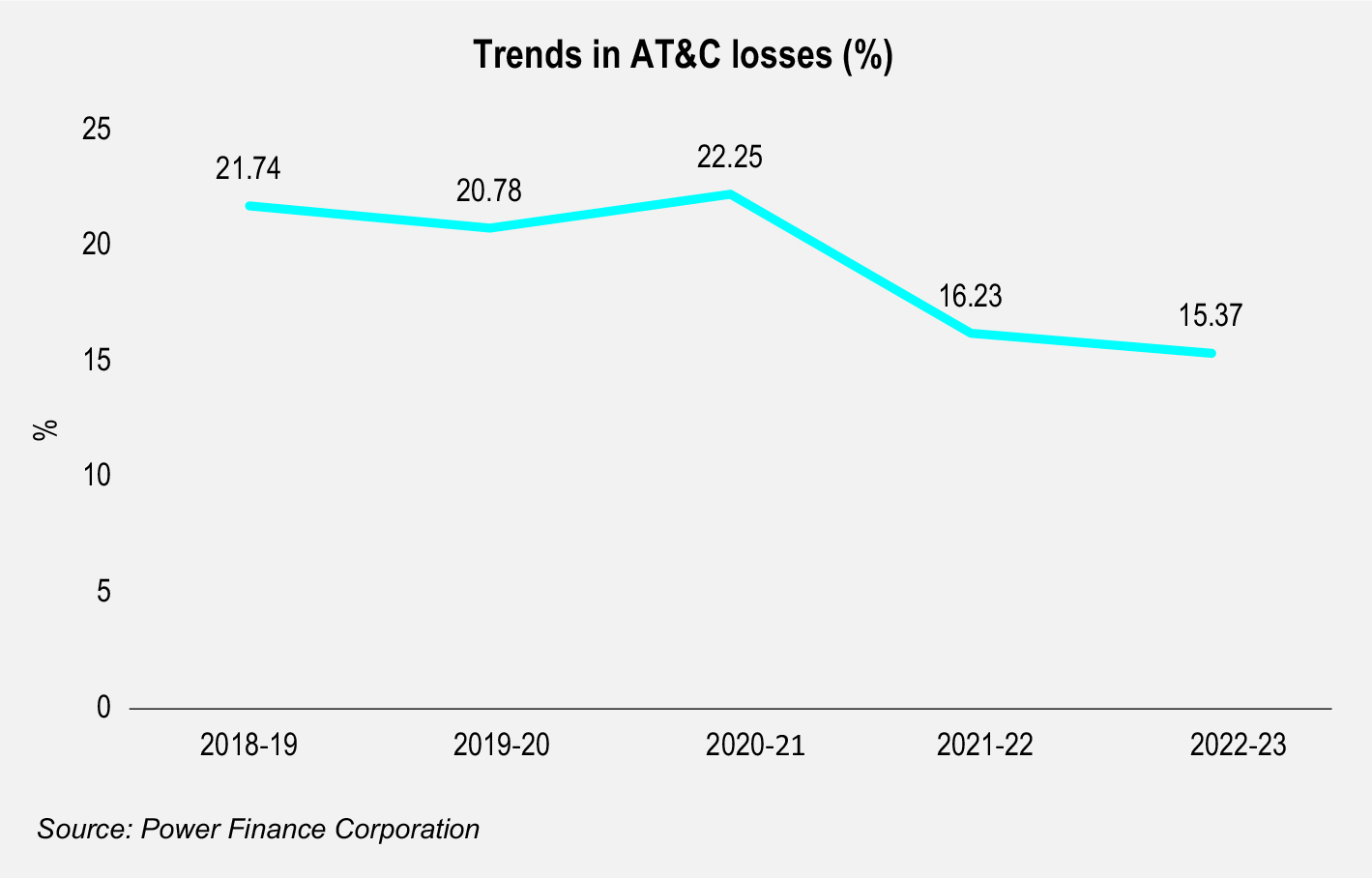

A robust power distribution system is crucial for achieving the country’s ambitious renewable energy goals and meeting the growing power demand. The operational and financial performance of discoms remains an area of concern although there has been some improvement in recent years. As per the Power Finance Corporation’s (PFC) Report on the Performance of Power Utilities, the aggregate technical and commercial (AT&C) losses decreased from 16.23 per cent in 2021-22 to 15.37 per cent in 2022-23. This can be attributed to the implementation of various government policies to improve the power distribution segment’s performance. A key initiative is the Revamped Distribution Sector Scheme (RDSS), with a budget of Rs 3 trillion, aimed at improving the operational efficiency and financial viability of discoms through result-oriented financial assistance. In addition, significant policy and regulatory initiatives have been taken, including the Electricity Rights of Consumers Rules, the implementation of green tariffs and the development of electricity markets. These efforts aim to bring discipline into the sector, improve the tariff structure and empower consumers.

Size and growth

The distribution network has been growing steadily in terms of line length and transformer capacity. As per the Central Electricity Authority (CEA), the total number of power substations (66/11 kV, 33/11 kV and 22/11 kV) in the country was 39,965, as of March 31, 2022, with a total installed capacity of 482,810 MVA. The total number of feeders (66 kV/33 kV/22 kV) stood at 36,804 in March 2022 and the length of the feeder infrastructure was 589,304 ckt km. The country had 230,979 feeders at the 11 kV level with a combined length of 4,935,279 ckt km. It had 1.47 million distribution transformers, with a combined capacity of 6.89 million MVA during the same period. The low-tension power grid comprised 2,231,495 km of single-phase lines and 5,714,263 km of three-phase lines.

As per NITI Aayog, the total energy sales stood at 1,117.9 billion units (BUs) in 2022-23. The domestic category consumers accounted for the maximum share of around 32 per cent at 355.8 BUs (over 331.6 BUs in 2021-22), followed by industrial consumers at 30.4 per cent or 340.2 BUs (compared to 330.26 BUs in 2021-22).

