Australia has been actively transitioning towards achieving a net zero economy by 2050. The government has increased the interim 2030 emissions reduction goal to 43 per cent (from the 2005 level), supported by an 82 per cent share of renewable energy sources (RES) generation target under the Powering Australia Plan and the Rewiring the Nation policy, with the recent Capacity Investment Scheme (CIS) and Renewable Energy Transformation Agreements (RETAs) supporting those targets. Further, recent state policies support the broader energy transition plan.

Australia’s National Electricity Market (NEM), which has been operating smoothly for the past 25 years, is facing two challenges – the retirement of coal-fired generation, and the electrification of its future transport, heating, cooling, cooking and industrial needs. The transition is progressing steadily, with rapid RES deployment, which will be supplemented by storage and backed up by gas. To efficiently achieve long-term power system needs, the Australian Energy Market Operator (AEMO), in December 2023, released the draft 2024 Integrated System Plan (ISP). Published every two years, the ISP includes an optimal development path (ODP) of generation, storage and transmission investments needed to meet the 2050 energy needs.

The draft plan, which is based on extensive consultations over the past 18 months, considers three scenarios to reach net zero by 2050. Of these, stakeholders have resonated the most with the “Step Change” scenario. To realise the ODP under this scenario, the plan calls for an additional 10,000 km of transmission lines by 2050, which will deliver net market benefits worth AUD 17.45 billion.

A look at recent government policies supporting the energy transition and the key highlights of the draft 2024 ISP.

Recent government policies

In 2023, there was greater government involvement and investment in the electricity sector. It expanded the CIS initiative fivefold to secure 32 GW (from the initial 6 GW) of new wind, solar and storage capacity. It will also negotiate new bilateral RETAs with state and territory governments under the National Energy Transformation Partnership, which is a framework for governments at various levels to collaborate on reforms to achieve net zero. Through collaboration under RETAs, states will ensure the delivery of new RES projects. Notably, over 56 per cent or 18 GW of the CIS capacity will be subject to RETAs.

New South Wales (NSW): At the state level, NSW’s Electricity Infrastructure Roadmap is underpinned by its five renewable energy zones (REZs), which coordinate the connection of transmission infrastructure to new generation and storage facilities across these REZs. The Energy Corporation of NSW is leading the delivery of the first five REZs. Other notable policies of NSW in late 2023 include the release of the draft Energy Policy Framework for RES and transmission infrastructure; the commitment to set up the Energy Security Corporation with funding of AUD 1 billion; and an AUD 800 billion addition to the Transmission Acceleration Facility to expedite the connection of the state’s REZ to the grid.

Queensland: To implement the Queensland Energy and Jobs Plan, the government introduced the Energy (Renewable Transformation and Jobs) Bill in Parliament in October 2023. It seeks to legislate the state’s RES targets of achieving 50 per cent by 2030, 70 per cent by 2032 and 80 per cent by 2035; calls for 100 per cent public ownership of transmission and distribution as well as deep storage assets (mainly pumped hydro storage), and 54 per cent of generation assets by 2035; introduces a priority transmission investment framework for critical infrastructure to be built by the state-owned transmission company Powerlink and a framework for REZs; and includes provisions for the development of the SuperGrid Infrastructure Blueprint by 2025, to be achieved in the decade thereafter. The bill has been referred to a parliament committee, which is expected to submit its response by March 1, 2024.

Victoria: In 2023, the state launched the Victorian Transmission Investment Framework (VTIF) to achieve its ambitious RES target of 95 per cent by 2035 and net-zero emissions by 2045. Victoria will pioneer Australia’s offshore wind (OSW) development, with the state setting a target of 2 GW of OSW capacity by 2032, 4 GW by 2035 and 9 GW by 2040. State-owned VicGrid is leading the planning and development of REZs and associated transmission infrastructure in the state.

Other states: South Australia recently passed the Hydrogen and Renewable Energy Act, 2023 (HRE Act) to implement a licensing and regulatory regime for large-scale hydrogen and RES projects. Tasmania, which is the country’s first and only state to have achieved 100 per cent self-sufficiency in RES and net zero emissions seven years ago, now aims to increase RES to 150 per cent by 2030 and 200 per cent by 2040. Meanwhile, Western Australia announced a new legislative exemption to cut environmental approval time frames as part of its AUD 22.5 million Green Energy Approvals initiative.

