With India intensifying its focus on renewable energy, hydropower is gaining traction as a vital energy source due to its ability to provide reliable and flexible power. The sector is set for significant expansion on the back of recent policy initiatives and ongoing project developments. To further advance hydropower, several measures have been implemented, such as the waiver of interstate transmission system (ISTS) charges for hydroelectric plants (HEPs) and guidelines for pumped storage plants (PSPs).

Segment size and growth

As of October 2024, the country’s installed hydropower capacity stood at 46,928.17 MW for large hydro and 5,077.25 MW for small hydro. During 2024-25 (till October), hydropower capacity of 40 MW was added with the commissioning of the Thottiyar HEP by the Kerala State Electricity Board. In 2023-24, the net hydropower capacity addition was 78 MW.

The northern region has the highest hydropower installed capacity, totalling 20,829.76 MW. According to the Central Electricity Authority’s (CEA) Reassessment Study (2017-23), the country’s exploitable hydropower potential is approximately 133 GW, with an additional pumped storage potential of 120 GW. However, only about 31 per cent of hydropower and 4 per cent of pumped storage capacities have been utilised so far.

Large hydro generation during April to October 2024 reached 109,037.19 MUs, reflecting a 6.93 per cent increase compared to the same period in the previous year. Similarly, small hydro generation rose by 20.43 per cent to 8,098.18 MUs. During the 2019-20 to 2023-24 period, the share of hydropower in the total renewable energy generation fell from 53 per cent to 37 per cent.

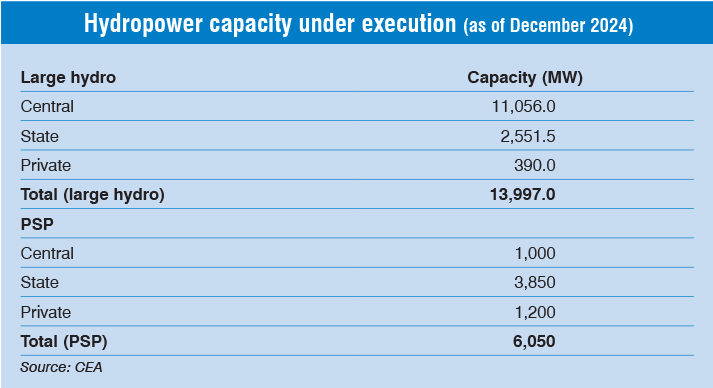

As of December 2024, there are 28 large hydropower projects (above 25 MW) of 13,997.5 MW capacity under construction. Around 1,730 MW of hydropower capacity is anticipated to be commissioned in 2024-25, including two units of pumped storage capacity (from Greenko’s Pinnapuram 4×240 MW and 2×120 MW projects in Andhra Pradesh).

Given their long-duration storage capabilities, PSPs are expected to play a pivotal role in sustainably integrating intermittent renewable sources while maintaining grid stability. This technology will be particularly important in meeting the rising demand for round-the-clock renewable energy by utilities and industrial consumers. As per CEA’s estimates for April 2024, India has the potential to deploy 118 PSPs with a total capacity of roughly 133,691 MW across different parts of the country. This includes both on-river and off-river projects.

Currently, eight PSPs with a combined capacity of 4,745.60 MW are operational, five (6,050 MW) are under construction, and four have been accorded concurrence by the CEA. Another 44 PSPs (60,050 MW) are at the survey and investigation stage.

New policy initiatives

New policy initiatives

The central government has renewed its focus on hydropower development by launching various reforms. These include granting renewable energy status to large hydroelectric projects, allowing new HEPs and PSPs to access concessions and green financing available to renewable energy. The waiver of ISTS charges on transmission of power from new HEPs as well as PSPs has been another key reform.

