India’s transmission system is undergoing rapid expansion, driven by large-scale interstate and intra-state transmission system build-outs, increased interregional capacity and green energy evacuation initiatives. In recent years, transmission expansion has witnessed the addition of multi-gigawatt corridors, high voltage direct current (HVDC) backbones and new pooling nodes, in sync with rising demand and renewable energy additions. These network expansions are critical to meet India’s climate targets and modernise its energy infrastructure.

Power Line presents the key trends and developments shaping the power transmission segment…

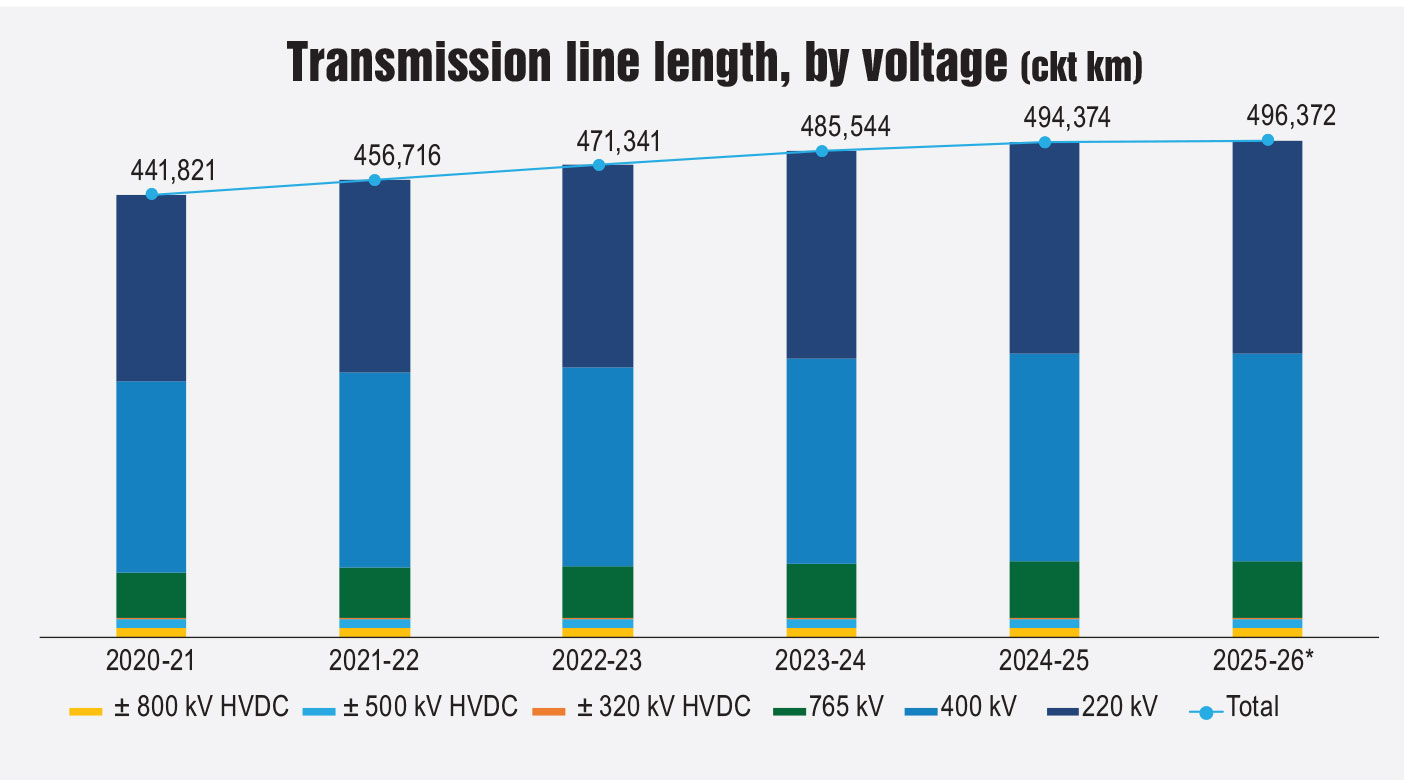

Segment size and growth

As of August 2025, the total transmission line length at the 220 kV and above levels stood at 496,372 ckt km, with 57,255 ckt km (11.53 per cent) at the 765 kV level, 207,049 ckt km (41.71 per cent) at 400 kV and 212,693 ckt km (42.84 per cent) at 230/220 kV. At the HVDC level, line length stood at 9,655 ckt km at the ±800 kV level, 9,432 ckt km at the ±500 kV level and 288 ckt km at the ±320 kV level. In 2025-26 (up to August 2025), the total transmission line addition was 1,998 ckt km. Between 2019-20 and 2024-25, transmission line length grew at a CAGR of 3 per cent.

With respect to interregional capacity in 2024-25, the segment added 2,200 MW in 2024-25, taking the total interregional capacity to 118,740 MW. As of August 2025, the country’s total interregional capacity further reached 120,340 MW. Between 2019-20 and 2024-25, the interregional capacity line grew at a CAGR of 3.7 per cent.

The transformation capacity across AC voltage levels stood at 1,341,918 MVA as of August 2025, with 336,700 MVA at the 765 kV level, 507,373 MVA at the 400 kV level and 497,845 MVA at the 230/220 kV level. The aggregate HVDC capacity stood at 33,500 MW, including 18,000 MW at the ±800 kV level, 13,500 MW at ±500 kV and 2,000 MVA at ±320 kV. Between 2019-20 and 2024-25, the AC transformation capacity grew at a CAGR of 6.7 per cent. Voltage-wise, the highest growth was recorded at the 765 kV and 400 kV levels, at 6.4 per cent and 8 per cent respectively. Meanwhile, the HVDC transformation capacity grew at a CAGR of 5.6 per cent, with the highest growth rate of 8.4 per cent recorded at the ±800 kV level.

