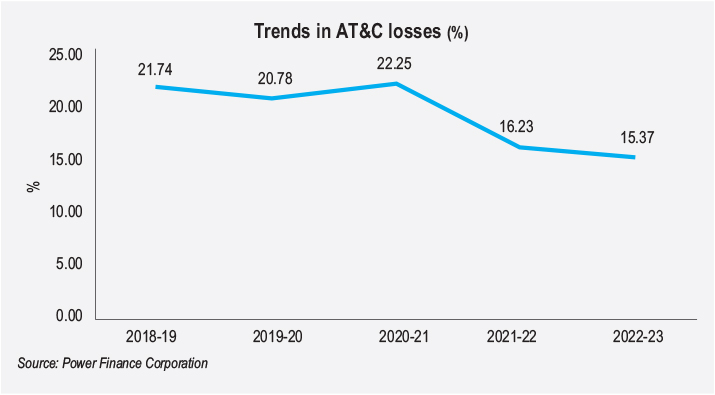

A resilient power distribution network is crucial for meeting India’s growing electricity demand and addressing evolving consumer needs. As electricity consumption rises, the distribution system needs to be capable of ensuring reliable and uninterrupted supply. Upgrading and modernising the distribution infrastructure are essential to accommodate the rising demand, improve efficiency and reduce losses in the system. Power distribution utilities are poised for major transformations in the coming years. Emerging customer demand and shifts in the energy landscape will accelerate the adoption of new business models for future utilities. Discoms are gearing up for increased load growth, the integration of more green energy into the grid, the expansion of rooftop solar and electric vehicles, network upgrades, enhanced consumer engagement and heightened competition in electricity supply. However, they continue to face significant operational and financial challenges, which affect their ability to maintain grid stability and ensure consumer satisfaction. The Power Finance Corporation’s (PFC) report highlights some positive developments, particularly a reduction in aggregate technical and commercial (AT&C) losses, which fell from 16.23 per cent in 2021-22 to 15.37 per cent in 2022-23. Despite this progress, AT&C losses remain a concern, reflecting ongoing inefficiencies and the commercial struggles of discoms. High losses affect their profitability and lead to higher electricity tariffs for consumers.

To address these issues, the government launched the Revamped Distribution Sector Scheme (RDSS) with a Rs 3 trillion budget to provide performance-based financial support. The scheme aims to improve discom efficiency, reduce losses and ensure their long-term sustainability by addressing the key challenges of poor infrastructure, revenue losses and operational issues. In addition, policy and regulatory reforms such as the Electricity (Rights of Consumers) Rules, 2020, empower consumers by ensuring reliable electricity supply and holding discoms accountable for service standards.

Size and growth

The distribution network has been growing steadily in terms of line length and transformer capacity. As per the Central Electricity Authority (CEA), the total number of power substations (66/11 kV, 33/11 kV and 22/11 kV) in the country was 39,965, with a total installed capacity of 482,810 MVA, on March 31, 2022. The total number of feeders (66 kV/33 kV/22 kV) stood at 36,804 in March 2022 and the length of the feeder infrastructure was 589,304 ckt km. The country had 230,979 feeders at the 11 kV level with a combined length of 4,935,279 ckt km. It had 1.47 million distribution transformers (DTs), with a combined capacity of 6.89 million MVA. The low tension power grid comprised 2,231,495 km of single-phase lines and 5,714,263 km of three-phase lines.

As per NITI Aayog, total energy sales were 1,117.9 BUs in 2022-23. Of this, domestic category consumers accounted for the maximum share of around 32 per cent at 355.8 BUs (over 331.6 BUs in 2021-22), followed by industrial consumers at 30.4 per cent or 340.2 BUs (compared to 330.26 BUs in 2021-22).

In 2023-24, the energy supply exhibited a clear uptrend, growing strongly. The energy requirement was 1,626 BUs, 8 per cent higher year on year than the previous year. Peak demand also grew strongly at more than 12 per cent year on year, with all-India peak demand (243 GW) being higher than peak supply (240 GW) in 2023-24. From April 2023 to March 2024, around 4 BUs of energy was not supplied as per the requirement. During the same period,

around 3 GW of all-India peak demand was not met.

