Improving the financial and operational performance of distribution companies remains a persistent challenge in the power sector. As per the Power Finance Corporation’s (PFC’s) latest report on the performance of state power utilities for 2023-24, the average aggregate technical and commercial (AT&C) losses for distribution utilities at the national level increased from 15.11 per cent in 2022-23 to 16.12 per cent in 2023-24. Meanwhile, billing efficiency decreased marginally from 86.98 per cent in 2022-23 to 86.91 per cent in 2023-24, while collection efficiency declined from 97.6 per cent to 96.51 per cent.

The report gives a detailed overview of key financial and operational metrics for discoms. It is based on a comprehensive survey covering 63 power distribution utilities out of 72 for the year 2023-24, compared to 67 utilities covered in the 2022-23 report. It is compiled based on audited/provisional annual accounts of the utilities. Of the 59 state and private discoms covered, 52 submitted audited annual accounts.

Power Line presents the key highlights of the report…

Performance of distribution utilities

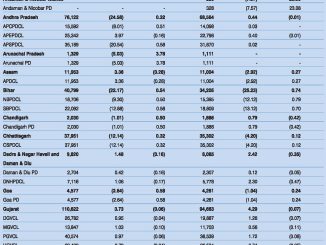

Overall, AT&C losses for distribution utilities increased from 15.11 per cent in 2022-23 to 16.12 per cent in 2023-24. Among the state sector utilities, Dakshin Gujarat Vij Company Limited (DGVCL) registered the lowest AT&C losses (1.31 per cent). Overall, 37 utilities reported AT&C losses lower than the all-India national average. The top five among them were DGVCL (1.31 per cent), India Power Corporation Limited (IPCL) (4.07 per cent), Tata Power Delhi Distribution Limited (TPDDL) (5.91 per cent), Adani Electricity Mumbai Limited (AEML) (6.12 per cent) and BSES Rajdhani Power Limited (BRPL) (6.58 per cent). On the other end of the spectrum, utilities with the highest AT&C losses included the Nagaland Power Department (PD) (47.11 per cent), Arunachal PD (44.56 per cent), Ladakh PD (42.46 per cent), Mizoram (34.85 per cent) and Jharkhand Bijli Vitran Nigam Limited (JBVNL) (31.17 per cent). During 2023-24, 19 states and union territories witnessed an improvement in AT&C losses over the previous year. These were Goa, Sikkim, Arunachal Pradesh, Uttar Pradesh, Puducherry, Bihar, Assam, Karnataka, Odisha, Gujarat, Haryana, Uttarakhand, Tripura, Manipur, Punjab, Chhattisgarh, Meghalaya, Nagaland and Delhi.

The billing efficiency decreased to 86.91 per cent in 2023-24 from 86.98 per cent in 2022-23. The top five utilities with the highest billing efficiency as per the report were DGVCL (98.69 per cent), IPCL (97.32 per cent), New Delhi Municipal Council (96.08 per cent), Brihanmumbai Electric Supply and Transport (95.88 per cent) and AEML (94.13 per cent).

The collection efficiency also declined from 97.6 per cent in 2022-23 to 96.51 per cent in 2023-24. However, several utilities recorded 100 per cent collection efficiency during 2023-24. These included DGVCL, Andaman & Nicobar PD, Uttar Haryana Bijli Vitran Nigam Limited, Chamundeshwari Electricity Supply Corporation Limited, Madhya Pradesh Paschim Kshetra Vidyut Vitran Company Limited, Meghalaya Power Distribution Corporation Limited, Sikkim PD, Tripura State Electricity Corporation Limited, Kanpur Electricity Supply Company Limited (KESCO), Purvanchal Vidyut Vitaran Nigam Limited, TPDDL, TP Northern Odisha Distribution Limited, TP Central Odisha Distribution Limited, BRPL and Gulbarga Electricity Supply Company Limited.

The aggregate losses (on a subsidy billed basis) for distribution utilities fell from Rs 594.97 billion in 2022-23 to Rs 255.53 billion in 2023-24, a 57.05 per cent reduction. Based on PFC’s data, the states with the highest loss levels were Karnataka with an aggregate loss of Rs 85.5 billion, followed by Uttar Pradesh at Rs 70.58 billion and Telangana at Rs 63.51 billion. In contrast, Gujarat posted a profit of Rs 43.39 billion, followed by Delhi at Rs 16.81 billion.

