By Dominic Scott, Senior Adviser; Raj Addepalli, Senior Adviser; and Alejandro Hernandez, Energy Systems Innovation Program Director, Regulatory Assistance Project (RAP), with thanks to Sushil Kumar Soonee and Deborah Bynum, RAP, for their assistance

The Indian economy is growing at a rapid rate and, as a result, the need for power is rising. The power system needs additional generation resources to meet these new loads and replace retiring generation. The nation will require new central or large-scale generation, both renewable and thermal, in the foreseeable future. Policymakers are deeply concerned about ensuring adequate resources to meet the system’s future reliability needs, which raises the question of how to attract new economic generation resources and retain existing resources. The current federal structure and the decentralised, multilateral scheduling approach for generation resources potentially carry inefficiencies in despatch and capacity consolidation.

At the same time, competitive electric wholesale markets are evolving in the country. A competitive market allows for the entry of “merchant” generation that relies solely on market-based revenue streams, without the need for long-term contractual support from discoms. Developing a competitive wholesale market paradigm where merchants can thrive, however, will take a significant amount of time. Meanwhile, there will continue to be a need for some kind of long-term contracts between discoms and independent power producers (IPPs) to provide assurance that generators can recover their investment costs.

The question then is how these contracts should be structured. Should they be modelled after many current power purchase agreements (PPAs) that are “physical” in nature (discussed in the next section), or should the sector move to a financially settled contract (FSC) structure that serves the same purpose but could be more efficient?

In this article, we describe the features of a physical PPA versus an FSC and the criteria for evaluating them, before articulating the benefits of moving to FSCs from traditional physical PPAs. The recent development of the virtual PPA route for large private consumers and the growing discussion around accommodating financial instruments, such as contracts for differences (CfDs), more broadly in regulation, point to the growing recognition of the potential of FSCs as a primary tool for striking future long-term contracts. As discussed in later sections, FSCs not only support project finance, but they also provide incentives consistent with market price signals, thus increasing efficiency in the system.

Physical PPAs versus FSCs

In a physical PPA, the buyer generally commits to purchase physical electricity. As the buyer owns the electricity, this is called a “physical” trade. By contrast, an FSC does not involve the physical delivery of power. The buyer, therefore, does not “own” the electricity, but rather the financial flows in the FSC enable the buyer to purchase energy from the market, effectively at the price determined in the FSC. The generator will sell into the market; they will have stronger incentives shaping their operation of the power plant under an FSC, based on market price signals.

Physical PPAs tend to be long term in nature, such as 10-20 years, whereas FSCs can range from short to medium to long term. Both can be bilaterally negotiated between the buyer and seller, but some FSCs can also be traded in organised financial markets. They can both be structured to provide certainty in revenue to the IPP and provide a hedge to the buyer. However, each structure has different implications regarding the incentive signals for commitment and despatch of the power plants, as well as the alignment of generator operations with market price signals, which thus affects the overall efficiency of the system.

Presently, the dominant type of contract in India is physical PPAs, with 87 per cent of energy contracted through PPAs of medium- to long-term structure.

FSC instruments

The financial instruments used in power contracts could include call options, CfDs, futures, forwards, swaps and similar mechanisms. With a call option, the buyer pays a “call premium” to the seller for the right to a payment of the excess of the market clearing price over a contracted strike price for capacity contracted. With a CfD, the buyer and seller agree to a contract strike price. If the market clearing price is higher than the strike price, the seller pays the difference between the market price and strike price to the buyer and vice versa if the market clearing price is lower. In (financial) forward markets, commitments are made by buyers and sellers for financial flows that allow parties to lock in a price for the purchase and sale of a given quantity of energy in the future. Futures markets are like forward markets but offer more standardised products by organised market makers. Swaps involve two parties that exchange cash flows from different financial instruments or assets over a specified period.

With all these instruments, there is no physical exchange of electricity between buyers and sellers, and financial flows are independent of the physical behaviours of resources, such as whether they are offered to the market. However, the buyers and sellers could agree on additional contractual terms if they choose. This might include, for example, a requirement for FSCs to be linked to a physical electricity generation asset, existing or new build, as is standard with renewable CfDs in Britain and call options for despatchable plants in Italy.