In 2023-24, the energy supply exhibited a clear uptrend, growing strongly. The energy requirement was 1,626 BUs, 8 per cent higher year on year. The peak demand also grew more than 12 per cent year on year, with the all-India peak demand (243 GW) surpassing the peak supply (240 GW). From April 2023 to March 2024, around 4 BUs of energy was not supplied as per the requirement while around 3 GW of all-India peak demand was unmet.

Operational and financial performance

As per PFC’s Report on the Performance of Power Utilities, the aggregate losses of distribution utilities increased from Rs 269.47 billion in 2021-22 to Rs 572.23 billion in 2022-23.

Meanwhile, the tariff subsidy billed by distribution utilities increased from Rs 1,444.69 billion in 2021-22 to Rs 1,695.32 billion in 2022-23. The tariff subsidy released by the state governments as a percentage of tariff subsidy billed by distribution utilities continues to be above 100 per cent at 108.08 per cent in 2022-23. The revenue gap on a tariff subsidy billed basis widened from Re 0.20 per kWh in 2021-22 to Re 0.39 per kWh in 2022-23, while the gap on a tariff subsidy received basis, excluding regulatory income and revenue grant under UDAY for loan takeover, deteriorated from Re 0.10 per kWh in 2021-22 to Re 0.46 per kWh in 2022-23.

Receivables from power sales improved from 138 days of sale as of March 31, 2022 to 119 days as of March 31, 2023. Further, payables for the purchase of power improved from 168 days of sale as of March 31, 2022 to 128 days as of March 31, 2023.

The total outstanding debt of distribution utilities increased from Rs 6,148.53 billion as of March 31, 2022 to Rs 6,843.79 billion as of March 31, 2023. As per the PRAAPTI portal, accessed on June 12, 2024, the total outstanding dues of discoms to gencos comprised balance legacy dues of Rs 289.7 billion and current dues of Rs 632.65 billion.

On the operational performance front, AT&C losses dropped to 15.37 per cent in 2022-23, almost 6 per cent lower than 2018-19 levels. This was driven by an improvement in collection efficiency, from 92.77 per cent in 2020-21 to 97.27 per cent in 2022-23. Meanwhile, billing efficiency improved from 86.13 per cent in 2021-22 to 87 per cent in 2022-23.

