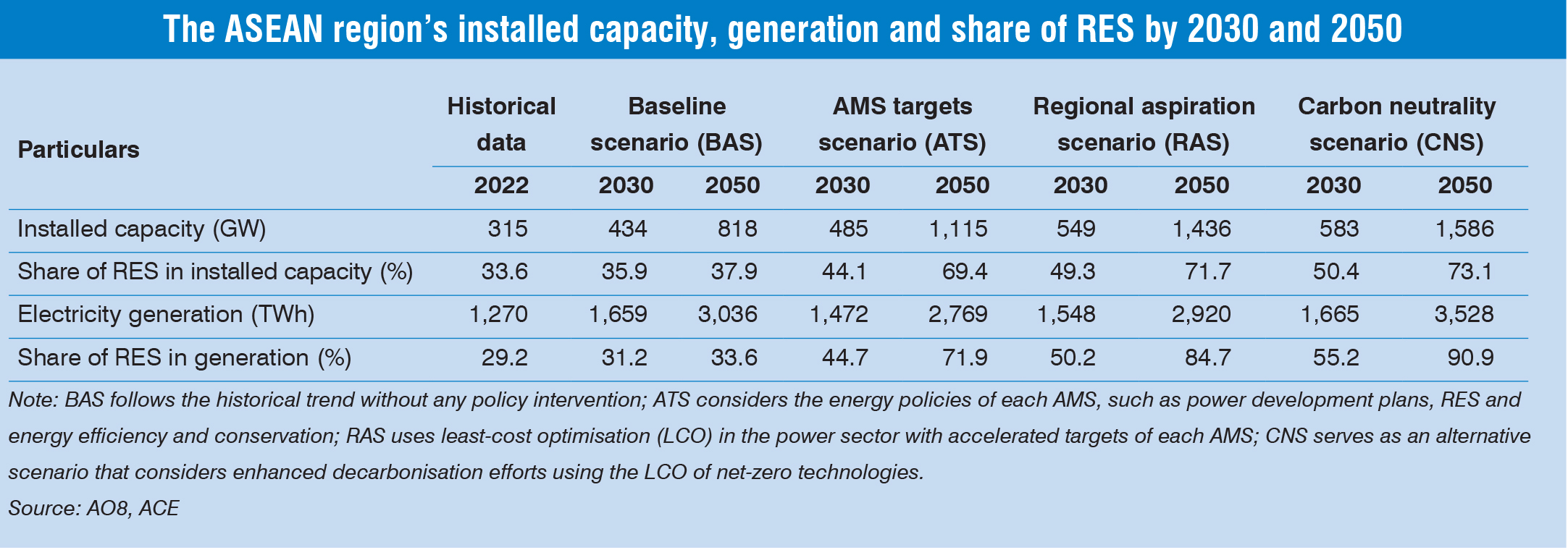

The economy of the Association of Southeast Asian Nations (ASEAN) region experienced a rebound in 2021, achieving a 4.1 per cent economic growth in 2023, and is projected to increase up to 4.7 per cent by 2025. This positions ASEAN, which comprises 10 members–Brunei Darussalam, Cambodia, Indonesia, Lao People’s Democratic Republic (PDR), Malaysia, Myanmar, the Philippines, Singapore, Thailand and Vietnam, home to 680 million people–among the world’s fastest growing economies. With rapid industrialisation and urbanisation, ASEAN’s energy demand is expected to continue increasing. While the region depends on fossil fuels to meet the growing demand, it is focusing on a sustainable transition to low-carbon energy sources along with energy security and economic growth. Renewable energy sources (RES) account for over one-third of the region’s installed capacity, which is set to increase to over 39 per cent by 2025, surpassing the 35 per cent target for the year.