The total transformation capacity addition during 2023-24 stood at 70,728 MVA, which rose to 86,433 MVA during 2024-25. In 2025-26 (as of August 2025), 37,905 MVA of total transformation capacity has been added.

The existing cross-border power transfer capacity stands at about 5,414 MW. This comprises India’s interconnections with Bhutan (2,651 MW), Bangladesh (1,160 MW), Nepal (1,600 MW) and Myanmar (3 MW). In 2024-25, India exported 0.86 BUs of electricity to Bhutan, 1.63 BUs to Nepal and 8.12 BUs to Bangladesh. Electricity imports stood at 5.33 BUs from Bhutan and 2.12 BUs from Nepal.

TBCB update

Tariff-based competitive bidding (TBCB) has grown significantly over the years, resulting in reduced prices, faster project execution, greater private sector participation and enhanced grid capacity and resilience.

As per the Central Electricity Authority (CEA), as of August 2025, a total of 85 transmission projects have been awarded through the TBCB mechanism. Of the total awarded projects, 42 projects with a transmission line length of 20,209 ckt km and transformation capacity of 189,100 MVA were secured by Power Grid Corporation of India Limited (POWERGRID) and 43 projects by private transmission service providers. As of August 2025, a total of 67 transmission projects have been commissioned under the TBCB route.

Key private players in the transmission segment are Resonia (erstwhile Sterlite), Adani, Tata Power, IndiGrid, GR Infra, Apraava Energy, Dineshchandra R. Agrawal Infracon Private Limited and Reliance.

In June 2025, Adani Energy Solutions secured an interstate transmission system (ISTS) project, titled “Network Expansion Scheme in WR to Cater to Pumped Storage Potential near Talegaon”, in Pune, Maharashtra. The project, scheduled to be commissioned in January 2028, entails the establishment of a 2×1,500 MVA, 765/400kV substation near Kalamb and associated infrastructure with 3,000 MVA of transformation capacity.