Aggregate losses on tariff subsidies received, excluding regulatory income and revenue grants under the Ujwal Discom Assurance Yojana (UDAY) for loan takeover, decreased from Rs 729.05 billion in 2022-23 to Rs 319.7 billion in 2023-24.

Aggregate losses on tariff subsidies received, excluding regulatory income and revenue grants under the Ujwal Discom Assurance Yojana (UDAY) for loan takeover, decreased from Rs 729.05 billion in 2022-23 to Rs 319.7 billion in 2023-24.

Distribution utilities sold 1,252,633 MUs of energy in 2023-24, a year-on-year increase of 6.56 per cent from 1,175,474 MUs in 2022-23. The highest energy sales were recorded in Maharashtra (139.47 BUs), Uttar Pradesh (113.48 BUs), Gujarat (109.21 BUs) and Tamil Nadu (92.74 BUs).

Revenue from operations, including billed tariff subsidies, increased by 13.57 per cent from Rs 8,458.41 billion in 2022-23 to Rs 9,605.95 billion in 2022-23. The top revenue-earning discoms for 2022-23 were Maharashtra State Electricity Distribution Company Limited (Rs 996.11 billion), Tamil Nadu Generation and Distribution Corporation (Rs 636.75 billion), Southern Power Distribution Company of Telangana Limited (Rs 321.02 billion), West Bengal State Electricity Distribution Company Limited (Rs 284.64 billion) and DGVCL (Rs 252.09 billion).

Tariff subsidies billed by distribution utilities increased from Rs 1,690.16 billion in 2022-23 to Rs 2,107.84 billion in 2023-24. As a percentage of the total revenue, tariff subsidies billed by utilities increased from 17.56 per cent in 2022-23 to 20.21 per cent in 2023-24. Subsidies released by state governments dropped to 97.4 per cent of billed subsidies in 2023-24 compared to 108.58 per cent in 2022-23.

During 2023-24, Rs 9.33 billion was booked by distribution utilities as income recoverable through future tariff as compared to Rs 279.12 billion booked during 2022-23. Total revenue (including tariff subsidy billed, regulatory income, revenue grants and other income) for distribution utilities increased from Rs 9,623.42 billion in 2022-23 to Rs 10,429.6 billion in 2023-24, whereas total expenditure increased from Rs 10,208.78 billion in 2022-23 to Rs 10,652.4 billion in 2023-24. Consequently, cost recovery improved from 94.27 per cent in 2022-23 to 97.91 per cent in 2023-24.

The gap in tariff subsidy billed narrowed from Re 0.41 per kWh in 2022-23 to Re 0.15 per kWh in 2023-24. The gap in tariff subsidy received, excluding regulatory income and revenue grant under UDAY for loan takeover, improved from Re 0.5 per kWh in 2022-23 to Re 0.19 per kWh in 2023-24.

The cash-adjusted gap also improved from Re 0.57 per kWh in 2022-23 to Re 0.39 per kWh in 2023-24. Receivables for the sale of power (number of days) remained constant at 115 days as of March 31, 2024.

Payables for the purchase of power (number of days) improved from 129 days as of March 31, 2023, to 132 days as of March 31, 2024. KESCO was the state utility with the lowest payables (0 days), followed by DGVCL (one day), Uttar Gujarat Vij Company Limited (two days) and Paschim Gujarat Vij Company Limited (three days).

The average cost of power (including own generation) for distribution utilities decreased from Rs 5.48 per kWh in 2022-23 to Rs 5.43 per kWh in 2023-24.

The net worth of distribution utilities remained negative at Rs 1,733.65 billion as of March 31, 2024. Total borrowings rose from Rs 6,848.36 billion to Rs 7,526.77 billion.

Conclusion

In conclusion, the PFC report highlights that state-owned distribution utilities continue to face financial and operational challenges. While energy sales and revenues have grown, aggregate losses have also increased sharply. Addressing these issues will require holistic strategies focused on debt management, revenue optimisation and improved efficiency across the power distribution segment.

Akanksha Chandrakar