In the long run, ASEAN is expected to witness a significant transformation in its energy mix, with a heavy dependence on RES for power generation. By 2050, RES such as solar, wind and hydro will contribute 1,742 TWh, or 63 per cent of the energy mix, exceeding the domination of fossil fuels in 2005 (85.8 per cent of 510 TWh) and 2022 (71.2 per cent of 1,267 TWh). This is driven by the region’s climate and energy goals. All ASEAN countries, except Indonesia and the Philippines, aim to reach net zero or carbon neutrality by 2050. While Indonesia aims to reach net zero by 2060, the Philippines does not have a specific target.

The ASEAN member states (AMS), through the ASEAN Economic Community (AEC), recognise the crucial role of regional cooperation in ensuring energy security, accessibility, affordability and sustainability at both the national and regional levels. The ASEAN Strategy for Carbon Neutrality, a strategic document endorsed during the 41st ASEAN Ministers on Energy Meeting (AMEM), 2023, emphasises the importance of integrating green infrastructure and markets within the energy sector, ensuring that regional efforts are effectively aligned with carbon neutrality goals. Further, to facilitate energy transition, ASEAN has established the ASEAN Plan of Action for Energy Cooperation (APAEC), which is renewed every 10 years. The current cycle spans from 2016 to 2025, with the next phase covering 2026 to 2035. The APAEC promotes multilateral energy cooperation and integration, aligning with the broader objectives of the AEC and its five-year strategic plans. The 8th ASEAN Energy Outlook (AEO8) recently released by the ASEAN Centre for Energy (ACE) – an intergovernmental organisation within the ASEAN structure – would form the foundation for developing APAEC 2026-30. The next phase of APAEC presents a unique opportunity for AMS to set even more ambitious climate and energy targets and achieve the ASEAN community’s long-term objectives of energy security and interconnectivity. A key component of this energy integration is the creation of an inter linked grid network–ASEAN Power Grid (APG)–amongst the ASEAN member countries.

Particularly, the 42nd AMEM, which concluded in September 2024, endorsed the theme for APAEC 2026-30 as “Advancing Regional Cooperation in Ensuring Energy Security and Accelerating Decarbonisation for a Just and Inclusive Energy Transition”. In the meeting, the AMS agreed that the APG is central to achieving a more resilient and sustainable energy future for ASEAN and facilitating cross-border electricity trade. To realise the APG, it tasked the Senior Officials’ Meeting on Energy (SOME) (AMEM’s operating arm that acts as a consultative committee for AMS’s cooperation activities) and ACE with expediting the finalisation of the APG enhanced MoU and its terms of reference (ToR) (before the expiry of the current MoU in 2025). Additionally, they are tasked with developing a framework for the ToR for subsea cable developments by the end of 2024 and establishing a timeline for concrete actions leading up to 2045. The success of the Lao PDR-Thailand-Malaysia-Singapore Power Integration Project (LTMS-PIP) (which commenced operations in June 2022) has been acknowledged as a model for multilateral power trade (MPT), further validating the feasibility of such initiatives. The LTMS-PIP recently entered into Phase II with doubling of electricity trade to 200 MW after an agreement between Singapore and Malaysia to import 100 MW. A similar initiative, the Brunei Darussalam-Indonesia-Malaysia-Philippines Power Integration Project (BIMP-PIP), is undergoing feasibility studies and

continued discussion.

The AMS is placing strong emphasis on establishing the necessary regulatory, policy, commercial and technical frameworks to enhance cross-border electricity trading and the urgency of upgrading interconnectors and deploying technologies, such as subsea links, to support the APG vision. Ministerial-level working groups have been established among various countries, including Lao PDR-Cambodia-Singapore; Vietnam-Singapore-US; and Singapore-US to facilitate cross-border electricity trading projects.

The AMS is placing strong emphasis on establishing the necessary regulatory, policy, commercial and technical frameworks to enhance cross-border electricity trading and the urgency of upgrading interconnectors and deploying technologies, such as subsea links, to support the APG vision. Ministerial-level working groups have been established among various countries, including Lao PDR-Cambodia-Singapore; Vietnam-Singapore-US; and Singapore-US to facilitate cross-border electricity trading projects.

