The short-term trading market has become an inevitable part of the power sector value chain and is now positioned as its key pillar. For sellers, including merchant and stressed power plants, the short-term power trading market has emerged as a necessary tool for maximising revenues by selling during higher-value, peak demand hours. While for consumers, especially commercial and industrial (C&I), sourcing power from the short-term market offers significant cost savings by providing electricity at competitive prices and with greater transparency.

During 2020-21, power exchanges performed spectacularly well despite the Covid-19-induced lockdowns; this resulted in a significant reduction in the demand for electricity in the country in the first two quarters of the year. The power exchanges achieved an all-time high volume of 79.59 BUs during the year, leading to 41 per cent year-on-year growth, indicating a significant shift in the Indian power market that has been largely dominated by bilateral deals. The year also saw the introduction of new market segments – the real-time market (RTM) and the green term ahead market (GTAM) – on the power exchanges.

A look at the key trends in power trading volumes and prices during the past year…

Market overview

During 2020-21, the short-term trading volumes were recorded at 146.01 BUs, which accounted for 10.6 per cent of the total generation during the year. The remaining 88.2 per cent power was procured by discoms through long-term contracts and short-term intra-state transactions. The short-term market has shown an increase of 6.5 per cent in 2020-21 over 2019-20, when 137.16 BUs were traded. Since 2015-16, the volume of short-term transactions has grown at a compound annual growth rate (CAGR) of around 4.8 per cent. Meanwhile, power generation has grown at a slower pace, at a CAGR of 3.3 per cent during the period.

Of the total volume transacted in the short-term market during 2020-21, the volumes traded through power exchanges accounted for around 54.5 per cent (79.59 BUs). The remaining share came from volumes transacted through trading licensees, deviation settlement mechanism (DSM) transactions and bilateral transactions between discoms that accounted for shares of 18.3 per cent (26.67 BUs), 15.7 per cent (22.91 BUs) and 11.5 per cent (16.84 BUs) respectively.

Power exchanges

Power exchanges

During 2020-21, an aggregate volume of 79.59 BUs was transacted on the two power exchanges, recording an increase of 41 per cent from the 56.45 BUs recorded in the previous year. Of the total volume, 73.9 BUs were transacted on the Indian Energy Exchange (IEX) while 5.69 BUs were transacted on Power Exchange India Limited (PXIL). The trading volume on the two power exchanges has grown at a CAGR of over 18 per cent from 2015-16 to 2020-21. Despite a nationwide lockdown during March-May 2020 and a reduction in the demand for electricity, especially in the first half of the fiscal, overall volumes on the exchanges grew as new products (RTM and GTAM) were added. Also, discoms and industrial consumers took advantage of the prevailing low prices on the exchanges to optimise their power portfolio.

DAM and TAM: During 2020-21, an aggregate volume of 69.34 BUs was transacted on the two power exchanges in the day-ahead market (DAM) and the term-ahead market (TAM). This was an increase of 22.8 per cent from the 56.45 BUs recorded in the previous year. Of the total volume traded, 60.62 BUs were traded in the DAM, while the remaining 8.72 BUs were traded in the TAM. The DAM is the electricity trading market for delivery on the following day, while the TAM allows delivery of electricity up to a duration of one week.

The IEX accounted for a major share in the DAM as 60.38 BUs (out of 60.62 BUs) were traded on its platform. The IEX’s trading volume in the DAM grew at a CAGR of over 12.2 per cent from 2015-16 to 2020-21. Meanwhile, over 240 MUs of the day-ahead volume were traded on PXIL during 2020-21. In the TAM, a volume of 3.27 BUs was transacted on the IEX platform while 5.45 BUs were transacted on the PXIL platform.

The month-wise trend shows that the weighted average price of electricity on the IEX during 2020-21 ranged from Rs 2.41 per unit to Rs 4.11 per unit in the DAM, and from Rs 2.58 per unit to Rs 3.73 per unit in the TAM. Meanwhile, the monthly weighted average price at the PXIL was Rs 2.53 per unit to Rs 4.19 per unit in the DAM, and Rs 2.54 per unit to Rs 3.79 per unit in the TAM. The lowest price in DAM at both the exchanges was witnessed in June 2020, reflecting lower fuel costs and spare generation capacities. This fall in electricity prices in the spot markets attracted price-sensitive buyers such as state electricity boards, whose financial health had worsened due to Covid.