In September 2024, the Union Cabinet approved a proposal by the Ministry of Power for modification of the budgetary support scheme aimed at creating “enabling infrastructure for HEPs” with a total outlay of Rs 124.61 billion. The scheme will be implemented from 2024-25 to 2031-32. It is applicable to PSPs and HEPs above 25 MW, with a cumulative generation capacity of about 31,350 MW and a letter of award given before June 30, 2028. The scheme will be implemented from 2024-25 to 2031-32. PSPs with an aggregate 15,000 MW of capacity will be supported under

the scheme.

Budgetary support for the cost of enabling infrastructure has been capped at Rs 10 million per MW for projects up to 200 MW. For projects with a capacity above 200 MW, Rs 2 billion plus Rs 7.5 million per MW has been allotted as budgetary support. In exceptional cases, the limit of budgetary support may go up to Rs 15 million per MW.

Modifications have been made in the new scheme in order to widen the ambit of budgetary support to cover the cost of enabling infrastructure by including four more items apart from construction of roads and bridges, that is, the cost incurred for the construction of: (i) transmission line from the power house to the nearest pooling point including upgradation of the pooling substation belonging to the State/Central Transmission Utility, (ii) ropeways, (iii) railway sidings, and (iv) communication infrastructure. The strengthening of the existing roads/bridges leading to the project will also be eligible for central assistance under this scheme.

In August 2024, the Union Cabinet approved central financial assistance (CFA) for the state governments in north-eastern India towards equity participation for the development of hydroelectric projects in the region. These projects will be joint ventures between state governments and central public sector undertakings. Under the scheme, a cumulative hydropower capacity of about 15,000 MW will be developed. The scheme has been allocated a budget of Rs 41.36 billion for a period of seven years from 2024-25 to 2031-32. The funding will be distributed as a 10 per cent gross budgetary support for the north-eastern region from the total outlay of the Ministry of Power. The state governments of the region are allowed to contribute a maximum of 24 per cent of the project equity with an upper limit of Rs 7.5 billion per project. The CFA will be provided only to viable hydroelectric projects. As an incentive, the states will have to “waive, stagger free power or reimburse SGST to make the projects viable.”

To promote hydropower in the Northeast, the Ministry of Power, vide orders dated 22.12.2021 and 11.05.2023, has identified 58 HEPs with an installed capacity of 44.7 GW in Arunachal Pradesh for implementation by hydro central public sector undertakings (CPSUs). MoUs for 13 projects, totalling 12.7 GW in capacity, were signed between the Government of Arunachal Pradesh and CPSUs. A number of stalled hydropower projects have been revived in the past few years due to the persistent efforts and policies of state governments. These include the Teesta VI (500 MW) and Rangit IV (120 MW) projects in Sikkim, and the Lower Subansiri (2,000 MW) and Dibang (2,880 MW) projects in Arunachal Pradesh.

Meanwhile, in November 2024, the CEA officially recognised Surface Hydrokinetic Turbine (SHKT) technology under the hydro category, encouraging innovation and exploration of alternative technologies to help achieve net zero emission goals and support the sustainable development of the country’s power sector. Unlike traditional power generation methods that rely on the potential energy of water (using structures such as dams, diversion weirs and barrages to create the necessary “head”), SHKT generates electricity by harnessing the kinetic energy of flowing water, with almost no need for a potential head. This technology presents a viable solution for the power sector to meet the increasing demand for continuous, baseload renewable energy, especially in regions with limited grid access. SHKT turbines are easy to install and offer a cost-effective generation method, with electricity production costing Rs 2 per unit-Rs 3 per unit. It creates a mutually beneficial situation for both renewable energy buyers and producers.

Challenges and outlook

Despite this growth potential, the hydropower segment faces several challenges, including disputes over water rights, environmental concerns, a shortage of financially strong civil contractors, and difficulties related to resettlement and unforeseen geological conditions. These problems often result in delays and cost overruns, underscoring the need for comprehensive strategies to overcome these barriers and fully realise the country’s hydroelectric potential. As per the CEA, a capacity of 1,230 MW is currently stalled.

Hydropower, especially PSPs, are necessary to achieve the government’s commitment of 500 GW of installed capacity from non-fossil fuel sources by 2030 and net zero carbon emissions by 2070.