Use case example for FSCs

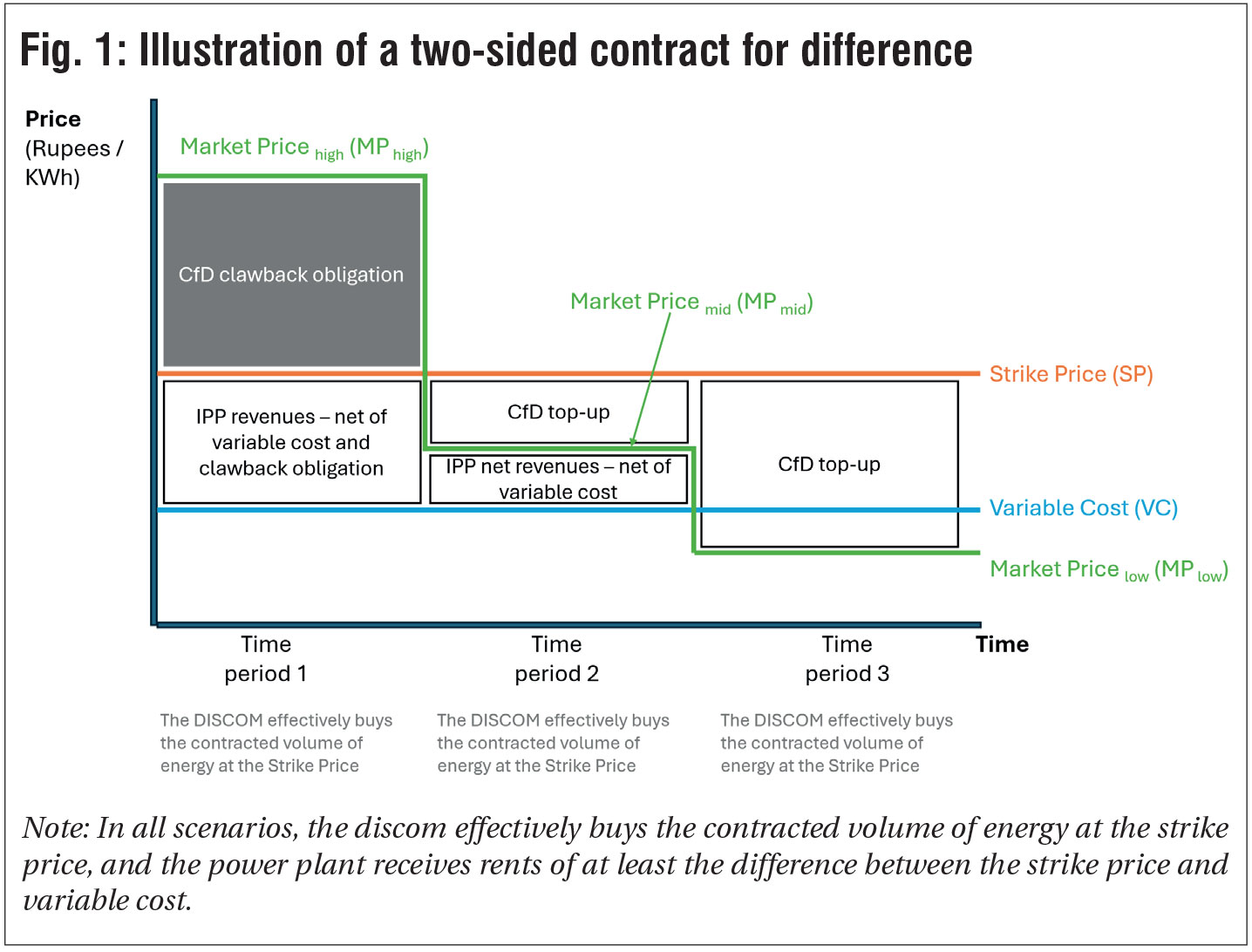

In a simplified example that could apply to a thermal plant, assume a two-sided CfD is struck for a given volume of capacity between a buyer (discom) and a seller (IPP), with a strike price ideally discovered in a competitive auction that is above the IPP’s variable cost. Assume a design where financial flows are independent of the actual physical scheduling of the contracted resource; instead, financial flows link only to the difference between the strike price and market clearing price. In Fig. 1, we present three scenarios, where:

- The market price is higher (MP high) than the strike price (SP)

- The market price (MP mid) is lower than the strike price but above the variable cost (VC)

- The market price (MP low) dips below the variable cost

- The implications for both the buyer and seller are as follows:

- When the market price is higher than the strike price, the IPP will have an incentive to offer and sell its output in the market. This is because, regardless of whether it offers the resource to the market, it has a “clawback” obligation under the CfD to return to the buyer the difference between the market price and strike price (MP high-SP) for each unit of capacity contracted in the CfD. Selling on the market at a price higher than the strike price means it enjoys net revenues of the high market price minus the variable cost (MP high-VC), which can finance the cash outflows for the difference between the high market price and the strike price (MP high-SP). Thus, the IPP retains the difference between the strike price and variable cost that will help cover its fixed costs. The buyer, on the other hand, has a cash outflow for purchasing power from the market at a price that exceeds the strike price, and receives a cash inflow of the market price minus strike price (MP high -SP) from the IPP, for a net price of the strike price. Thus, the buyer and seller have effectively hedged and the IPP has the correct incentive to operate according to the market signals.

