India’s power sector is shifting from long-term generation contracts to short-term and spot electricity markets, driven by factors such as falling solar and wind costs, national renewable energy targets, renewable purchase obligations, coal allocation flexibility and efforts to improve discom finances. The power trading segment has experienced significant growth over the past year, driven by increasing demand and policy reforms aimed at enhancing market efficiency. In 2023-24, the total volume of power traded exceeded 239 billion units (BUs), indicating a maturing of the market, providing greater liquidity and flexibility for participants.

Furthermore, initiatives promoting market coupling are expected to enhance power trading volumes and open new opportunities for market participants.

Power exchange segment and bilateral transactions

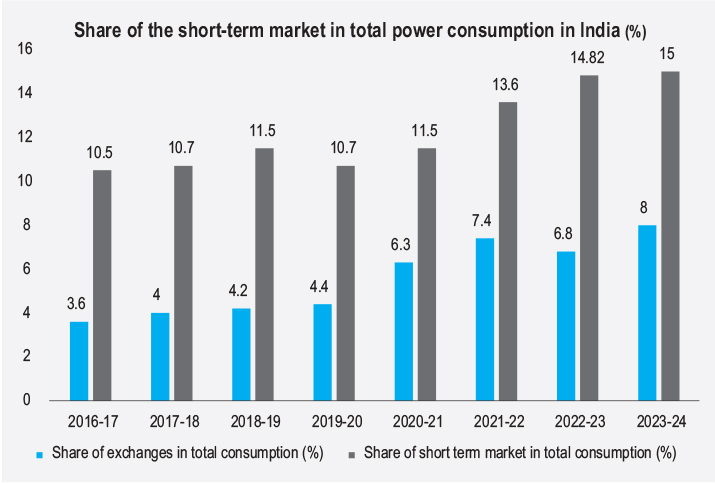

During 2023-24, a total of 1,617.04 BUs of electricity was supplied, of which 239.09 BUs was transacted through short-term trading, marking a 7.37 per cent increase over that in the corresponding period of the previous year. These volumes accounted for 14.78 per cent of the total generation during this period. Further, in short-term trading, 123.11 BUs (51.49 per cent) were traded through the three power exchanges – Indian Energy Exchange Limited (IEX), Power Exchange India Limited (PXIL) and Hindustan Power Exchange (HPX). Bilateral trade constituted 86.96 BUs (5.37 per cent) and the remaining 29.01 BUs (12.13 per cent) were transacted through deviations. The bilateral trade included transactions through traders (59.19 BUs) and direct transactions between discoms (25.98 BUs).

In the day-ahead market (DAM), a total volume of 53.55 BUs were transacted across the three power exchange platforms during 2023-24, an increase of 4.26 per cent over that in the previous year. The IEX accounted for a major share in DAM, with a trading volume of 53.38 BUs, while PXIL accounted for 0.078 BUs and HPX accounted for the remaining volume.

The real-time market (RTM) saw an increase in volume transacted in 2023-24, reaching 27.64 BUs from 24.18 BUs in 2022-23, an increase of 14.31 per cent. The IEX accounted for a major share in RTM, with a trading volume of 27.58 BUs, while PXIL accounted for 0.027 BUs and HPX accounted for 0.025 BUs.

The term-ahead market (TAM) recorded a volume of 19.7 BUs in 2023-24, a decrease of 8.41 per cent compared to 21.51 BUs in 2022-23. In the green TAM, an aggregate volume of 0.33 BUs was transacted during 2023-24 across the three power exchange platforms compared to 2.56 BUs in 2022-23.

The green day-ahead market (GDAM) witnessed a total transaction volume of 2.49 BUs traded on the IEX, while no transactions took place on PXIL and HPX. The total volume of electricity transacted in power exchanges under GDAM during 2022-23 was 3.817 BUs.

During 2023-24, a total volume of 0.95 BUs was transacted in the green-term-ahead market (GTAM) on the three power exchange platforms, a 77.33 per cent decrease over the aggregate volume of 4.19 BUs transacted in the previous year. Of the total, around 0.73 BUs was traded on the IEX, while PXIL accounted for 0.19 BUs and HPX ac¬counted for the remaining 0.52 BUs.

During 2023-24, an aggregate volume of 32.97 BUs was transacted on the three power exchange platforms under the term-ahead market (TAM), an increase of 69.95 per cent over the previous year, wherein an aggregate volume of 19.4 BUs was transacted. Of the total traded volume, the IEX accounted for approximately 14.94 BUs, while PXIL accounted for 8.68 BUs and the remaining 9.35 BUs was traded by HPX.