As per the 12th Annual Integrated Rating and Ranking of Power Distribution Utilities report, the financial deficit in the power distribution sector widened to Rs 790 billion in financial year 2023, primarily driven by an 8 per cent increase in the gross input energy and a substantial rise in power purchase costs during the year. The absolute cash gap also increased from Rs 440 billion in financial year 2022 to over Rs 790 billion in financial year 2023, driven by the increasing average cost of supply and average realisable revenue gap.

The total sectoral debt increased by 11 per cent, from Rs 6.17 trillion in financial year 2022 to Rs 6.87 trillion in financial year 2023. The average power purchase costs during financial year 2023 rose by 71 paise per kWh from financial year 2022, as compared to the marginal increase of 4 paise per kWh in financial year 2022 over that in financial year 2021.

Key developments

Key developments

Electricity (Late Payment Surcharge and Related Matters) (Amendment) Rules, 2024: In February 2024, the Ministry of Power (MoP) notified the Electricity (Late Payment Surcharge and Related Matters) (Amendment) Rules, 2024. The amendments allow long-term power generators to sell power in the short-term market, allowing power generators to explore additional avenues for selling their generated power beyond their long-term contracts. Power generators that do not offer their surplus power will now not be eligible to claim capacity or fixed charges corresponding to that surplus quantum. Further, the surplus power cannot be offered for sale in the power exchange at a price of more than 120 per cent of the energy charge plus applicable transmission charge.

Electricity (Second Amendment) Rules, 2024: In January 2024, the MoP incorporated provisions for subsidy accounting and payment and the framework for financial sustainability. As per these amendments, discoms are now required to provide quarterly reports with detailed information about subsidy payments. The amendment also introduces procedures for allowing the transfer of expenses incurred by distribution licensees for the creation and upkeep of distribution assets.

Amendment to Electricity (Rights of Consumers) Rules: In February 2024, the MoP notified the Electricity (Rights of Consumers) Amendment Rules, 2024, reducing the timeline for obtaining new electricity connections and simplifying the process of setting up rooftop solar installations. The rules have granted exemptions from conducting a technical feasibility study for systems up to 10 kW. For systems with a capacity higher than 10 kW, the timeline for completing the feasibility study has been reduced from 20 days to 15 days.

Future outlook

The CEA, in collaboration with distribution utilities, has formulated the Distribution Perspective Plan up to fiscal year 2029-30. According to the 20th Electric Power Survey, the country’s peak electricity is projected to rise to 334,811 MW by 2029-30, demonstrating a compound annual growth rate of 6.45 per cent from 2021-22 to 2029-30.

The total power substation capacity (66/11 kV, 33/11 kV and 22/11 kV) in the country is expected to increase to 624,332 MVA by 2029-30. During 2022-23 to 2029-30, 12,192 substations with a total capacity of 141,522 MVA are expected to be added. The plan aims to add 92,920 new 11 kV feeders with a total length of 968,503 ckt km between 2022-23 and 2029-30. This will bring the total number of 11 kV feeders to around 323,899 and increase the overall network length to approximately 5,903,782 ckt km.

An addition of 46.5 million new distribution transformers (DTs) has been planned between 2022-23 and 2029-30. This represents a substantial increase in DT capacity, bringing the total to 9.28 million MVA by the end of the decade.

Based on details received from utilities, about Rs 4.28 trillion will be required for upgrading the distribution infrastructure during 2022-27, of which about Rs 1.89 trillion will be available to discoms, including funds sanctioned under the RDSS. The available funds will constitute around 44 per cent of the total investment required up to 2027. About Rs 2.86 trillion will be required for the upgradation of the distribution infrastructure during 2027-30, taking the total investment required to Rs 7.42 trillion during 2022-30.

Going forward, there are ambitious plans to build a robust distribution network. With peak demand projected to rise, the draft distribution plan outlines infrastructure expansion strategies to ensure sufficient capacity, with a strong emphasis on renewable energy sources.