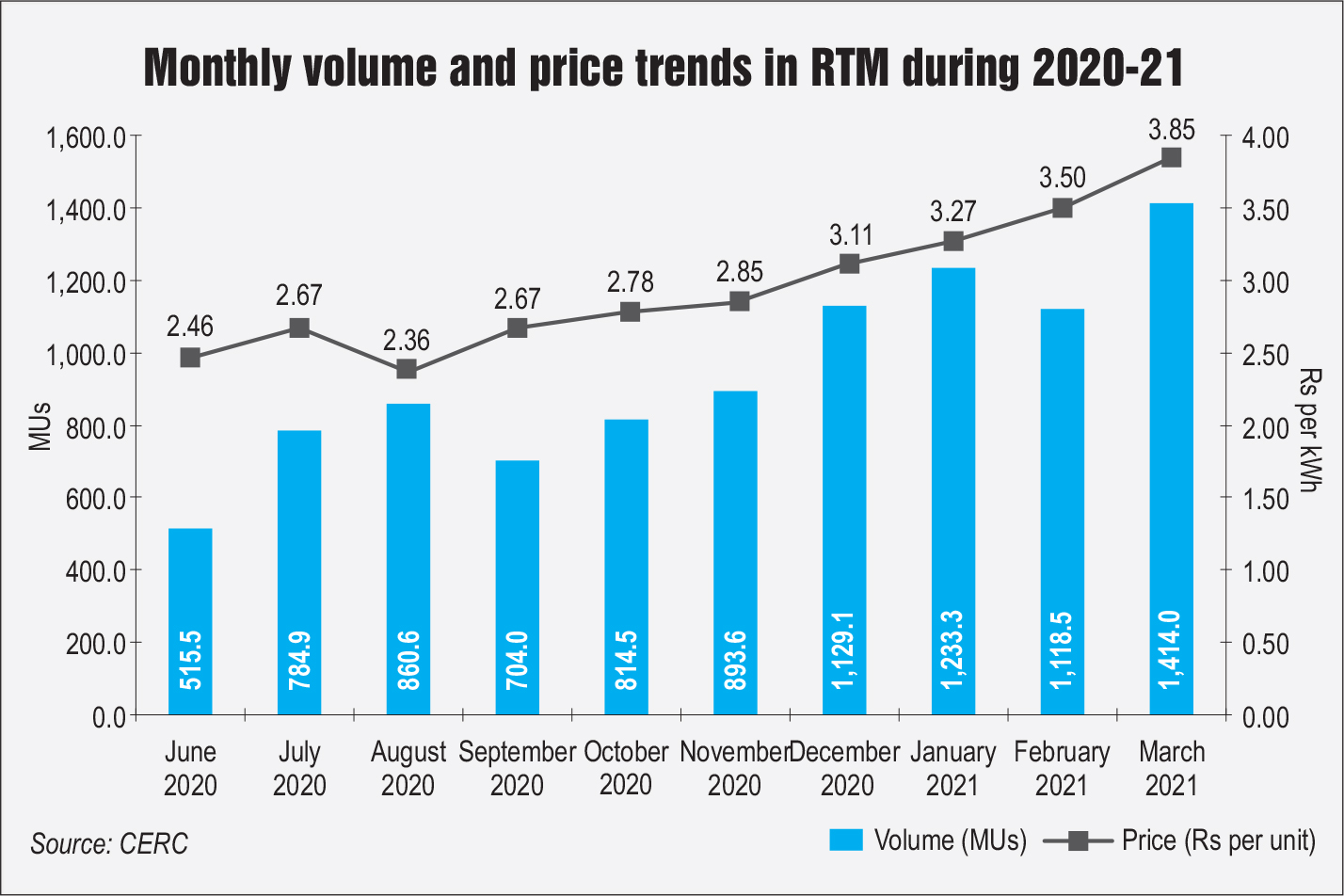

RTM: Launched by the IEX and PXIL in June 2020, the RTM allows 48 sessions of half an hour each in a day, which means the trading of electricity is done round the clock and power delivery can be scheduled at intervals of one hour. The development has allowed utilities and open access consumers to manage power demand-supply variation and meet 24×7 power supply in a flexible, efficient and dynamic way.

Trading in the RTM has exceeded market expectations, with the RTM trading volume recorded at 9.47 BUs during the 10 months of operation in 2020-21. Of this, 99.98 per cent of the volume was traded on the IEX. The RTM accounts for around 12.8 per cent of the IEX’s overall power traded volume during 2020-21 and has been trading over 1 BUs for four consecutive months from December 2020 to March 2021. The RTM has emerged as a “go-to platform” for distribution utilities and industrial consumers to meet their real-time electricity demand-supply balance. The market saw participation from over 400 market participants during March 2021 at the IEX. The month-wise trend shows that the weighted average price of electricity in the RTM during 2020-21 ranged from Rs 2.36 per unit to Rs 3.85 per unit at the IEX, and Rs 2.61 per unit at the PXIL.

