Boilers, turbines and generators (BTGs) are the key components of thermal power plants (TPPs), responsible for electricity generation. Recent capacity augmentation in TPPs to meet the growing power demand has increased the business potential of the BTG industry. The thermal power sector is witnessing a revival after three years, even as India’s power generation mix continues to transition. Factors such as increasing economic activity, robust GDP growth, industrial expansion and record high power demand are prompting many utilities to accelerate the brownfield expansion of their existing coal-based thermal power projects.

Industry overview

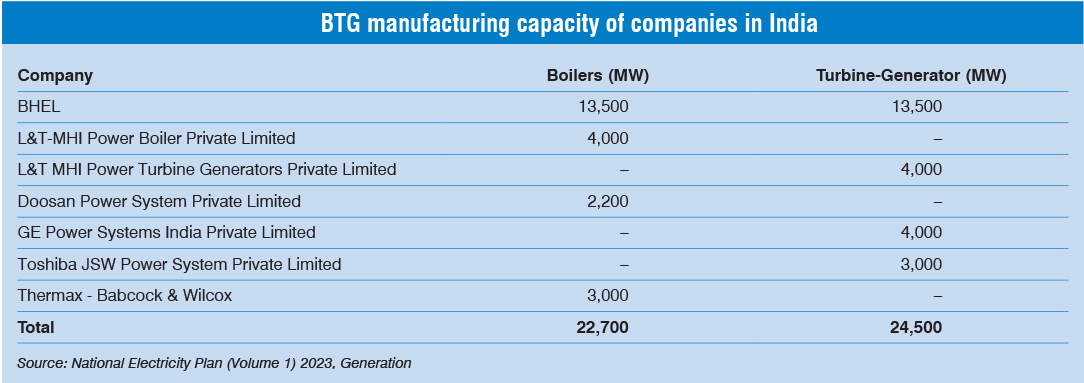

Over 65 per cent of India’s electricity generation capacity comes from TPPs, with the majority being coal-based, driving the demand for BTG manufacturing. The Indian industry is well equipped to produce a wide range of utility boilers and auxiliaries.

Bharat Heavy Electricals Limited (BHEL) is the country’s largest boiler manufacturer, capable of producing steam generators with capacities ranging from 30 MW to 800 MW, using coal, lignite, oil, natural gas, or a combination of these fuels. Indigenous manufacturers are also capable of producing turbines up to 800 MW for steam, 270 MW for hydro and 260 MW for gas turbines. Additionally, generators up to 800 MW for utility and combined cycle applications are manufactured domestically.

One of the key opportunities for BTG industry players lies in the government’s ambitious plans to augment the country’s thermal power generation capacity to approximately 280 GW by 2032. In line with this, the government has renewed its focus on adding 80 GW of thermal capacity by 2032 to ensure national energy security. After an extended pause, there are signs that the BTG tendering pipeline is gaining momentum. In 2023-24, around 9.6 GW of thermal power projects were ordered. According to the Central Electricity Authority’s (CEA) National Electricity Plan, an additional 51 GW of thermal power generation capacity is projected to be added over the next decade, averaging 5.1 GW per year.

Further, as the outdated subcritical units are retired, there will be a growing demand for new supercritical units, creating significant equipment supply opportunities for BTG providers. This shift is expected to further promote the BTG industry, which has built significant manufacturing capacity.

Trends and opportunities

Trends and opportunities

The global BTG market size was around $59.86 billion in 2022 and is predicted to grow to around $77.20 billion by 2030 at a CAGR of roughly 3.4 per cent between 2023 and 2030.

For the Indian market, the shift towards clean coal technologies like ultra-supercritical and advanced ultra-supercritical (AUSC) by new power plants is a key area of opportunity. Supercritical and ultra-supercritical units improve efficiency by 8 per cent, cut CO2 emissions and save 2 per cent fuel per unit of power, while AUSC aims for 45-46 per cent efficiency using indigenous materials like Alloy 617M.

