It’s a trend that marks a significant u-turn in the government’s approach towards coal imports. After two straight years of decline, in 2017-18, coal imports rose to 213 mt, increasing by almost 11.5 per cent over the previous fiscal (191 mt). India’s overall coal imports had declined by over 6 per cent each in 2015-16 and 2016-17. The uptick in coal imports seen in 2017-18 is attributable to the shortfall in domestic coal supply, owing to transport bottlenecks (railways) and a surge in coal demand by thermal power plants.

Acknowledging that the shortage situation is likely to persist, the government has now asked utilities to start importing coal. “We have written to the states allowing them to import coal as per their requirements. Coal will continue to be a problem for two to three years till new mines are opened,” stated R.K. Singh, minister of state (independent charge), power, and new and renewable energy, at the recently held conference of states’ power ministers in July. This is in sharp contrast to the situation in 2016, when coal production had marked a steady increase, to the point that there was surplus production and the government wanted the utilities to pursue a domestic coal sourcing strategy. It had thus announced plans to completely eliminate thermal coal imports for the next few years. Power Line takes stock of the recent trends in coal imports and the outlook going forward…

Import trends

During the period April 2017-March 2018, the country imported 155-158 mt of thermal coal according to industry estimates. The corresponding figure for 2016-17 as per coal ministry data is around 149 mt. About 80-85 per cent of the thermal power capacity is partially or fully dependent on imported coal. Meanwhile, imports of coking coal (one of the key inputs for steel production) were about 46.5 mt in 2017-18, nearly 8.1 per cent higher than that in the previous fiscal, accounting for about 22 per cent of the total coal imports during the year.

According to data from the Indian Ports Association, the top 12 major ports reported a 19.32 per cent surge in imports of thermal coal to 28.28 mt during April-June 2018. In the corresponding quarter of the previous financial year, the ports had handled 23.7 mt of thermal coal. For coking and other coal, an increase of 6.85 per cent was reported during the first quarter of the current fiscal at 13.03 mt. Source-wise, Indonesia remained the country’s largest source of thermal coal imports. About three-fifths of the imported coal came from Indonesia, followed by South Africa. Meanwhile, imports from the US also gained traction. In 2017, India reportedly imported 7.54 mt of thermal coal from the US; in 2018, till April, thermal coal import volumes from the US more than doubled.

What caused the current coal shortage

What caused the current coal shortage

Thermal power demand has been increasing, as is reflected in the improvement in the plant load factors (PLFs) of thermal power plants. Interestingly, in 2017-18, the declining trend in thermal PLFs was arrested and the overall thermal PLF went up by approximately 80 basis points to 60.7 per cent. While the PLFs for central public sector units went up by 109 basis points to 72.4 per cent, state utilities, which account for one-third of the installed thermal capacity, recorded a 255 basis point improvement to 56.9 per cent.