In December 2024, Sterlite Power acquired the project special purpose vehicle, Fatehgarh III Beawar Transmission Limited, from bid process coordinator PFC Consulting Limited. The project was awarded under the TBCB process. It entails developing a 350 km transmission corridor at the 765 kV voltage level from Fatehgarh III to Beawar in Rajasthan. It will strengthen green power evacuation from renewable energy zones in Fatehgarh (9.1 GW), Bhadla (8 GW) and Ramgarh (2.9 GW).

In March 2025, IndiGrid received a letter of intent from REC Power Development and Consultancy Limited to develop an interstate transmission project under the BOOT model within the TBCB framework. The project, Transmission Scheme for Evacuation of Power from the Ratle HEP (850 MW) and the Kiru HEP (624 MW): Part-A, aims to facilitate the evacuation of power from hydroelectric power plants (HEPs).

Key policy and regulatory developments

PMU guidelines

In March 2025, the CEA notified guidelines on a unified philosophy for the placement of phasor measurement units (PMUs) in India’s electricity grid. These guidelines aim to improve grid monitoring and reliability by standardising PMU installation requirements across the country’s power transmission network. These guidelines are applicable to all future projects based on the regulated tariff mechanism (RTM) and TBCB. They will also be applicable to projects (awarded through TBCB or RTM) where price bids have not yet been submitted but tenders were issued prior to the release of these directives.

Amendments to SBD for TBCB projects

In June 2025, amendments were introduced to the standard bidding document (SBD) for TBCB, applicable to firm and despatchable renewable energy projects as well as competitive bidding processes for procuring power from solar, wind and solar-wind hybrid projects. The amendments address project developers’ concerns around regulatory approvals for power supply agreements (PSAs) and delays in tariff implementation. Key changes include a reduction in the performance bank guarantee requirement from 5 per cent to 3 per cent of the expected project cost in order to ease the financial burden on project developers; permission for distribution licensees to approach the relevant electrical regulatory commission to avoid PSA validation delays; and a stipulation that non-adherence to SBDs will require prior approval from the appropriate commission.

Manual on transmission planning criteria

In January 2025, the CEA amended the Manual on Transmission Planning Criteria, 2023. The updated version introduces a uniform approach to inter/intra-state transmission system planning. It ensures the system can manage multiple load generation scenarios and contingencies, coordinates transmission system expansion with power and load growth to avoid unnecessary expenditures, and highlights the need for customers and utilities to submit network access requirements with justification well in advance.

Further, the amended manual on transmission planning criteria recognises the role of platforms such as the PM Gati Shakti National Master Plan, appropriate intra-state transmission planning, an integrated communication plan to ensure the safe and reliable operation of the grid, and technical guidelines to develop a robust electricity transmission system.

Payment for transmission line RoW

In March 2025, the Ministry of Power released supplementary guidelines for calculating compensation related to the right of way (RoW) for transmission lines in accordance with Section 67 (provision as to opening up of streets, railways, etc.) and Section 68 (overhead lines) of the Electricity Act, 2003.

The supplementary guidelines address challenges related to land acquisition and compensation, ensuring that payments reflect actual land value and providing transparency to stakeholders. The guidelines are applicable exclusively to interstate transmission system (ISTS) lines where landowners have contested compensation on the grounds that circle rates are lower than market rates. The market pricing committee is entrusted with determining the market rate of land. The supplementary guidelines aim to address the gaps in prior guidelines to provide a more open and fair procedure for land acquisition and compensation.

Amendment to connectivity and GNA regulations

In September 2025, the Central Electricity Regulatory Commission notified Connectivity and General Network Access to the inter-State Transmission System (Third Amendment) Regulations, 2025, implementing comprehensive procedural and structural improvements.

The amendments include key provisions such as the reallocation of unoccupied terminal bay capacities within ISTS clusters, new rules for modifications in renewable sources for connectivity, and updated compliance requirements for land and financial closure. The third amendment also addresses the management of bank guarantees and the withdrawal of applications. It expands connectivity eligibility to small power producers connected through renewable park developers.