As per the CEA’s broad status thermal report, 11 projects (20 units) aggregating 15,160 MW based on ultra-supercritical technology are under construction. Additionally, India’s first 800 MW AUSC TPP worth Rs 150 billion will be built in Korba, Chhattisgarh, by NTPC and BHEL. With a thermal efficiency of 46 per cent, it will outperform existing supercritical (41-42 per cent) and subcritical (38 per cent) units, promoting high-efficiency and low-emission power generation. The project is supported by government incentives and is a joint effort with the Indira Gandhi Centre for Atomic Research.

TPPs are also implementing flexibilisation solutions to balance fluctuating renewable energy. They are investing in advanced upgrades like condition monitoring systems, control and instrumentation enhancements, combustion optimisation and steam/flue gas management. Pithead plants with low fuel costs are better suited for sub-40 per cent load operations, while newer plants require significant investment in fast ramping equipment. Ageing plants are less capital-intensive for flexibilisation but incur higher operational costs. Flexibilisation retrofits must be evaluated on a case-by-case basis for commercial viability, presenting a key area of opportunity for equipment and technology providers. TPPs are also adapting for biomass co-firing and converting to biomass-fired plants, as mandated by the government.

TPPs are leveraging digital solutions such as artificial intelligence, digital twins and IIoT to optimise performance and ensure reliability. Industry players are offering technologies like remote monitoring and diagnostic services, remote vibration and diagnostic systems, and plant automation and live monitoring for real-time monitoring and advanced analytics.

Renovation and modernisation (R&M) and life extension (LE) of coal-based power plants present significant opportunities for equipment companies. During 2017-22, R&M/LE works were identified for 71 units (14,929 MW), with eight units (1,197 MW) already completed up to September 2024. The remaining projects are at various stages, including feasibility studies, detailed project reports, and tendering. Further, the CEA has identified 148 units with a total capacity of 38,150 MW as potential candidates for R&M/LE works during 2024-33), with units over 20 years old as of December 2022.

Thermal utilities in the country are also taking steps for the implementation of government norms to reduce suspended particulate matter, NOX and SOX emissions in the coming years. This has driven investments in flue gas desulphurisation (FGD) systems and electrostatic precipitators for pollution control. According to the Ministry of Power, FGD is being installed in 537 units (204.16 GW), with installation completed in 39 units (19.43 GW). Further, contracts/letters of award have been awarded for 238 units (105.2 GW) while 139 units (42.85 GW) are at various stages of tendering and 121 units (36.68 GW) are at the pre-tendering stage.

Further, growth in the nuclear power segment is expected to increase demand for nuclear steam turbines and generators. NITI Aayog and the Department of Atomic Energy are exploring the potential of repurposing retiring TPPs with small modular nuclear reactors.

Challenges and outlook

The BTG market faces several significant challenges that affect both operational efficiency and market growth. In the case of TPPs, while the BTG equipment market is mature, challenges remain regarding the full indigenisation of FGD and selective catalytic reduction systems. Also, stricter emissions regulations and environmental standards require manufacturers to continuously innovate to remain compliant, adding pressure to already high operational costs. The market is also impacted by supply chain disruptions, including raw material shortages, rising transportation costs and logistical issues, which can delay production timelines and hinder the overall efficiency of the industry. Ageing infrastructure and the need for frequent maintenance result in increased downtime and operational inefficiencies, further limiting productivity.

These challenges notwithstanding, trends such as the integration of digital technologies and internet of things are enhancing efficiency and reliability, and enabling predictive maintenance and real-time monitoring. Investments in decarbonisation technologies, such as carbon capture and storage, also create avenues for innovation. Furthermore, there is growing demand for customised and scalable solutions to address the diverse needs of the industrial, commercial and residential sectors.

Ongoing investment in research and development is critical for the industry to remain at the forefront of technological advancements. Partnerships between industry, academia and research institutions can drive innovation and provide solutions to the challenges faced by the BTG sector.

Aastha Sharma