By Dr Sapan Thapar, Associate Professor, TERI School of Advanced Studies

By Dr Sapan Thapar, Associate Professor, TERI School of Advanced Studies

Projected to be the fastest-growing economy this fiscal, India will require enabling support from all factors of production to maintain its momentum towards Viksit Bharat @2047, including energy. The power sector has been among the numerous success stories of the country, with the total installed capacity crossing 500 GW (half attributed to cleaner sources), over 2 trillion units being generated, and the energy needs of over 250 million consumers being met. An impressive addition in power generation capacity, led by solar and wind, bridged the supply deficit, enabling universal access to electricity on affordable terms.

However, a key challenge lies in the last leg of the energy value chain, which is the power distribution sector and its (perennially) weak financial health. Discoms, numbering over 70, are saddled with $80 billion of debt and payment dues to generating companies amounting to $7 billion. Most of these utilities experience a high level of aggregate technical and commercial (AT&C) losses due to technical mismanagement, under-recoveries and an indifferent attitude towards consumers. Despite repeated reforms and multiple schemes, cost parity between the annual revenue realised (ARR) and the average cost of supply (ACS) has not been attained, even after accounting for subsidies, indicating a loss on every unit sold. The current value is in the range of Re 0.40 per kWh. We analysed these challenges and offer bold and pragmatic solutions towards ushering in the concept of “one nation, one tariff”.

A major component (70-80 per cent) in tariff build-up is the power purchase cost. However, it varies across discoms, based on the vintage of technology, contracts and portfolio. Consider a solar/coal plant selling power to multiple discoms but at different price points, culminating in non-uniform consumer tariffs across states and even discoms within the same state. Another scenario can be discoms sourcing power from plants set up within their respective states (for instance, pithead coal plants or solar/wind/hydro), giving them an undue advantage in terms of costs, only because of natural resource endowment.

The second issue is multiple tariff slabs, over 20, even within a discom. As per our estimates, over 1,500 different tariff slabs prevail in the country, and these are determined and approved every year. The primary reason is cross-subsidising certain consumer segments (households and agriculture) at the expense of commercial and industrial establishments, making them commercially unviable. It may be important to note that India is among a very few countries that levy higher tariffs on industries/commercial establishments than on consumers. This has led to a flight of large consumers from grid purchases to third-party open access or captive mode plants, further eroding the revenue of discoms, creating a vicious cycle of cross-subsidies. This is a paradox, as states compete to attract private investment, with energy being a key factor.

A primary reason for the current imbroglio is the concurrency of electricity as a subject under the Indian constitution, which makes it difficult to undertake pan-Indian reforms. We propose the following bold but pragmatic solutions…

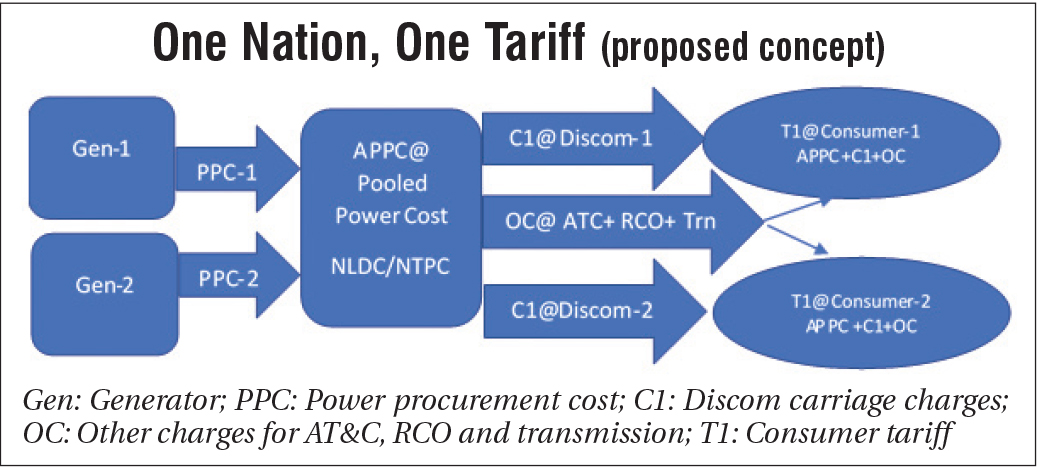

The first is the creation of a national agency (akin to the National Load Despatch Centre) to procure power from multiple generating plants across the country and sell it through another pan-Indian entity (say NTPC Limited) directly to the end-consumers at the same price point. The Ministry of Power Merit (Merit Order Despatch of Electricity) portal can be utilised to derive the average marginal price on a country-wide basis. In addition, the existing expertise of the state electricity regulatory commissions (SERCs) in computing the average power purchase cost (PPC), as a part of the renewable energy certificate/renewable purchase obligation (RPO) mechanism, would prove to be helpful.

The role of discoms would be to serve as network service providers, offering carriage facilities at predetermined rates. The costing can be arrived at by subtracting the PPC from the overall discom expenses, to be averaged for the entire country. A functional example has been the bifurcation of Power Grid Corporation of India Limited (POWERGRID) into multiple entities – Grid Controller of India Limited, which is responsible for maintaining grid stability; Central Transmission Utility of India Limited, serving as the interstate transmission system planner; and POWERGRID, operating as a transmission licensee on pure commercial principles.

