the despatch of power will be reduced by 50 per cent. The obligation of the discoms to pay within 45 days of the presentation of bill (or the period given in the power purchase agreement [PPA]) remains unchanged. Failing to do so, the late payment surcharge (LPS) would be applicable on the discoms. For the period between March 24 and June 30, 2020, the LPS has been reduced; however, after June 30, 2020, LPS will be payable at rates given in the PPAs/regulations. The obligation to pay for capacity charges and transmission charges as per the PPA will continue. As per the payment security mechanism applicable from August 1, 2019, the National Load Despatch Centre and the Regional Load Despatch Centre schedule and despatch power from generation companies to distribution utilities only after the implementation of the payment security mechanism, in the form of a letter of credit (LoC) by discoms to generation companies. The move is aimed at tackling the issue of delays in payments by the discoms to generation companies and has instilled some payment discipline among the discoms as the rate of increase of unpaid due has decelerated.

ADITYA: Reportedly, a new reform-linked scheme tentatively named Atal Distribution System Improvement Yojana (ADITYA) is expected to replace UDAY, which expired on March 31, 2019. The new scheme is expected to focus on institutional reforms and making discoms financially sustainable. The government expects an outlay of about Rs 3,000 billion under the scheme, which aims to lower the AT&C losses of discoms to 12 per cent, reduce the gap between costs and revenue and promote private participation in power distribution. States with more than 18 per cent AT&C losses can opt for an infrastructure support reform package, which entails choosing between running discoms on the public-private partnership model, outsourcing distribution to multiple supply and network franchisees and working through input-based distribution franchisees. The scheme is expected to be implemented in three phases till 2024. The first phase is likely to entail infrastructure upgradation, including the implementation of smart meters worth Rs 2,300 billion, of which 15 per cent would be provided by the central government and 10 per cent by the state government. Under the second phase, the inefficient discoms would undergo institutional reforms to be able to take advantage of the investment support. Meanwhile, Phase III is likely to focus on the development of human resources.

Other developments: In one of the key announcements, the central government under the latest budget has set a target to replace all conventional electricity meters with smart prepaid meters in the next three years. This is expected to create a demand for close to 300 million smart meters in the coming years, and is likely to significantly transform the manner in which electricity metering has been done in the country so far, though the timeline for its implementation is likely to be affected by the Covid-19 crisis.

In a first-of-its-kind exercise, a National Perspective Plan at the distribution level is being prepared by the Central Electricity Authority. Till now, the central government has been preparing perspective plans for the generation and transmission segments under the National Electricity Plan. The distribution plan would keep consumers’ needs at the centre of its focus, the power ministry stated. The plan anticipates an increase in distribution substation capacity of 38 per cent and in distribution transformation capacity of 32 per cent as well as an increase, of 27-38 per cent in feeder lengths till 2022. In another key development, in June 2019, Power Grid Corporation of India Limited and NTPC Limited came together to form a joint venture (JV), the National Electricity Distribution Company (NEDC), for undertaking distribution operations. The JV has been set up on a 50:50 equity participation basis. The main aim of the NEDC is to undertake electricity distribution and related activities in states and union territories.

In a first-of-its-kind exercise, a National Perspective Plan at the distribution level is being prepared by the Central Electricity Authority. Till now, the central government has been preparing perspective plans for the generation and transmission segments under the National Electricity Plan. The distribution plan would keep consumers’ needs at the centre of its focus, the power ministry stated. The plan anticipates an increase in distribution substation capacity of 38 per cent and in distribution transformation capacity of 32 per cent as well as an increase, of 27-38 per cent in feeder lengths till 2022. In another key development, in June 2019, Power Grid Corporation of India Limited and NTPC Limited came together to form a joint venture (JV), the National Electricity Distribution Company (NEDC), for undertaking distribution operations. The JV has been set up on a 50:50 equity participation basis. The main aim of the NEDC is to undertake electricity distribution and related activities in states and union territories.

To conclude, implementing policy measures to promote private participation, lower network losses and the enhance financial viability of the discoms are steps in the right direction and are likely to yield results in the coming years. However, implementing these in the right spirit, along with closely monitoring the progress under various policies, is critical to obtain the desired outcome.