During 2024, efforts were made to advance the APG interconnection and MPT, improve coordination among stakeholders, and improve sustainable and reliable electricity supply across the AMS. This includes the commencement of ASEAN Interconnection Masterplan Study (AIMS) III to further develop minimum requirements for the MPT; the completion of the ongoing technical and commercial feasibility studies for the Indonesia-Malaysia interconnections – Peninsular Malaysia to Sumatra and North Kalimantan to Sabah as well as the facilitation of new studies for other identified interconnections under AIMS III; capacity building in project finance; progress in harmonising technical standards; establishment of dispute settl ement mechanisms; road map for the MPT in ASEAN; and development of regulatory frameworks. These developments shaping the substantive progress of the APG are taking place under close coordination among the Heads of ASEAN Power Utilities and Authorities (the primary coordinator of the APG, which reports to SOME), the APG Consultative Committee, and ASEAN Energy Regulatory Network, facilitated by ACE and the ASEAN Secretariat.

Another aspect that is key to advancing regional interconnection projects is substantial investments. The Asian Development Bank and the World Bank are supporting the energy transition in the region, along with a dedicated facility for the APG. It is important to ensure close coordination between multilateral development banks and ASEAN countries to establish financing facilities for the planned energy projects. By 2030, the region will need to invest $200 billion in upgrading both domestic and regional infrastructure to fast-track interconnections and the energy transition.

Another aspect that is key to advancing regional interconnection projects is substantial investments. The Asian Development Bank and the World Bank are supporting the energy transition in the region, along with a dedicated facility for the APG. It is important to ensure close coordination between multilateral development banks and ASEAN countries to establish financing facilities for the planned energy projects. By 2030, the region will need to invest $200 billion in upgrading both domestic and regional infrastructure to fast-track interconnections and the energy transition.

APG – Recent developments

First mooted in 1999, the APG envisions the integration of electricity markets, the harmonisation of regulations, and the establishment of regional institutions in addition to the construction of cross-border interconnections. The APG is divided into three geographic areas–the North System (Cambodia, Lao PDR, Myanmar, Thailand and Vietnam); the South System (Indonesia, Malaysia and Singapore); and the East System (Brunei Darussalam, Indonesia, Malaysia and the Philippines). The APG is expected to progress in three stages: starting with bilateral trade, followed by subregional trade, and finally by an integrated regional system.