GTAM: On August 21, 2020, the IEX commenced trading in the GTAM, which allows renewable energy developers to sell electricity in the short-term market through intra-day and day-ahead contracts in both the solar and non-solar categories, which were later expanded to cover daily and weekly contracts from December 2020. Meanwhile, the PXIL launched the GTAM on its platform on March 24, 2021, offering trade in two types of green term-ahead contracts – intra-day contracts and any-day contracts – in both solar and non-solar segments.

The GTAM has received an encouraging response from market participants. During the eight months of operation in 2020-21, around 785.12 MUs were traded in the GTAM at the IEX. Meanwhile, around 0.39 MUs were traded in the GTAM at the PXIL during March 24, 2021 to March 31, 2021. The month-wise trend shows that the weighted average price of electricity in the GTAM during this period ranged from Rs 3.06 per unit to Rs 4.68 per unit at the IEX, and Rs 4.61 per unit at the PXIL. The IEX has witnessed an average monthly participation of over 30 in the GTAM. The market has enabled distribution utilities, industrial consumers and renewable energy generators to buy and sell green power while also supporting them in fulfilling their renewable purchase obligation (RPO) targets.

Traders

Traders

During 2020-21, about 26.67 BUs of electricity was transacted bilaterally through traders, a decline of 11 per cent as against the 29.95 BUs recorded during 2019-20. Volumes traded through trading licensees have declined at a CAGR of 5.5 per cent during 2020-21 since 2015-16. In 2020-21, the weighted average price of electricity transacted through traders ranged from Rs 3.02 per unit to Rs 4.10 per unit.

Open access consumer participation

A growing number of industrial consumers have turned to power exchanges owing to competitive prices. In 2019-20, over 5,170 open access (OA) consumers procured power through the two exchanges, as compared to around 4,950 consumers in 2018-19. In both the power exchanges, OA industrial consumers bought 14.46 BUs of electricity, which accounted for 29 per cent of the total day-ahead volume transacted in the power exchanges during 2019-20.

At the IEX, around 14.45 BUs were traded in 2019-20 by 4,555 OA consumers at a weighted average price of Rs 2.84 per unit, lower than the weighted average price of Rs 3.16 per unit for the total electricity transacted at the exchange. Meanwhile, around 10 MUs of power was procured by 615 OA consumers at the PXIL at a price of Rs 3.22 per unit, as against the weighted average price of Rs 3.38 per unit for the total electricity transacted at the exchange.

REC trading

REC trading

During 2020-21, the renewable energy certificate (REC) market shrank to 0.92 million RECs on the two power exchanges, as against the trading of 8.92 million and 12.6 million RECs recorded in 2019-20 and 2018-19 respectively. As of March 31, 2021, an inventory of 6.06 million RECs has piled up, which includes 0.77 million solar and 5.28 million non-solar green certificates. This is because REC trading has been suspended since July 2020 after the Appellate Tribunal for Electricity (APTEL) decided to postpone the trading by four weeks while hearing three separate petitions related to an issue of fixing floor and forbearance prices of RECs by the CERC. In June 2020, the CERC issued a suo motu order and fixed the forbearance price at Rs 1,000 per MWh and the floor price at zero for solar and non-solar RECs. In August 2020, the IEX and PXIL sought the reopening of REC trading, but it did not take place during the entire year. This also impacted the ability of distribution companies to meet their RPOs.

The market clearing volume of solar and non-solar RECs was 0.15 million and 0.77 million, respectively, during the three months (from April to June 2021) of trade of 2020-21. Of the total solar RECs, 0.12 million were traded at the IEX while the remaining 0.03 million were traded at the PXIL. Similarly, for non-solar RECs, 0.58 million were traded at the IEX while 0.19 million were traded at the PXIL. The monthly weighted average market clearing price for solar RECs ranged between Rs 1,000 per MWh and Rs 2,400 per MWh on the IEX, and between Rs 1,010 per MWh and Rs 2,000 per MWh on the PXIL. Meanwhile, for non-solar RECs, it was Rs 1,000 per MWh on both the power exchanges.

Regulatory developments

Several key developments took place on the power trading front in the past one year.

Market-based economic dispatch (MBED): In June 2021, the MoP notified a discussion paper on MBED, which envisages a centralised system to route electricity consumption in all states through power exchanges to discover a national uniform price and ensure that the cheapest available power is despatched. The move is expected to lead to significant savings in procurement costs. According to the draft proposal, MBED can yield around 4 per cent savings on an average in power procurement costs.

