Within the entire power value chain, broadly categorised into generation, transmission and distribution (apart from trading and other allied activities), the primary cash generation takes place at the distribution end, which feeds the entire value chain. Despite being the most critical link in the value chain, this sector has historically seen the maximum distress and most of the players, barring a few urban-centric private players, have always been on the stretcher. Political populism has also compounded the problem.

The Government of India, from time to time, has provided oxygen to the sector, which has ranged from straight bailouts to grants for modernisation and system strengthening (APDRP and RAPDRP), network expansion (DDUJY, RGGVY and Saubhagya) and schemes such as UDAY. While most of these schemes have only partially met their objectives, the need to support the sector continues. The latest in this sequence is the Rs 3.03 trillion Revamped Distribution Sector Scheme (RDSS) launched in July 2021, which includes Rs 976.31 billion worth of central government budgetary support, with the main objective of reducing aggregate technical and commercial losses to between 12 and 15 per cent by the year 2024-25. The scheme has two components:

- Part A – Financial support for prepaid smart metering and system metering and upgradation of the distribution infrastructure.

- Part B – A small component of approximately Rs 2 billion for training and capacity building and other enabling activities.

Various state-owned discoms are utilising the package for system strengthening (RDSS-1) and significant action has also taken place towards modernisation of metering infrastructure (RDSS-2). As with RDSS-1, it may be assumed that the money is being spent on much-needed infrastructure, we shall analyse some of the critical issues involved with RDSS-2.

Previously, the cost of single-phase domestic meter reading and spot billing ranged between Rs 7 and Rs 12 (using a downloadable optical probe or manually with or without photographs). But the entire process had several loopholes and deficiencies, and needed to be modernised. Uttar Pradesh and Haryana’s distribution companies took the bold decision to award contracts for installing 4 million and 1 million smart meters respectively, way back in 2017, for their urban consumers at a cost-plus price, to be paid on monthly meter reads only, which was set at Rs 85.95 plus GST for Uttar Pradesh’s discoms and Rs 86.98 plus GST for Haryana’s discoms. The contracts were awarded to Energy Efficiency Services Limited. The implementation of the project has been slow, and over the past five-and-a-half years, only about 1.2 million smart meters have been installed in Uttar Pradesh (out of 4 million) and 735,000 smart meters in Haryana, as per the latest information.

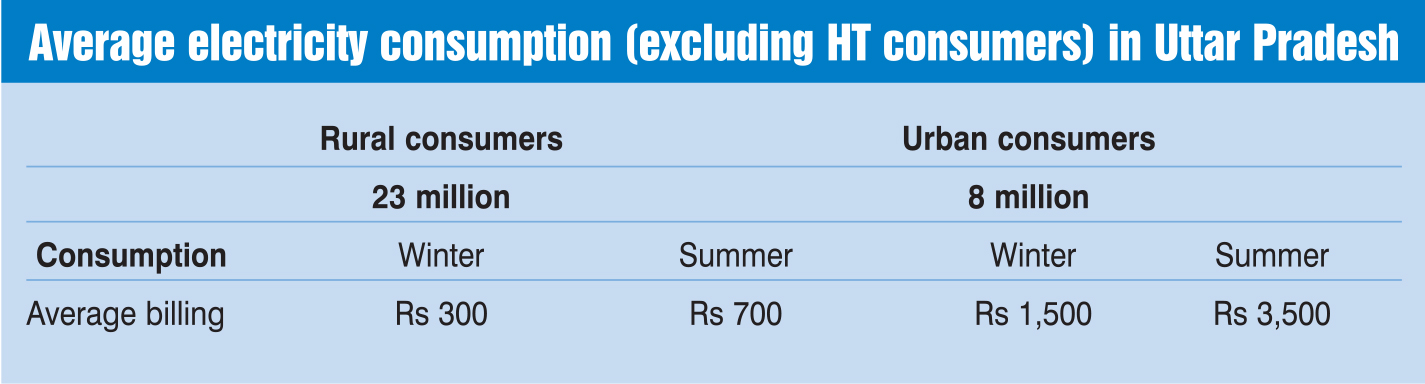

Now, the question is, is the above cost of smart metering justified? The accompanying table gives the data of average billing per month per domestic consumer for Uttar Pradesh’s discoms for the year 2019-20.

It can be safely assumed that in the power distribution business, the cost of bulk power procurement is  about 80-85 per cent of the average billing rate to the end consumer. Add to it line losses of 10-15 per cent (and more), operations and maintenance, and administrative and general expenditure of about 10 per cent, depreciation and taxes. This hardly leaves any room to pay Rs 85.95 plus GST as pure metering cost. Or does it?

about 80-85 per cent of the average billing rate to the end consumer. Add to it line losses of 10-15 per cent (and more), operations and maintenance, and administrative and general expenditure of about 10 per cent, depreciation and taxes. This hardly leaves any room to pay Rs 85.95 plus GST as pure metering cost. Or does it?

The analysis of the billing pattern of consumers who have migrated to smart meters for year 2019-20 for Uttar Pradesh’s discoms reveals that the monthly billing increased by about Rs 216 per consumer per month, making increased investment in smart metering look very attractive. But this proved to be short-lived. The increase in billing for these consumers dropped to only Rs 50 per consumer subsequently. The initial increase was mainly due to the billing of stored readings and more efficient billing. Therefore, the jury is still out on the viability of the cost of smart metering. However, the high cost of smart metering may not be the only determinant. There are a host of other benefits of smart (and smart prepaid) metering, which have been well documented, such as:

Benefits to discoms

- Meter reading gets “automated”, which increases the billing efficiency to nearly 100 per cent. Error-free billing leads to fewer consumer complaints and an increase in the consumer satisfaction index.

- Through the use of data analytics, consumer monitoring and “revenue protection” (vigilance) activities become easier and more targeted.

- In prepaid mode, revenue collection becomes automatic with 100 per cent cash in advance.

- Dealing with “defaulters” becomes much easier due to the auto disconnection/reconnection (RC-DC) facility.

Benefits to consumers

- Electricity consumption can be monitored in real time and even “controlled” by consumers using their smart phone devices.

- Error-free billing “avoids” unwarranted “harassment” caused due to manual billing.

- Faster reconnections on payment, should the supply get disconnected on any earlier payment defaults.

- 24×7 “recharge” facility: Prepaid smart meters can be recharged online through various payment methods. Moreover, discoms are promoting discounts on online recharges.

With smart meters, meter reading gets automated, which increases billing efficiency to nearly 1 00 per cent.

Uttar Pradesh, the largest beneficiary of the RDSS scheme owing to its massive population and consumer base, has recently floated (and awarded) smart metering tenders based on a fixed down payment of Rs 900 per smart meter and the balance to be paid over 8 to 10 years on a per month per meter reading basis. This has been done for the 100 per cent consumer base, including approximately 6.9 million left-out urban consumers and about 22.9 million rural consumers. It may be noted that even after the negotiations, the awarded rates are much higher than the discoms’ own estimates, and the difference varies from 23.62 per cent to 39.43 per cent. During calendar year 2023, Gujarat also awarded contracts for smart meters on the same basis.

Notably, the rates offered by various bidders to Uttar Pradesh’s discoms are much higher than to Gujarat’s discoms. Surprisingly, the difference in rates is steeper for higher-end meters and is almost double for feeder meters. Surely, such a big difference cannot be explained merely by the time-gap of less than six months. The possible reasons could be the realisation by bidders that the terrain of Uttar Pradesh’s discoms is more difficult than that of Gujarat’s discoms, or that Uttar Pradesh is possibly a more difficult place to do business in compared to Gujarat.