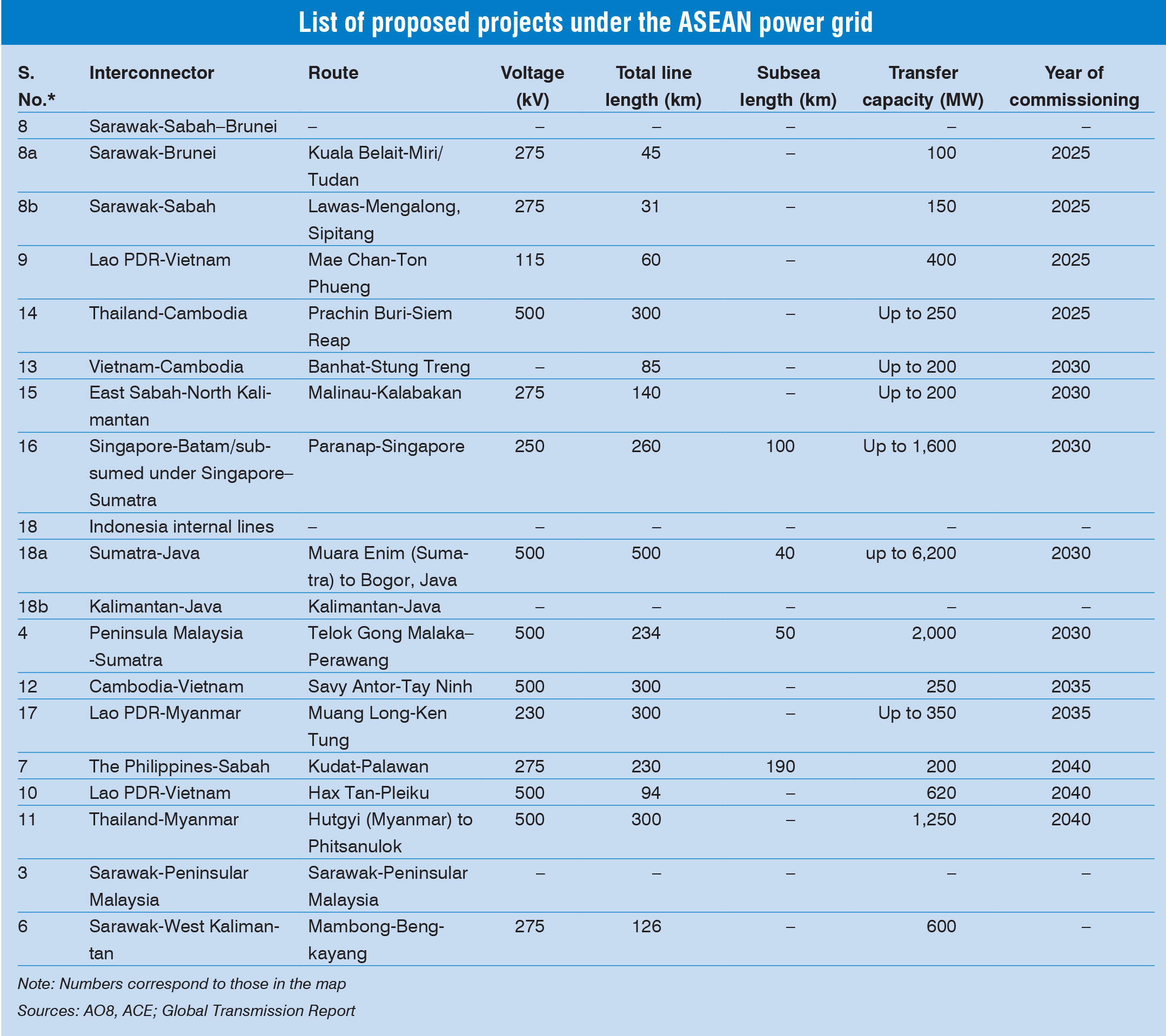

As of October 2024, nine out of the 18 key interconnection projects envisioned under the APG have been completed, resulting in a total installed regional electricity capacity of 7.7 GW, which includes 4.7 GW of dedicated independent power producer (IPP) generation exports (generation to grid). Most of these interconnections are bilateral, with energy trade conducted through long-term power purchase agreements. Ongoing projects currently at various stages of implementation include subsea cables between the Indonesian island of Sumatra and Peninsular Malaysia, overland grids between Kalimantan and Sabah, and upgrades to the interconnections between Thailand and Malaysia.

The completion of the APG will have significant benefits for energy security, decarbonisation costs and emission reductions. AIMS III Phases I and II demonstrate that cross-border interconnections will facilitate the utilisation of 62 RES projects – 42 solar projects with a capacity of 8,119 GW and 20 wind projects with a capacity of 342 GW. Regional interconnections are expected to optimise energy systems, thus reducing the need for 1.2 TWh of electrical storage, 16 TWh of hydrogen storage and 600 GW of solar capacity by 2050. By then, the APG could reduce the economic cost of decarbonisation in the region by $800 billion and the carbon footprint of the energy transition by 13 per cent.

Early results of energy integration are evident from the region’s first multilateral power project, LTMS-PIP, which facilitates the import of up to 100 MW of hydropower from Lao PDR to Singapore via Thailand and Malaysia, using existing interconnections. The project facilitated the trade of a total of 266 GWh of electricity as of February 2024. After the expiration of the initial agreement in June 2024, Singapore’s Keppel Limited and state-owned Electricite du Laos signed a renewal agreement on June 24, 2024. However, the Singapore government is yet to finalise the transmission agreement with Thailand and Malaysia due to disputes over power purchase quantities. The deadline for signing the transmission agreements among the three countries is December 31, 2024. Meanwhile, in September 2024, Phase II of the project took off with Tenaga Nasional Bhd, Malaysia’s state-owned power utility, entering into a cross-border agreement with Keppel’s renewable arm, to supply up to 100 MW of electricity. This followed the Singaporean Energy Market Authority’s decision to extend Keppel’s licence to import electricity for another two years until 2026.