Further, the GNA amendment introduces new compliance monitoring frameworks, requiring regional load despatch centres to publish utilisation statistics, and strengthens control measures for transmission connection grantees from the application stage to the commercial operation date.

National Electricity Plan

In October 2024, the CEA released the National Electricity Plan (NEP)-Transmission, outlining the transmission network requirements up to 2031-32. Based on a peak electricity demand of 277 GW and an installed electricity generation capacity of 609.6 GW as per the 20th EPS report by 2026-27, NEP-Transmission plans the addition of approximately 114,687 ckt km of transmission lines and about 776,330 MVA of transformation capacity at 220 kV and above during 2022-27. Also, the addition of about 1,000 MW of HVDC bipole capacity is envisaged over the same period.

Given a peak electricity demand of 366 GW and an installed generation capacity of 900 GW by 2031-32, as per NEP-Generation, NEP-Transmission envisages the addition of about 76,787 ckt km of transmission lines and 497,855 MVA of transformation capacity at 220 kV and above during 2027-32. An additional 32,250 MW of HVDC bipole capacity is projected to be added during 2027-32.

By the end of 2026-27, transmission line length and transformation capacity is projected to reach 571,403 ckt km and 1,847,280 MVA respectively. Meanwhile, by the end of 2027-32, transmission line length and transformation capacity are expected to stand at 648,190 ckt km and 2,345,135 MVA respectively. HVDC bipole capacity is projected at 34,500 MW by 2026-27 and 66,750 MW by 2027-32.

Interregional transmission capacity additions are envisaged at 30,690 MW during 2022-27, taking the cumulative power transmission capacity to 142,940 MW by 2026-27. For 2027-32, an addition of 24,600 MW is estimated, bringing the total power transmission capacity to 167,540 MW by 2031-32.

Cross-border links will play a key role in the energy transition. Grid interconnections have allowed India and neighbouring countries to efficiently utilise surplus renewable electricity. NEP-Transmission envisages increasing power transfer capacity to 7,000 MW by 2026-27.

With the rise of renewable energy, storage systems have become critical to absorb surplus clean energy and reduce curtailments. NEP-Transmission projects a battery energy storage system (BESS) capacity of 8,680 MW by 2026-27 and 47,244 MW by 2031-32.

The investment requirement for additional 220 kV transmission systems by 2027 is estimated at Rs 4,252.22 billion, including Rs 2,691.5 billion for ISTS and Rs 1,560 billion for the intra-state transmission system. For 2031-32, an investment of Rs 4,909.2 billion is required, including Rs 3,916.24 billion for ISTS and Rs 992.96 billion for intra-state transmission systems.

Green energy evacuation

With the rapid growth of clean energy resources, the electricity transmission grid faces multiple challenges in maintaining reliable grid operation. To ensure safe evacuation of renewable energy, the government has prioritised the establishment of energy storage facilities to optimise the use of transmission infrastructure. Plans are being made to build new transmission networks both between and within states to keep pace with the renewable capacity expansion. Efforts are being made to strengthen transmission interconnections, enhancing voltage stability and angular stability, and reducing losses. Provisions for central financial assistance have been made to support states in building transmission infrastructure for clean energy integration.

Green energy corridors

Green energy corridors support India’s renewable ambitions with the reliable evacuation and integration of large volumes of variable wind and solar power from resource-rich regions to demand centres. They reduce curtailment, improve grid stability, and provide specialised intra- and interstate transmission capacity, control technologies and grid enhancements, ensuring cost-effective and round-the-clock supply of electricity.

GEC-I

The Intra-State Transmission System Green Energy Corridor Phase-I (InSTS GEC-I) scheme is being implemented by the state transmission utilities (STUs) of eight renewable energy-rich states – Andhra Pradesh, Gujarat, Himachal Pradesh, Karnataka, Madhya Pradesh, Maharashtra, Rajasthan and Tamil Nadu – to establish 9,767 ckt km of transmission lines and 22,689 MVA of substation capacity, facilitating the integration of 24 GW of clean energy.