The cost of power is not the only factor in deciding the final tariff. There are three associated parameters involved. These are AT&C losses, renewable energy purchase and transmission charges (cum losses), all of which vary widely across states.

States incur charges based on renewable resource endowment, which itself varies significantly in terms of the type of technologies (solar, hydro, wind) and project location. A single national value, in terms of the cost of renewable energy procurement, can ensure meeting India’s renewable energy targets without any bias among states. The expertise of entities like the Solar Energy Corporation of India can be employed to source renewables under transparent bidding processes.

To encourage efficiency in operations, the performance of states/discoms, in terms of decreasing AT&C losses and increasing the renewable consumption obligation (RCO), can be rewarded under the norms of the Finance Commission. The 15th Finance Commission incentivised reforms by linking states’ borrowing with the performance of their discoms. This can be extended under the proposed mechanism as well.

The overarching change would be in terms of the roll-out of GST in the power distribution sector. States may not be inclined, perceiving loss of revenue, similar to the unwillingness shown in the petroleum sector. However, most discoms are running in losses and not making any meaningful contribution to the state exchequer. On the contrary, they depend on state governments to sustain their operations. Even in the case of a positive balance sheet, they are required to socialise their profits (similar to losses) among the end-consumers.

Beyond this, states may seek compensation in lieu of electricity duty, which is typically levied on industrial consumers and varies across states. The total annual duty collection across the country was estimated at Rs 400 billion, which, in unit terms, comes to a meagre Re 0.25 per kWh. Financial support extended by the central government to the state-owned distribution utilities under multiple reform schemes (APDRP, UDAY, RDSS) is far greater than the earnings made by states from electricity duty. State governments can be asked to choose from either levying electricity cess or seeking financial support from the government. This way, they can be nudged towards GST.

A key challenge could be resistance from consumers who have been enjoying subsidised power. The answer lies in coupling decentralised solar subsidy schemes such as the PM Surya Ghar Yojana and PM KUSUM, with a “give-it-up” approach. A similar campaign initiated in 2015 in the liquefied petroleum gas segment led to a large number of consumers voluntarily surrendering their cooking gas cylinder subsidies.

Interestingly, energy generated from a rooftop solar plant would be sufficient to offset the free power offered by discoms. A typical 3 kW solar rooftop system generates 400 kWh per month, almost double the existing free units offered to consumers under prevailing schemes. The financial value of solar power generated, over its 25-year lifetime, would be 50 per cent higher than the total subsidy offered. Consumers availing of subsidy under government schemes can be asked to give up their discounted tariffs.

Interestingly, energy generated from a rooftop solar plant would be sufficient to offset the free power offered by discoms. A typical 3 kW solar rooftop system generates 400 kWh per month, almost double the existing free units offered to consumers under prevailing schemes. The financial value of solar power generated, over its 25-year lifetime, would be 50 per cent higher than the total subsidy offered. Consumers availing of subsidy under government schemes can be asked to give up their discounted tariffs.

The proposed concept, as explained in the accompanying figure, involves determining a common tariff by summing up the average national cost attributed to the following:

- Power purchase

- Discom carriage charges

- AT&C losses

- Transmission charges and losses

- Renewable energy compliance

As an illustration, a commercial entity in State A would pay the same tariff as a household in State B. This would obviate any tariff distinction across states/discoms as well as consumer types. Subsidies to any consumer segment can be directly routed via the direct benefit transfer mechanism. For consumers procuring power under open access, power exchange or captive facilities, standardised network utilisation charges can be levied by discoms.

Regarding the constitutional provisions, learnings can be made from the recent notification on RPO/RCO norms made under the Energy Conservation Act, 2001, and not the Electricity Act, 2003. Other examples include the “One Nation, One Grid, One Frequency” concept, harmonising the power transmission sector, and the Central Electricity Regulatory Commission norms for renewable energy tariffs as well as renewable energy certificates, widely adopted by the SERCs.

In this digital age driven by artificial intelligence, smart meters can be the key enablers. Most people in India are adept at using mobile apps involving commercial transactions (like taxi booking and e-commerce). Smart meters can offer actionable insights to end-consumers based on the prevailing/anticipated demand-supply trends, enabling demand-side management. This can even enable a time-of-day tariff, based on demand-supply patterns and generation schedule, which can be applicable for all consumers.

The suggested measures can usher in One Nation, One Tariff in the country, a kind of renaissance in the power sector, benefitting stakeholders across the value chain. The cost of power supply will get homogenised, reducing the cost of doing business for industrial and commercial entities; the need and quantum of bail-out packages for discoms as well as consumer subsidies will reduce, easing the financial load on the exchequer; the administrative work of SERCs and discoms towards determining tariffs will ease; and consumers will be able to better manage their supply-demand using smart energy systems.

Amidst the steadily increasing electrification of the Indian economy, the suggested pathways will enable a swift and sustainable transition of the power sector.