- When the market price is lower than the strike price but higher than the variable cost, the IPP receives from the buyer a “top-up” payment of the strike price minus market price (SP-MP mid), irrespective of whether it offers the capacity to the market. This leaves the incentive intact for the IPP to offer and sell its output in the market. The IPP’s resulting net cash inflow from the market will be the market price minus the variable cost (MP mid-VC) and from the buyer strike price minus market price (SP-MP mid). The IPP essentially retains as a margin the difference between the strike price and the variable cost that will help cover its fixed costs. The buyer, on the other hand, has a cash outflow for purchasing power from the market at this market price and pays to the IPP an amount of the strike price minus the market price (SP-MP mid) for a net price of the strike price. Thus, the buyer and seller have effectively hedged, and the IPP has the correct incentive to operate as the market price dictates.

- When the market price is below the IPP’s variable cost, the IPP receives from the buyer a “top-up” payment of the strike price minus market price (SP-MP low), irrespective of whether it offers its output to the market. For the IPP, the value of offering and selling its output in the market is negative, as the variable cost exceeds the market price. So, the resource is, correctly, not scheduled in the market. Thus, the IPP’s net cash inflow from the market is zero, and the buyer provides the IPP with a margin of the strike price minus market price (SP-MP low) that will help cover its fixed costs. In this transaction, the buyer has a cash outflow for purchasing power from the market at the SP. In sum, the buyer has effectively hedged, the IPP has correct incentives to operate accordingly (in this case, by not scheduling in the market), and the IPP has a margin to contribute towards fixed cost recovery. The bumper margins for the IPP in time period 3 (Fig. 1) may, to some extent, be captured by consumers through competition in setting the strike price.

This example illustrates how a CfD helps provide revenue certainty for the IPP if it operates in alignment with market prices. It shows how the CfD provides signals for resources to ensure they are available to schedule when prices are high, and to refrain from scheduling when they are so low that the resource is not in merit. It also shows how CfDs can limit the buyer’s exposure to high prices. Instruments like FSCs send efficient signals to flexible resources that accommodate the variability of renewables. This benefit will only grow in value as the share of renewables in India increases and prices become more volatile. FSCs, therefore, help future-proof the system.

Criteria for evaluating physical versus financial contracts

There are several relevant criteria for evaluating which type of contract is preferred. They include:

- Alignment of the generator’s operation incentives with market price signals:

- IPPs should operate when it is economical to do so, including efficient scheduling.

- Availability during system scarcity, guided by market price signals.

- Remove or minimise the IPP’s incentive to exercise market power.

- The certainty, stability and predictability of revenue streams to the IPP, to enable it to finance the investment.

- Regulatory certainty for buyers and sellers.

- Fair pricing for both buyer and seller.

- The contribution to resource adequacy to maintain system reliability.

Benefits of FSCs over traditional physical PPAs

Both traditional PPAs and FSCs provide revenue certainty to the sellers, the IPPs. They also provide price certainty to the buyers. Both support resource adequacy under the right underlying regulatory framework, such as a requirement that FSCs be tied to a physical resource, and in the structure of resource adequacy penalty and settlement arrangements. (Note: potential “free-rider” problems – where under-contracted discoms rely on energy supplied from capacity contracted through FSCs by other discoms without contributing to the cost of that capacity – could be addressed by imposing significant penalties for shortfalls.) In certain existing physical PPAs, the terms and conditions of a contract are such that some generators are not scheduled even if their marginal running or variable cost is less than the market price, and sometimes they are scheduled even if their marginal cost is higher than the market price. This happens at times because generation scheduling currently follows a decentralised merit order, where each discom may optimise only within its own portfolio. This reduces the efficiency of the system and costs consumers money.

FSCs overcome this problem by motivating resources to participate in markets, where they are instead scheduled according to the overall merit order rather than within individual silos of each discom’s contracted resources. These contracts drive efficient scheduling behaviour when there is a system scarcity. Thus, FSCs provide better incentives for the generator to operate in alignment with market price signals.

In sum, the FSC allows for:

- Greater market liquidity assists price discovery, reveals important information about the value of different resources and informs investment choices.

- Surplus capacity of any discom to be identified in the market and scheduled by other discoms, ensuring resources are not operated in silos. This supports efficient scheduling.

- IPPs to have an incentive signal to offer their output into the market at their marginal cost and to self-curtail when market prices fall below their variable costs.

- Signals to IPPs as to when to take a plant off for maintenance, that is, when market prices are lowest or even negative.

- More visibility of market schedules, which assists the system operator when forming plans to accommodate the expected energy mix (for instance, ensuring sufficient inertia).

- Minimising the potential for generators to exert undue influence in the market. Market prices above the strike price will not benefit the IPP’s contracted capacity under the CfD.

Conclusion

As discoms seek new long-term PPAs with IPPs, we recommend they strongly consider the use of FSCs rather than the traditional physical PPAs. Policymakers can help capture the benefits of FSCs by fostering their implementation in regulatory arrangements. The FSC, as demonstrated above, will improve efficiency in the system and lead to lower generation costs and prices for consumers, while retaining revenue certainty for IPPs and embedding a price hedge for buyers, and in so doing, bring multiple wins for India.