Redesigning the REC market: The MoP released a discussion paper on redesigning the REC market in June 2021, to align it with emerging changes in the power sector and to promote new renewable energy technologies. The paper proposes to make RECs valid in perpetuity instead of having a validity period. REC holders would have complete freedom to decide on the timing of the sale; therefore, forbearance prices will not be required to be specified. The CERC will need to devise a monitoring and surveillance mechanism to ensure there is no hoarding of RECs and artificial rise in market prices. Renewable energy generators will be eligible for REC issuance over a reduced 15-year period from the commissioning date of the project and the existing renewable energy projects that are eligible to get RECs will continue getting it for 25 years. The last date to submit comments and suggestions on the discussion paper was June 25, 2021.

Draft Ancillary Services Regulations, 2021: The CERC issued the draft Ancillary Services Regulations, 2021 in May 2021 to provide mechanisms for procurement, through administered as well as market-based mechanisms, deployment and payment of ancillary services for maintaining grid frequency close to 50 Hz. The commission has proposed a mechanism to allow load despatch centres to buy power to be used for ancillary services from the spot market through electricity exchanges. For tertiary reserve ancillary service, the NLDC will have to notify power exchanges the quantum of electricity requirement on a day-ahead basis before commencement of the DAM or the RTM.

Power Market Regulations, 2021: In February 2021, the CERC issued the Power Market Regulations, 2021. As per the regulations, the scheduling and delivery of transactions for day-ahead contracts and real-time contracts (including the timeline for gate closure, wherever applicable) shall be in coordination with the NLDC and in accordance with relevant provisions of the Open Access Regulations and the Grid Code. Price discovery shall be done by power exchanges or by the market coupling operator as and when notified by the commission.

Update on electricity derivatives and forwards: In July 2020, the MoP approved trading of electricity through forward and derivative contracts. The Securities and Exchange Board of India (SEBI) is expected to oversee the functioning of all financially traded electricity forwards while the CERC would regulate physically settled forwards, where electricity is delivered on a future date at the contracted price. It is expected that the derivatives market may start functioning in 2022-23 allowing both generators and consumers to use it as a new hedging tool to mitigate price volatility and other associated risks. This will help in expanding the overall structure of the physical delivery market, besides adding electricity as a commodity in the financial market.

New PPA exit guidelines: The MoP notified new guidelines in March 2021, paving the way for distribution utilities to exit power purchase agreements (PPAs) upon expiry of their terms by giving six months’ notice. This is an important development for states that were procuring relatively costly power from central generating stations. Post the discoms’ exit, generating companies will have the flexibility to sell power in any mode – long term, medium term or at the power exchanges. According to industry experts, the move will reduce the power purchase cost of discoms that are bound to buy high-cost power from inefficient old plants. The discoms are also likely to engage in medium- to short-term purchases, including greater procurement through power exchanges, where tariffs can be competitive.

Integrated DAM: In April 2021, the MoP issued letters to the CERC, Power System Operation Corporation (POSOCO) and power exchanges for developing an integrated DAM within power exchanges with separate price formation for renewable energy power and conventional power. The move aims to provide multiple options to market participants in the renewable energy space. The integrated DAM would essentially blend the trading of green and conventional energy and is expected to better the power price discovery as well as improve payment to power generators.

Cross-border electricity trade (CBET): The IEX commenced CBET on its platform from April 17, 2021, a first-of-its-kind initiative which will allow power exchanges to expand their power markets to the South Asia region. This follows the notification of CBET Regulations by the CERC in 2019 and the recent notification of CBET Rules in March 2021 by the Central Electricity Authority (CEA). Currently, the IEX has begun trading of electricity hosting participants from Nepal on its platform. So far, it has traded 150 MUs electricity.

Registration of third power exchange: In May 2021, the CERC approved the registration of Pranurja Solution Limited (PSL) as the third power exchange in India after the IEX and PXIL. PSL was incorporated in 2018 as a consortium of PTC India, BSE Investments and ICICI Bank. PTC India and BSE Investments hold 25 per cent stake each in Pranurja, followed by ICICI Bank, which holds 9.9 per cent. Other shareholders are Greenko Energies (5 per cent), Jindal Power (2 per cent), Meenakshi Power (5 per cent) and six others. PSL has filed a petition for grant of registration to operate a power exchange under Regulation 16 of the CERC (Power Market) Regulations, 2010. PSL has a net worth of Rs 500 million, thus fulfilling the commission’s net worth requirement of Rs 250 million.

Conclusion

In order to encourage consumer-level participation in the short-term power market, the removal of tariff-related barriers such as high cross-subsidy charges levied by discoms needs to be dealt with by state regulators. In the coming months, the restarting of trade in RECs, commencement of trade in energy saving certificates under the Perform, Achieve and Trade (PAT) cycle 2, and launch of new market segments such as longer-duration delivery contracts and the integrated DAM are expected to increase participation in the short-term market. Going ahead, market volumes are also likely to grow as more renewable energy is added to the system and the existing long-term power purchase agreements of discoms expire.

Nikita Gupta