Electricity traded through traders was recorded at 59.19 BUs during 2023-24, accounting for 24.76 per cent of the total transaction volume in the short-term market. This marked an increase of 75.12 per cent from 33.8 BUs recorded in the previous financial year.

Trading in certificates

Trading in certificates

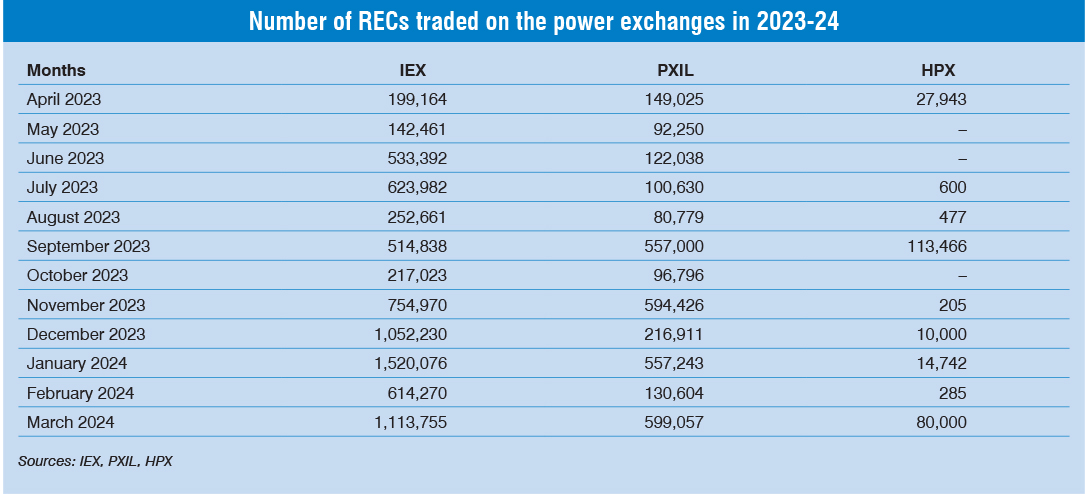

Renewable energy certificates: In 2023-24, renewable energy certificate (REC) trading reached 7.5 million certificates, a 27 per cent increase from that in the previous year. Since the introduction of new REC regulations, prices have become more competitive, hitting an all-time low of Rs 140 in June 2024, compared to Rs 1,000 in April 2023. These changes are expected to further encourage obligated entities to purchase RECs and fulfil their renewable purchase obligations.

Energy saving certificates: The Perform, Achieve and Trade mechanism is a market-driven initiative to boost industrial energy efficiency. Designated consumers are set efficiency targets, earning energy saving certificates (ESCerts) if they exceed them. Those who fall short must buy ESCerts to offset their deficit. During 2023-24, 0.86 million ESCerts (equivalent to 855 MUs) were traded on the IEX, at the floor price of Rs 1,840 per ESCert as compared to a total of 0.18 million ESCerts traded in the previous year, marking an increase of 378 per cent.

Open access consumer participation

On the power exchanges, open access (OA) industrial consumers bought 7.6 BUs of electricity, which accounted for 9.6 per cent of the total DAM, GDAM and RTM volume transacted during 2022-23. OA consumers at the IEX and PXIL stood at 5,159 and 769 in 2022-23 respectively, as of March 2023. HPX, which started in July 2022, had 239 OA consumers in 2022-23, constituting 49.5 per cent of its portfolio. The weighted average price of electricity bought by OA consumers at the IEX was Rs 3.92 per kWh, lower than that of the total electricity transacted on the IEX (Rs 5.90 per kWh), through DAM, GDAM and RTM.

Regulatory updates

Regulatory updates

Cross-border trading

Recently, in August 2024, the Ministry of Power (MoP) revised the Guidelines for Import/Export (Cross Border) of Electricity, 2018. The amendments included proposed changes to the rules governing power exports by coal and gas-based power stations. Further, the ministry has introduced changes to provisions for stations that exclusively supply power to neighbouring countries. As per the guidelines, generating companies and distribution companies in India may export electricity generated from coal, renewable energy, or hydropower plants to neighbouring countries, either directly or through Indian trading licensees, subject to approval from the designated authority. Under the amendments, such exports are allowed only if the electricity is generated using imported coal, spot e-auction coal, coal from commercial mining, or other sources specified by the government. However, these restrictions do not apply to collective transactions on power exchanges in India. For gas-based power plants, exports are allowed only if the electricity is generated using imported gas or other approved sources. In addition, the new guidelines allow these generating stations to connect to the Indian grid (interstate or intra-state) to sell power within the country, if there is a sustained non-scheduling of full or partial capacity, or if a default notice is issued by the generator for any reason, including delayed payments under the power purchase agreement.

