As the country shifts towards cleaner energy sources and energy demand rises, hydropower, especially pumped storage, is gaining significant traction, particularly for enhancing system flexibility. Hydropower plays various roles such as peak load management, regulation, frequency response and reserve support. Recent policy initiatives, including the waiver of inter-state transmission system (ISTS) charges for hydroelectric plants (HEPs) and the central government’s guidelines for pumped storage plants (PSPs), are expected to invigorate the sector in the next few years.

Size and growth of the hydropower segment

Large hydro

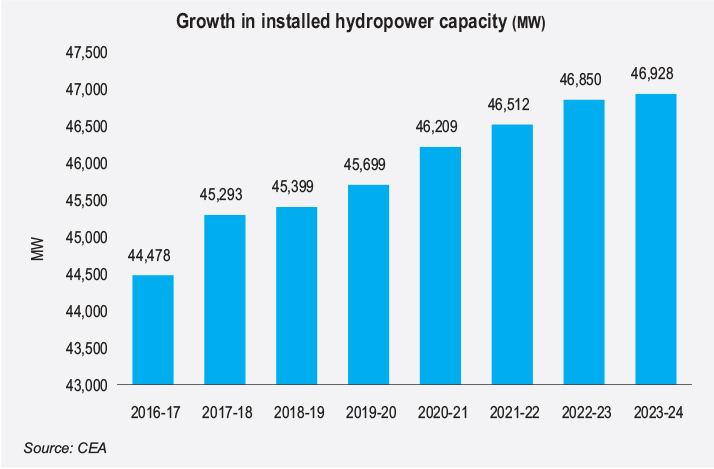

The installed large hydropower capacity (above 25 MW) in the country stood at 46,928 MW as of March 2024. The share of hydropower in the country’s total installed capacity is 11 per cent. The Central Electricity Authority (CEA) estimates the hydroelectric potential at 145,320 MW, of which only 32 per cent has been tapped. During the past five years (2019-20 to 2023-24), only 1,229 MW of hydropower capacity was added. In 2023-24, 78 MW of capacity was commissioned, including SJVN Limited’s Naitwar Mori Units 1 and 2 (2×30 MW) and uprating of BBMB’s Bhakra Left HEP Unit 1 from 108 MW to 126 MW.

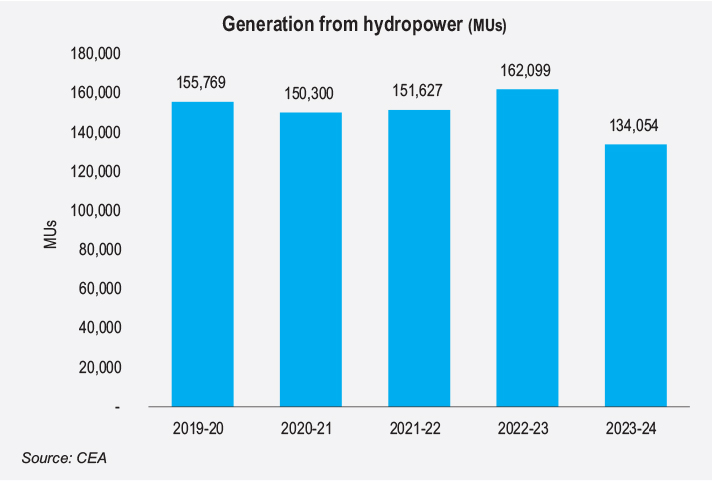

Based on the CEA’s generation data, erratic rainfall led to a fall in hydropower electricity generation recorded during 2023-24, which was only 134.05 billion units (BUs), 17.76 per cent lower than 162.99 BUs in the previous year. Its share in the total power generation dipped to 9 per cent in 2023-24 from 11 per cent in the previous fiscal.

Small hydro

India possesses significant small-hydro power (SHP) potential (25 MW and below) of about 19,749 MW, but less than 20 per cent of this capacity has been utilised, primarily due to challenges in remote site locations and the associated costs of transmission infrastructure. The total installed SHP capacity stands at 5,003.25 MW as of March 2024. The total generation from SHP plants in 2023-24 was 9,485.04 million units (MUs), 15 per cent lower than the 11,170.61 MUs recorded in the previous fiscal.

Policy initiatives

In April 2023, the Ministry of Power (MoP) notified guidelines for pumped storage hydropower projects (HPPs), considering the significant role of PSPs in stabilising the grid and meeting the peaking power demand. It provides recommendations for the PSP market, PSP policies and safe PSP development. It includes aspects such as the monetisation of ancillary PSP services to meet critical electricity market requirements; reimbursement of the state GST tax, or exemption of fees on land acquisition for off-river PSPs; removal of an upfront premium for project allocation; and the identification and safe development of exhausted mines for prospective PSP sites.