Future demand scenarios

The latest ISP considers three future demand scenarios through 2050 – Step Change, Progressive Change, and Green Energy Exports – based on varying rates of emission reduction, electricity demand and decarbonisation. The Step Change scenario fulfils Australia’s emission reduction commitment in a growing economy, the Progressive Change scenario reflects slower economic growth and energy investment, and the Green Energy Exports scenario considers very strong industrial decarbonisation and low-emission energy exports. All three scenarios align with the government’s net zero commitments and acknowledge that coal will continue to be phased out over the coming years. After extensive consultation, the AEMO concluded that Step Change should be the ISP’s most likely scenario.

Under this scenario, to realise the ODP, the draft ISP calls for investment that would almost triple grid-scale RES generation capacity by 2030 (to 57 GW) and increase it sevenfold by 2050 (to 126 GW); add almost four times the firming capacity from despatchable storage, hydro and gas-powered generation by 2050 (amounting to 74 GW); and support a fourfold increase in rooftop solar capacity by 2050 (equivalent to 72 GW). Further, energy consumption is expected to increase from 180 TWh currently to over 260 TWh by 2030 and over 420 TWh by 2050.

The AEMO forecasts that coal will completely exit the energy market by 2038, five years ahead of the date in its 2022 ISP. Notably, 90 per cent of the current 21 GW of coal capacity would be retired much earlier, by 2034-35. In light of this, the need for RES has increased to 6 GW per year in the coming decade compared to 4 GW forecasted in the 2022 ISP. Wind is expected to dominate installations till 2030, and by 2050, grid-connected solar will be 55 GW and wind 70 GW. The draft has increased backup gas-powered generation capacity to 16 GW by 2050, up from 10 GW in the 2022 ISP. Further, 50 GW/654 GWh of despatchable storage is expected by 2050.