In July 2023, the Central Electricity Authority issued amendments to facilitate the cross-border transfer of power through the RTM segment of India’s power exchanges. As per the amendment, any Indian power trader, on behalf of any entity of a neighbouring country, may trade in the Indian power exchanges (in the DAM/RTM/both DAM and RTM segments), after obtaining approval from the designated authority, up to a specified quantum (MW) and duration, provided that the entity, on behalf of which the Indian power trader is trading, belongs to a neighbouring country that has signed an agreement for cooperation with India in the power sector, and the generating asset from which the power is being traded is also owned/controlled by the same country.

Market coupling

In February 2024, the Central Electricity Regulatory Commission (CERC) issued a suo moto order, directing Grid India to implement a shadow pilot model for the coupling of power markets. The proposed shadow pilot seeks to couple three markets on the power exchanges – the RTM of the three power exchanges, separately coupling the RTM with security constrained economic despatch (SCED), and coupling DAM of the three power exchanges. This pilot is expected to help in evaluating the operational, market and regulatory consequences prior to undertaking a full-scale implementation.

In January 2024, the CERC initiated a pilot study on market coupling. The study focuses on coupling of RTM and DAM with SCED and analyses its consequences on the market, regulatory and operations before implementing it. The commission used power exchange bid data to simulate the impact of market coupling, showing slight improvements in economic surplus, cleared volumes and market efficiency, particularly in RTM and DAM. Market coupling enhanced trade between exchanges, reduced consumer costs and increased surplus by matching lower-cost sellers with higher-value buyers, especially during peak periods.

Earlier, in August 2023, the CERC released a staff paper on market coupling, which discusses regulatory provisions for market coupling, the international experience, objectives of market coupling in India, issues and challenges in the implementation of market coupling and key points for discussion. The enabling provisions for market coupling have already been provided by the Commission in the CERC (Power Market) Regulations 2021. To study the readiness of the market and gauge the prerequisites for a smooth transition towards market coupling, the CERC has discussed some of the key issues in the implementation of market coupling and invited stakeholders’ comments on designing the framework for the implementation of market coupling.

Other developments

Other developments

In May 2024, the CERC released a staff paper on “Regulatory Oversight on Bidding Behaviour in Power Exchanges” to address issues such as abnormal increases in power prices. The paper discusses price discovery mechanisms, uniform market clearing prices, pay-as-bid and bid screening to enhance market predictability. As per the staff paper, all sellers must disclose their variable costs and technical parameters monthly, with this information remaining confidential. Each seller’s variable cost will be the benchmark supply offer (BSO) for their supply offer, and the designated agency will communicate the BSO for each category of suppliers to the power exchanges monthly. Power exchanges must ensure that a seller’s bid price offer for a time block does not exceed 1.6 times the respective BSOs and the average bid price offer submitted by a seller throughout the day (96 time blocks) does not exceed 1.2 times the

respective BSOs.

On February 21, 2024, the CERC issued a suo moto order to power exchanges aimed at enhancing market probity and transparency. This order mandates that no manual entry of bids by exchanges on behalf of their members is allowed during or after trading hours and no bids will be accepted after trading hours. Within one month, exchanges must implement a robust system with end-to-end data encryption from members’ trading workstations to the exchange platform. The order validation process must be fully automated without manual intervention. Additionally, bid cancellation and modification are not permitted after trading hours and there will be no extension of trading hours.

Conclusion

While power trading has grown significantly, the segment faces several challenges. One of the key challenges pertains to price volatility, which is primarily caused by supply-demand imbalances and fluctuations in fuel availability. Apart from this, transmission constraints also affect market performance, especially during peak demand periods. As the integration of renewable energy sources increases, the need for grid expansion and modernisation becomes critical.

As power markets in India evolve, electricity is increasingly being treated as a tradable commodity. Power exchanges and short-term contracts are anticipated to account for a significant share in trading volumes. Additionally, cross-border electricity trade is expected to rise in the coming years. The increasing integration of distributed energy resources is another growth driver for the segment. By aggregating these resources through virtual power plants, new trading opportunities will emerge, allowing smaller producers to boost market liquidity and enhance grid flexibility.

Aastha Sharma