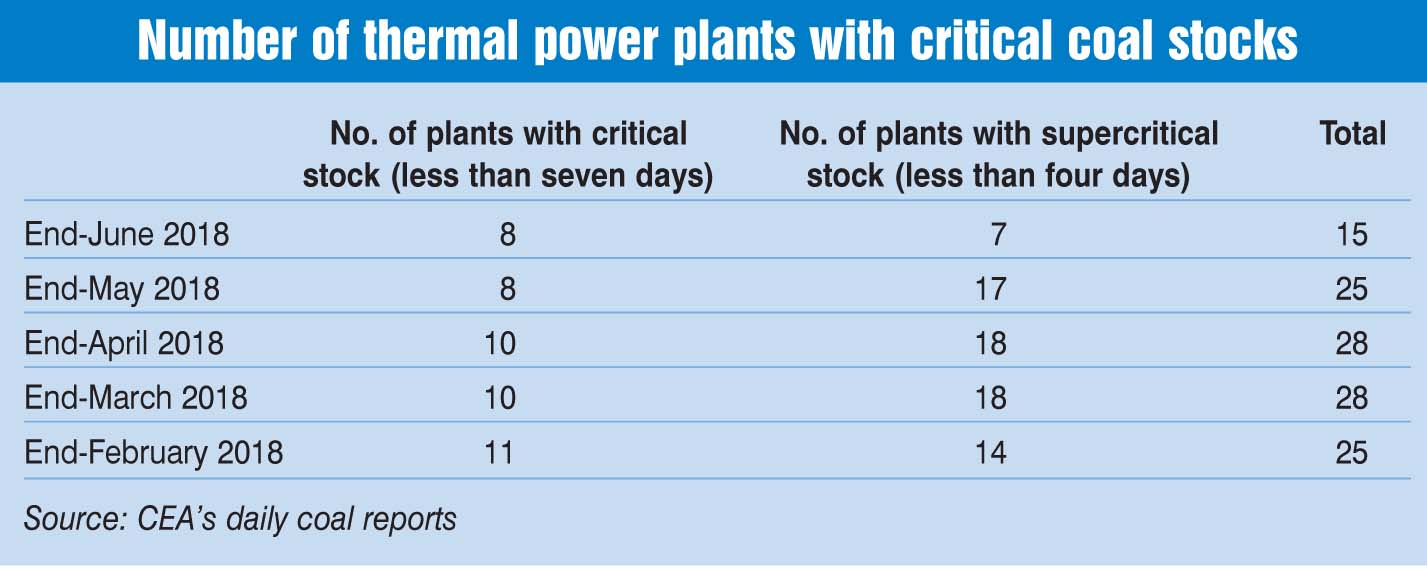

The resurgence in thermal power demand, say analysts, has also been on account of lower generation from wind and hydro power this year. Further, there has been a steady decline in power plant coal stocks since April 2017 as states delayed coal procurement. This triggered the current coal shortage as thermal power plants were already sitting on low coal stocks. As the Central Electricity Authority’s (CEA) data for end-June 2018 shows, all power plants were left with just 10 days of coal stocks on an average against the normative requirement of 22 days, and about 15 plants out of 116 power plants across the country had critical stocks (of less than seven days).

State-run Coal India Limited’s (CIL) production performance has also not been up to the mark. In the past three years, CIL’s actual production has been lower than its targets (7 per cent lower in 2016-17, 5 per cent lower in 2017-18 and 2.5 per cent lower in the first quarter of 2018-19). The shortages can be roughly equated to the shortfall in CIL’s coal production target, that is, 33 mt (in 2017-18), according to CARE Ratings. Moreover, all plants that reported critical coal stocks were non-pithead, implying that the coal shortages were due to logistical or infrastructural challenges. CIL has had a railway rake availability of 285 to 290 rakes, against a requirement of over 309 rakes a day. The company has also been struggling to transport coal from its sidings into wagons due to the onset of monsoon.

The coal shortage has pushed up merchant power market prices. After two consecutive years of sub-Rs 3 per unit levels, spot prices on the power exchanges firmed up during the year. However, September, October and March witnessed a spurt in demand for short-term power, driving up prices beyond Rs 4 per unit. According to SBICAP Securities, “Due to the shortage of coal at plants supplying power under long-term power purchase agreements, demand has moved to the short-term market. Therefore, merchant plants with design/access to imported coal (as domestic e-auction coal is also under short supply) have been able to capitalise on rising spot market rates.” The power sector’s overall coal requirements are pegged at 615 mt for 2018-19. While the official coal production target is set at 610 mt, CIL recently stated that it is aiming to improve its production level to 652 mt in 2018-19 on the back of high demand.

Outlook

Outlook

The uptrend in coal imports has so far continued in 2018-19 as well. Power plants that blend domestic and imported coal have imported 3.6 mt of coal in the first two months of 2018-19, which is 39 per cent more than the same period in 2017-18. Confirming this trend, another set of estimates (from the American Fuels and Natural Resources) shows that thermal coal imports rose by more than 14 per cent to 43.4 mt in April-June 2018 as compared to a year earlier. Meanwhile, the CEA has supported the government’s view and concluded that government-owned thermal power plants must import coal (about 20 mt) to compensate for domestic coal shortages.

State utilities have already initiated imported coal procurements. The state power utilities of Andhra Pradesh and Tamil Nadu have recently stated that the two states have imported a total of 1.6 mt of coal since the beginning of this year. Andhra Pradesh has imported around 200,000 tonnes of coal till May 2018 and plans to import a total of around 1 mt in 2018. Meanwhile, Tamil Nadu Generation and Distribution Corporation Limited (TANGEDCO) has imported around 1.4 mt of coal in 2018. Maharashtra too has floated a tender for obtaining 1 mt of coal, while Gujarat plans to ramp up imports by 400,000 tonnes this year. Karnataka is also reportedly planning to import coal this year.

What is worrying, however, is that global coal prices have been on a steady rise. Indonesia, India’s biggest source of imports, set its July thermal coal reference price at a six-year high of $104.65 per tonne, an increase of 8.3 per cent month on month and 32.6 per cent from a year ago. Australian thermal coal prices have broken through $120 per tonne for the first time since 2012, driven by strong consumption in Asia. What will further drive up coal import demand, according to analysts, is the proposed pet coke ban for the cement industry, which, if implemented, could lead to a high demand for coking and thermal coal.

Conclusion

According to industry observers, a number of measures will be needed in the medium to long term if India is to maintain its import reduction trajectory. From the ramping up of domestic coal production, auctioning of blocks for commercial coal mining, faster operationalisation of domestic blocks and significant improvement in rail infrastructure to the timely implementation of new rail corridors that would significantly increase transport volumes – a multi-pronged approach would be needed to increase supply. Till then, coal imports remain the only viable option to tide over the shortfall in the near future.