Operational and financial performance

As per PFC’s Report on the Performance of Power Utilities, the aggregate losses of distribution utilities increased from Rs 269.47 billion in 2021-22 to Rs 572.23 billion in 2022-23. Receivables from power sales improved from 138 days of sale as of March 31, 2022, to 119 days as of March 31, 2023. Further, payables for the purchase of power improved from 168 days of sale as of March 31, 2022, to 128 days as of March 31, 2023.

The total outstanding debt of distribution utilities increased from Rs 6,148.53 billion as of March 31, 2022, to Rs 6,843.79 billion as of March 31, 2023. With regard to outstanding discom dues, as per the PRAAPTI portal (accessed on June 12, 2024) the total dues of discoms to gencos comprised remaining legacy dues of Rs 289.7 billion and current dues of Rs 632.65 billion.

On the operational performance front, AT&C losses fell to 15.37 per cent in 2022-23 (on a provisional basis) from 16.23 per cent in 2021-22. This was driven by an improvement in collection efficiency, from 92.77 per cent in 2020-21 to 97.27 per cent in 2022-23. Meanwhile, billing efficiency improved from 86.13 per cent in 2021-22 to 87 per cent in 2022-23.

As per the 12th Annual Integrated Rating and Ranking of Power Distribution Utilities report, financial deficit in the power distribution sector widened to Rs 790 billion in FY 2023, primarily driven by an 8 per cent increase in the gross input energy and a substantial rise in power purchase costs during the year. The absolute cash gap also increased from Rs 440 billion in FY 2022 to over Rs 790 billion in FY 2023, driven by the increasing average cost of supply-average realisable revenue (ACS-ARR) gap. The total sectoral debt increased by 11 per cent, from Rs 6.17 trillion in FY 2022 to Rs 6.87 trillion in FY 2023. The average power purchase costs during FY 2023 rose by 71 paise per kWh from FY 2022, as compared to the marginal increase of 4 paise per kWh in FY 2022 over FY 2021.

Key developments

Key developments

Electricity (Late Payment Surcharge and Related Matters) (Amendment) Rules, 2024: In February 2024, the Ministry of Power (MoP) notified the Electricity (Late Payment Surcharge and Related Matters) (Amendment) Rules, 2024. The amendments allow long-term power generators to sell power in the short-term market, allowing power generators to explore additional avenues for selling their generated power beyond their long-term contracts. Power generators who do not offer their surplus power will now not be eligible to claim capacity or fixed charges corresponding to that surplus quantum. Additionally, the surplus power cannot be offered for sale in the power exchange at a price of more than 120 per cent of the energy charge plus the applicable transmission charge.

Electricity (Second Amendment) Rules, 2024: In January 2024, the MoP incorporated provisions for subsidy accounting and payment, as well as the framework for financial sustainability. As per these amendments, discoms are now required to provide quarterly reports with detailed information about subsidy payments. The amendment also introduces procedures for allowing the transfer of expenses incurred by distribution licensees for the creation and upkeep of distribution assets.

Amendment to Electricity (Rights of Consumers) Rules, 2024: In February 2024, the MoP notified the Electricity (Rights of Consumers) Amendment Rules, 2024, reducing the timeline for getting new electricity connections and simplifying the process of setting up rooftop solar installations. Exemption has been given for the requirement of technical feasibility studies for systems with capacities of up to 10 kW. For systems with capacities higher than 10 kW, the timeline for completing feasibility studies has been reduced from 20 days to 15 days.

Smart metering update

As of June 2024, 11.6 million smart consumer meters have been installed in the country. Notably, during 2023-24, 4.84 million smart consumer meters were installed, nearly doubling the installations from the previous year.

Overall, around 222 million smart consumer meters, 5.26 million DT meters and 0.18 million feeder meters have been sanctioned across the onboarded states. As of September 4, 2024, over 117 million consumer smart meters have been awarded, which is 53 per cent of the total sanctioned meters, and 13.2 million consumer smart meters have been installed as per the NSGM dashboard. Further, over 4 million (78 per cent) of the sanctioned DT meters and 130,295 (71 per cent) of the sanctioned feeder smart meters have been awarded.

With the government mandating the transition to a complete smart metering system, replacing all the existing 250 million meters by 2025, the pace of smart meter awards and installations is expected to accelerate in the coming months. Bihar leads with the highest installation of smart meters, totalling 3,235,830, followed by Assam with 2,147,283. Uttar Pradesh closely trails with 1,186,953 meters installed, while Madhya Pradesh and Haryana have installed 971,151 and 847,467 meters respectively.