The second multilateral project, BIMP-PIP, announced at the 41st AMEM in August 2023, envisions 17 interconnections among the four countries, and is expected to reduce the price of electricity as well as the use of fossil fuels. The United States Agency for International Development is currently supporting a $2 million feasibility study on the BIMP-PIP. While the LTMS-PIP facilitates unidirectional energy trade using existing overland grids, the BIMP-PIP will facilitate a higher level of energy integration through new overland and subsea cables that will enable bidirectional trade.

The second multilateral project, BIMP-PIP, announced at the 41st AMEM in August 2023, envisions 17 interconnections among the four countries, and is expected to reduce the price of electricity as well as the use of fossil fuels. The United States Agency for International Development is currently supporting a $2 million feasibility study on the BIMP-PIP. While the LTMS-PIP facilitates unidirectional energy trade using existing overland grids, the BIMP-PIP will facilitate a higher level of energy integration through new overland and subsea cables that will enable bidirectional trade.

In addition to the BIMP-PIP, several bilateral interconnections that were not part of the original APG plan are now at various stages of discussion, including subsea cables between Singapore and Vietnam, Singapore and Cambodia, and overland interconnection between Lao PDR and Vietnam.

The way forward

The implementation of the proposed interconnections requires the development of institutional, market and technical capacities, which are expected to be reflected in the upcoming APG agreement. The ASEAN Framework Agreement for Power Trade, which is a key component of the APG MoU, is expected to facilitate the development of protocols on regional institutions, market development and infrastructure planning.

The establishment of a regional institution is vital for boosting multilateral power trade in the ASEAN region. While the LTMS-PIP working groups and task forces provide valuable lessons in viable models for regional cooperation on specific projects, experiences with grid management in 36 European countries (through the European Network of Transmission System Operators) and 12 Southern African countries (through the Southern African Power Pool) highlight the need for a regional institution. The AEO8 states that developing a regional institution based on binding mandates is necessary for driving this integration despite the difficulties posed by political challenges. It recommends that the APG MoU should develop procedures to facilitate discussion between policymakers on developing binding legislation for setting up such a regional energy institution with adequate resources and proper frameworks.

In terms of market development, there is a need for reforming domestic power markets, given that in most ASEAN countries (except Singapore and the Philippines, which have liberalised their electricity markets), state-owned integrated power utilities continue to monopolise the sector. For the creation of a regional energy market, the risks and challenges need to be mitigated through the development of standardised wheeling charges and dispute resolution mechanisms, as well as maximising opportunities in green finance, such as renewable energy certificate markets.

The key requirements for infrastructure planning and operations in the ASEAN region include the sharing of accurate and reliable data on energy supply, demand, consumption and system performance; the harmonisation of grid codes; and the identification of priority “backbone” projects. While the LTMS-PIP has developed a platform to share data on sales, purchases, electricity wheeling and system constraints, the APG will require a much higher level of data sharing and standardisation. For this, ACE has proposed the development of a “data-sharing framework and governance guidelines” to facilitate discussion on identifying the type, use and timeliness of data exchange in the ASEAN region. Further, the grid codes need to be updated to accommodate greater RES integration and use of distributed generation. Given the funding constraints, an ASEAN Projects of Common Interests (PCI) categorisation of regional interconnections, similar to the European Union’s PCI initiative, could facilitate the pooling of financial resources for priority backbone projects of the APG.

Fast-tracking the progress of the APG needs high levels of political commitment, technical harmonisation and data sharing, as well as massive infrastructure investments. The upcoming APG MoU provides an opportunity for policymakers to create consensus on the development of regional institutions, markets and infrastructure planning. A collaborative approach remains key for an integrated, energy-secure and sustainable ASEAN power market.