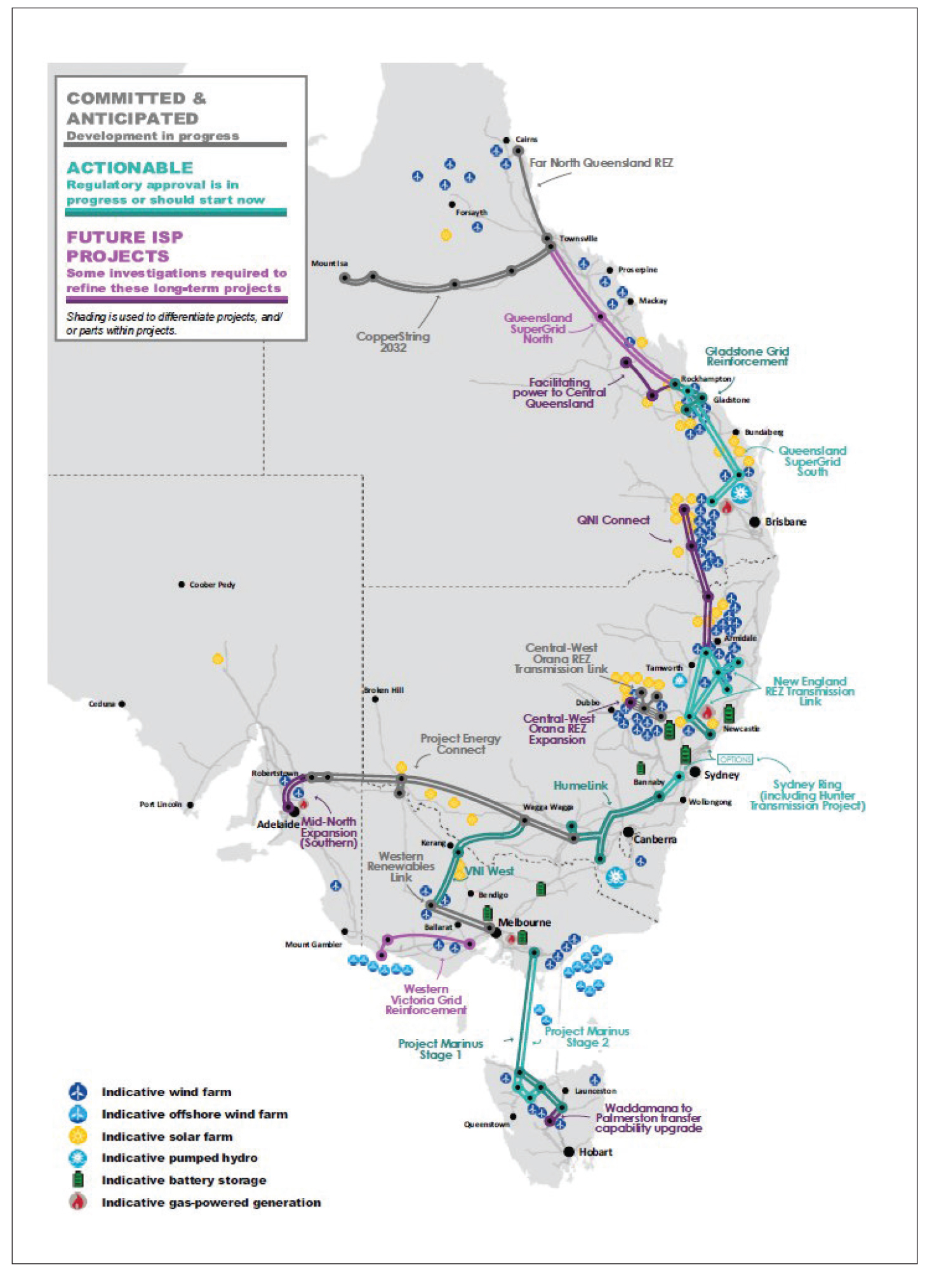

Optimal development path for transmission

Optimal development path for transmission

The ODP largely consists of the same key projects as in the 2022 ISP. Some of the projects have become operational, including the Queensland-NSW Interconnector Minor upgrade (QNI Minor), Victoria-NSW Interconnector Minor upgrade (VNI Minor) and Eyre Peninsula Link.

Overall, by 2050, around 10,000 km of lines are needed under the Step Change and Progressive Change scenarios, and double that amount is needed under the Green Energy Exports scenario. In the interim, by 2030, about 5,000 km is needed, including approximately 4,000 km of new transmission lines and upgrading about 1,000 km of existing lines.

Five committed and anticipated projects are under way for delivery, comprising about half of the 5,000 km of lines to be delivered in the next decade. Queensland’s CopperString 2032 is a newly committed transmission project meanwhile the planned capacity for the Central-West Orana REZ transmission link has been increased to 6 GW from 4.5 GW previously. These projects are expected to be at full capacity by the end of 2029.

Five projects remain actionable and are advancing, while two future projects have progressed to actionable status – Queensland’s SuperGrid South (formerly Central to Southern Queensland) and Gladstone Grid Reinforcement. In NSW, the New England REZ extension and further augmentation are now included as stages in the New England REZ Transmission Link project. Work on these projects should commence or continue as soon as possible under the ISP framework or the relevant state approvals framework. The seven projects will provide another 2,500 km of the needed transmission and are expected to be at full capacity by the end of 2032.

A set of 13 future ISP projects has been identified across states, including an interconnector between Queensland and NSW. The AEMO may require proponents to undertake preparatory activities to enable a more detailed consideration in the next ISP. AEMO considers optimal timings for these projects to give greater market certainty and enhanced power system reliance as coal is retired. This allows time for appropriate community co-design of project implementation and provides flexibility in the procurement of expertise, materials and equipment. The actual delivery dates are, however, to be decided by transmission network service providers.

It is observed that supply chain issues and workforce shortages have resulted in high costs for power projects in recent years, including an increase of around 30 per cent for transmission projects. The AEMO expects transmission project costs to continue to increase beyond the rate of inflation as the sector adapts to market pressures and also to account for environmental and land costs. In fact, the net market benefits of transmission investment have reduced by 37 per cent from AUD 27.7 billion under the 2022 ISP due to an increase in costs, updates to energy policies, commitment to transmission projects whose benefits are now assumed and not included in the total, and lower gas prices.

Challenges and the way forward

In January 2024, the AEMO’s NSW agency AEMO Services cautioned that the country could at most install 4 GW of new clean energy capacity annually, compared to the 6 GW target. It has acknowledged the challenges in implementing the ISP, recognising that energy transition is complex. These challenges include the safe and reliable operations of NEM during the transition, integration of new technologies, maintaining affordability and keeping pace with the global decarbonisation drive. The AEMO has called for grid investments to take place well ahead of when the infrastructure is needed. It highlighted the necessity of garnering support from involved stakeholders, particularly landowners and traditional owners, to mitigate risk to the stability of the nation’s power systems as coal-based capacities are retired. The draft 2024 ISP is open to stakeholders’ feedback with written submissions due before February 16, 2024. Thereafter, the AEMO will finalise the 2024 ISP by June 28, 2024.

The country’s energy transformation relies on the accelerated development of the proposed REZs and the grid of the future. The whole-of-system planning under the ISP will help the industry, investors, governments and communities to plan for the decarbonisation of the power system in the coming years.