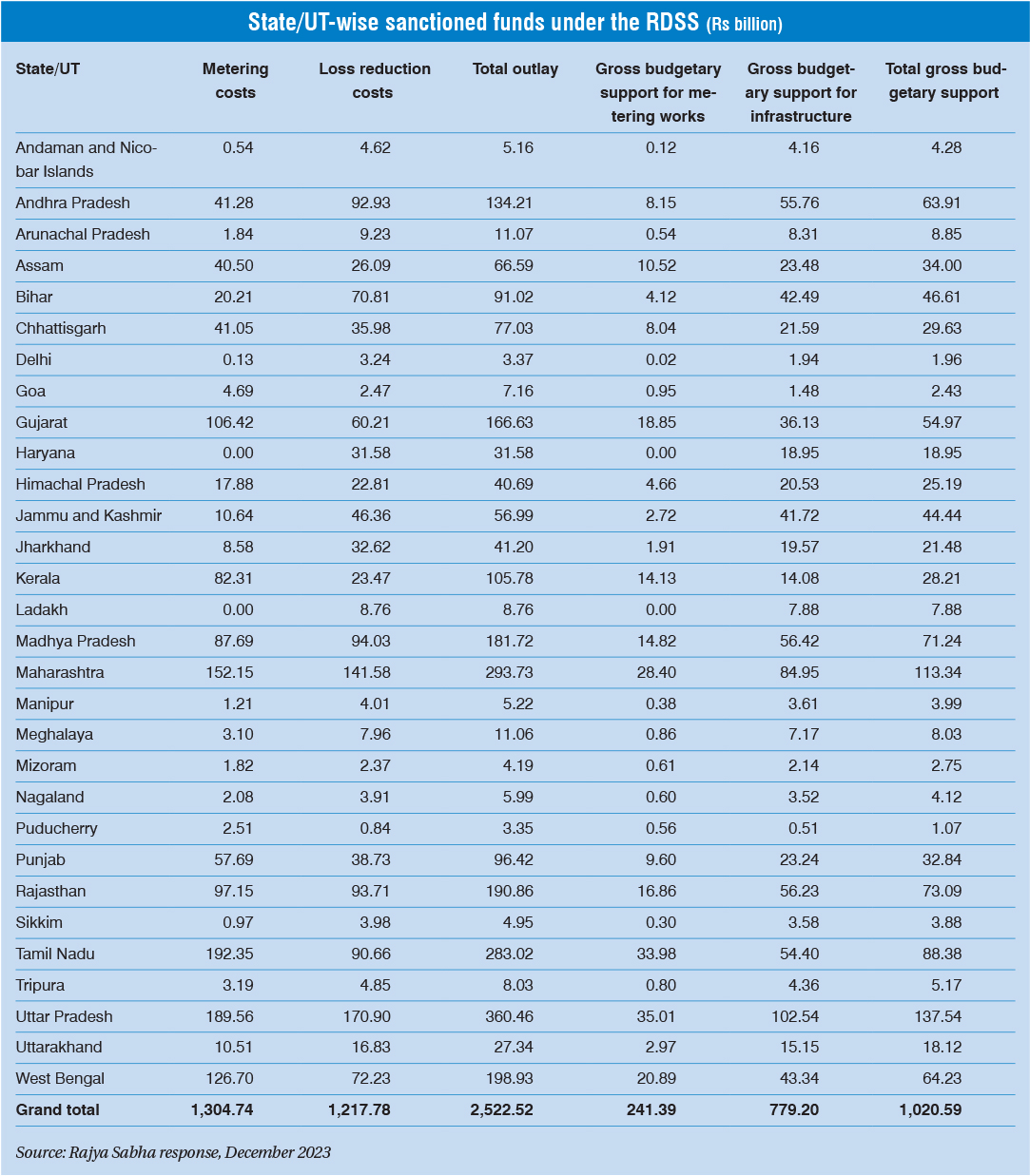

Update on the RDSS

Update on the RDSS

The reforms-based and results-linked RDSS has an outlay of Rs 3,037.58 billion over five years (2021-22 to 2025-26), with an estimated government budgetary support of Rs 976.31 billion. The scheme aims to reduce AT&C losses on a pan-Indian level to 12-15 per cent by 2024-25; reduce the ACS-ARR gap on a pan-Indian level to zero by 2024-25; and improve the quality, reliability and affordability of power supply to end-consumers. The RDSS focuses on providing financial support for smart metering systems, distribution infrastructure upgrades, training, capacity building and other enabling activities. Within the framework of the RDSS, there is a provision to extend financial support to eligible discoms for the deployment of prepaid smart meters for 250 million consumers, as well as system metering with communication features, by March 2025.