In a key development in May 2023, the waiver of ISTS charges was extended to PSPs for which construction work was awarded up to June 30, 2025, subject to certain conditions. Subsequently, partial waiver of ISTS charges, in steps of 25 per cent from July 1, 2025 to July 1, 2028, was extended for PSPs where construction work was awarded up to June 30, 2028.

In June 2023, the timeline for the concurrence of detailed project reports (DPRs) for other PSPs was reduced from 125 days to 90 days to expedite the process. The identified potential of PSPs in the country is about 119 GW (comprising 109 PSPs). Out of this, eight projects (4.7 GW) are under operation, four projects (2.8 GW) are under construction and two have received concurrence from the CEA (2.3 GW), with construction slated to start shortly. Further, 33 projects (42 GW) are under survey and investigation for the preparation of DPRs.

In March 2023, the CEA published revised guidelines for the formulation and concurrence of DPRs for PSPs. These guidelines reduce the timeline for the concurrence of DPRs from 90 days to 50 days for PSPs awarded under Section 63 of the Electricity Act, 2003 (tariff determined by bidding), PSPs that are part of integrated renewable energy projects including wind and solar energy, and PSPs being developed as captive or merchant plants.

Earlier, in September 2023, the central government constituted a standing technical committee to assess issues arising from geological surprises in HEPs, and to examine any additional time or cost involved. The committee will prepare biannual reports for the MoP and has the flexibility to include additional members for specific projects when necessary.

Project updates

Project updates

In April 2024, REC Limited signed an agreement with Chenab Valley Power Project Private Limited (CVPPPL), under which REC will provide CVPPPL with financial assistance of Rs 18.69 billion as term loan for the greenfield 4×156 MW Kiru HEP in Kishtwar district of Jammu & Kashmir.

In March 2024, the central government inaugurated the 2,880 MW Dibang multipurpose hydropower project of NHPC Limited in the Lower Dibang Valley district of Arunachal Pradesh. To be built at a cost of over Rs 318.75 billion, the Dibang project will be the highest dam structure in the country. The project will generate 11,223 MUs of hydropower every year, which will be fed into the northern grid. With a construction period of 108 months, the project is scheduled to be commissioned in February 2032. Meanwhile, in June 2023, NHPC Limited achieved a major milestone in the Subansiri Lower HEP, reaching the dam’s top elevation of level 210 metres in all blocks.

To expedite project development, over 5 GW of projects in the Northeast were handed over to SJVN Limited in July 2023. These are the Etalin HEP (3,097 MW), Attunli HEP (680 MW), Emini HEP (500 MW), Amulin HEP (420 MW) and Mihumdon HEP (400 MW). The development of these projects will involve an investment of over Rs 500 billion.

Meanwhile, the pumped storage segment pipeline is growing. Important MoUs have been signed in the past year to set up PSPs. These include an MoU signed between NHPC and Gujarat Power Corporation Limited for a substantial investment in the proposed 750 MW Kuppa pumped hydro storage project; an MoU between the Uttarakhand government and JSW Energy to establish two PSPs with a combined capacity of 1,500 MW in Almora over the next six years; an MoU between Tata Power and the Maharashtra government for two 2,800 MW of PSPs; and an MoU between NHPC Limited and Andhra Pradesh Power Generation Corporation Limited for two PSPs.

Regarding cross-border HEPs, in June 2023, SJVN Limited signed a project development agreement for the 669 MW Lower Arun HEP to be located in the Sankhuwasabha and Bhojpur districts of Nepal. The project will be constructed in five years at a cost of Rs 57.92 billion with a levellised tariff of Rs 4.99 per unit. In addition, SJVN is executing the 900 MW Arun-3 HEP, which is at an advanced stage of construction, and the 490 MW Arun-4 HEP. In June 2023, NHPC Limited and Nepal’s Vidhyut Utpadan Company Limited signed an MoU for the development of the 480 MW Phukot Karnali HEP in Nepal.

Challenges and future outlook

Challenges and future outlook

According to CEA data, there are currently 32 projects under active construction with a cumulative capacity of 16,737.5 MW. This includes 12,056 MW from the central sector, 3,091.5 MW from the state sector and 1,590 MW from the private sector. According to the CEA’s National Electricity Plan 2023, large hydro is poised to contribute approximately 17 per cent to the country’s projected renewable energy capacity (over 344 GW) by 2026-27. Further, in the medium term (2022-27), the upcoming capacity includes 10,814 MW of conventional hydro projects and 2,700 MW of PSPs, while in the 2027-32 period, around 9,982 MW of conventional hydro and 19,240 MW of PSP capacity additions are expected.

However, to expedite capacity addition in this sector, it is crucial to address challenges. Fully developing India’s hydroelectric potential is technically viable but faces various hurdles. These include issues regarding water rights, environmental considerations, the lack of financially robust civil contractors, challenges linked to resettlement and rehabilitation, and unforeseen geological conditions. These factors frequently lead to significant delays and cost overruns for HEPs.

Akanksha Chandrakar