States such as Karnataka, Madhya Pradesh, Rajasthan and Tamil Nadu have completed their projects, while states like Andhra Pradesh, Gujarat, Himachal Pradesh and Maharashtra received scheme extension till June 2025, with further extensions requested till December 2025. With respect to financial progress, as of July 2025, over Rs 28.39 billion has been released against the sanctioned grant of Rs 31.64 billion.

GEC-II

The Green Energy Corridor-II (InSTS GEC Phase II) is being executed in Gujarat, Himachal Pradesh, Karnataka, Kerala, Rajasthan, Tamil Nadu and Uttar Pradesh to establish 7,919 ckt km of transmission lines and 24,488 MVA of substations to evacuate 20 GW of clean energy.

GEC-III

The Indian government plans to advance the third phase of the GEC scheme to enhance intra-state renewable energy transmission capability. Under the union budget for 2025-26, the allocated funds for GEC-III is estimated at Rs 560 billion, of which the central government will contribute about Rs 224 billion or 40 per cent of the total budget. The remaining funds will come from state governments and stakeholders. Key states in this phase include Gujarat, Rajasthan, Maharashtra, Karnataka and Andhra Pradesh, with over Rs 290 billion projected from Gujarat.

Technology implementation

Transmission utilities are increasingly adopting predictive maintenance techniques that leverage data analytics to monitor equipment condition and make proactive decisions. Drones equipped with thermal imaging, high resolution and corona cameras are being used to monitor transmission lines, substations and reactors in real time. This approach has proven better, cheaper and faster than traditional ground-based methods. To create precise digital copies of transmission lines and towers, aerial surveillance and remote inspection technologies are being deployed. These smart digital twins are combined with artificial intelligence (AI) to enable better maintenance and record-keeping.

The digital revolution is reshaping the transmission workforce. Substation automation, AI-driven fault identification and drone-based inspections require a blend of basic transmission expertise as well as skills in data science, IT and analytics. In this regard, POWERGRID has implemented digital tools to optimise labour procedures such as drone-based patrols and predictive outage management. Its asset management via the Artificial Intelligence in Transmission (AMRIT) system uses AI and image-processing technology to detect faults in transmission lines.

Issues and the way forward

The electricity transmission segment continues to face project planning and execution challenges. The timely construction of green electricity transmission infrastructure, particularly at the intra-state level, is often hampered by execution-related issues. Unlike ISTS projects, which benefit from centralised planning and safe cost recovery systems, intra-state lines are executed by STUs with limited funding. Weak creditworthiness and restricted access to concessional financing add to these problems.

RoW challenges further delay project execution. Land acquisition disputes, often fuelled by compensation requests surpassing state-mandated rates, have delayed transmission infrastructure development and led to significant cost overruns.

Institutional complexities also pose challenges. Electricity, being a concurrent subject, enables both central and state governments to exercise planning and regulation. While this framework promotes decentralised decision-making and role clarity, the multiple layers of approval can increase delays and uncertainty across project stages, from planning to grid integration.

The shortage of equipment/components, such as extra high voltage (EHV) transformers, wires and other hardware, coupled with import restrictions has delayed timelines and increased costs for both state and private licensees. Regulations such as the General Financial Rules, 2023 have further complicated equipment procurement, particularly from neighbouring countries.

Technical challenges such as voltage instability, recurrent outages of EHV lines and partial compliance with grid standards have resulted in the underutilisation of transmission infrastructure. These issues have limited the evacuation of renewable energy capacity during peak generation hours, impacting the efficient use of transmission corridors in India. On the regulatory front, cost recovery, tariff design and time/cost overrun pass-through uncertainties reduce private investors’ risk appetite, delaying financial close and execution.

Nevertheless, emerging technologies such as AI , drones and predictive maintenance are expected to enhance operational efficiency and reduce downtime. Going forward, India must leverage its human capital, strong supply chains and supportive policies to establish a resilient transmission infrastructure.