According to the Rajya Sabha Report (December 2023), around Rs 1,217 billion has been sanctioned (aggregate value of detailed project reports approved) for loss reduction works and Rs 1,304 billion for smart metering works. The overall physical progress of loss reduction works under the RDSS is currently at 14.77 per cent (as per the RDSS dashboard accessed on September 17, 2024). So far, under the scheme, about 197 million prepaid smart meters, 5.2 million DT meters and 188,000 feeder meters have been sanctioned across 30 states/union territories, with a total sanctioned cost (including project management agency costs) of about

Rs 1.3 trillion.

Network projections and investment requirements

The CEA, in collaboration with distribution utilities, has formulated the Distribution Perspective Plan up to fiscal year 2029-30. According to the 20th Electric Power Survey, the peak electricity demand of the country is projected to rise to 334,811 MW by 2029-30, demonstrating a CAGR of 6.45 per cent from 2021-22 to 2029-30.

The total power substation capacity (66/11 kV, 33/11 kV and 22/11 kV) in the country is expected to increase to 624,332 MVA by 2029-30. During 2022-23 to 2029-30, it is envisaged that another 12,192 substations will be added with a total capacity of 141,522 MVA.

The plan aims to add 92,920 new 11 kV feeders with a total length of 968,503 ckt km between 2022-23 and 2029-30. This will bring the total number of 11 kV feeders to around 323,899 and increase the overall network length to approximately 5,903,782 ckt km.

An addition of 46.5 million new DTs has been planned between 2022-23 and 2029-30. This represents a substantial increase in DT capacity, bringing the total to 9.28 million MVA by the end of the decade.

Based on the details received from utilities, about Rs 4.28 trillion will be required for the upgradation of distribution infrastructure during 2022-27, of which about Rs 1.89 trillion will be available to discoms, including funds sanctioned under the RDSS. The available funds will constitute around 44 per cent of the total investment required up to 2027. Approximately Rs 2.86 trillion will be required for the upgradation of distribution infrastructure during 2027-30, taking the total investment required to Rs 7.42 trillion during 2022-30.

Conclusion

The Indian power distribution sector continues to face several challenges, including unreliable supply, fiscal indiscipline and insufficient capital expenditure. Despite the implementation of reform programmes such as the Restructured Accelerated Power Development and Reform Programme, the Integrated Power Development Scheme, the Ujwal Discom Assurance Yojana, the financial restructuring plan and bailout packages amounting to millions, discom debt reached Rs 6.87 trillion in 2022-23. However, recent government interventions, such as the late payment surcharge regulations, timely subsidy disbursement and the RDSS, have created a positive momentum. AT&C losses were reduced due to improvements in both billing and collection efficiency. The ACS-ARR gap also narrowed, aided by more timely tariff orders issued by state regulators.

The primary challenge is to make discoms financially viable while empowering consumers. Annual integrated ratings and consumer service ratings play a crucial role in helping discoms assess performance and take accountability for improvements. The Electricity Amendment Bill, 2022, aims to empower consumers by introducing competition, allowing them to choose from multiple service providers and fostering privatisation within the sector. The bill also supports discoms in enhancing decision-making efficiency and achieving financial independence. However, state governments and regulatory commissions have been slow to adopt the provisions for competition, such as allowing parallel licensing.

Although progress has been made, several critical challenges persist. High AT&C losses and rising power costs, largely due to fuel and procurement expenses, continue to strain discom finances. Reducing the gap between the cost of supply and revenue, along with minimising reliance on borrowing for operational needs, is key to achieving financial stability for discoms.

Looking ahead, the sector is poised for significant improvements through initiatives such as smart metering, digital solutions and advanced distribution management systems, all of which can enhance efficiency and support renewable energy integration. Strengthening corporate governance through the appointment of independent directors, and improving financial and human resource management practices will also be vital for long-term success. With ongoing reforms, technological advancements and a focus on clean energy, the outlook for the power distribution sector is promising. Swift implementation of reforms such as the RDSS and the adoption of technologies such as smart grids, advanced metering infrastructure, energy storage systems and artificial intelligence will be essential in shaping a sustainable and competitive future for the sector.

Akanksha Chandrakar