By Kumaresh Ramesh, Intern; Dominic Scott and Raj Addepalli, Senior Advisers; and Alejandro Hernandez, Programme Director, Regulatory Assistance Project

Financially settled contracts (FSCs) offer multiple advantages compared to traditional physical power purchase agreements (PPAs). While both traditional PPAs and FSCs provide revenue certainty to the sellers and independent power producers (IPPs), as well as price certainty to buyers, FSCs also incentivise generators to make power available in wholesale markets during times of system scarcity. This improves reliability, reduces overall system costs and benefits customers. In addition, FSCs support the use of surplus capacity by discoms, improve market liquidity and enable price discovery – making them an invaluable regulatory tool.

India’s resource adequacy framework places an obligation on discoms to contract sufficient capacity and ensure that performance-based incentives or penalties are built into those contracts – particularly for availability during critical hours. With the right regulatory framework, discoms can use FSCs to present generators with incentives to be available during hours of system scarcity, similar to existing incentives for merchant generators.

System scarcity

Scarcity in the electric system occurs when there is a risk that the electric supply is inadequate to meet customer demand. In an extreme stress scenario, shortages of power could lead to service interruptions- rotating outages or even uncontrolled blackouts. In competitive markets, prices go up when levels of demand approach the limits of supply. Depending on how competitive electric markets are set up, energy prices can significantly increase during these “scarcity hours”. Scarcity can happen due to many factors, including increased loads, unexpected outages of generation and/or transmission facilities and extreme weather, and can be aggravated by a lack of customer demand responsiveness to scarcity. Scarcity pricing is a feature of many competitive wholesale electricity markets. The resulting higher prices incentivise generators to produce more output and consumers to reduce demand.

Note: In addition, the discoms pays the steady premium to the generator

Incentives for generators under “merchant” basis, FSCs and PPAs

In some competitive markets, new generating resources are built on a “merchant” basis, where investors in the generation plant rely primarily or solely on expectations of future market-based revenues. There is no contract between the merchant generating resource and the discom or large consumer. Most markets also have some form of FSCs, and some still have traditional physical PPAs. In these latter two arrangements, a customer or discom contracts with the generator. In this section, we distinguish between these three types of arrangements – traditional PPAs, FSCs and a pure merchant plant – to demonstrate the incentives generators have to operate efficiently and be available to run during scarcity hours when the resource is needed the most. Relying on markets rather than long-term contracts for their revenues and profits, merchant generators are motivated to be available and to operate during scarcity hours when prices are high — higher prices yield higher profits.

India’s traditional thermal PPAs typically have a two-part contract structure – a variable cost (energy) recovery part and a fixed cost (capacity) recovery part. In the energy part of the tariff, the generator is paid its variable operating costs, which are linked to fuel prices. In the capacity part of the tariff, the generator is paid its fixed costs such as debt servicing, equity return, operation and maintenance expenses, and insurance. Capacity payments are reduced when monthly or annual availability falls below a specified level, and modest incentives are typically in place for generators who offer higher levels of availability. These incentives, however, are weak and bear no link to the value of the resource to the system at the moment of the outage, so generators have no great motivation to provide availability during scarcity hours. These effects are compounded by the fact that the buyer generally has the first right of refusal for contracted capacity, and sales outside the PPA are generally restricted. In practice, this restricts the generator’s flexibility in accessing merchant markets, as long-term capacity remains locked under the contract.

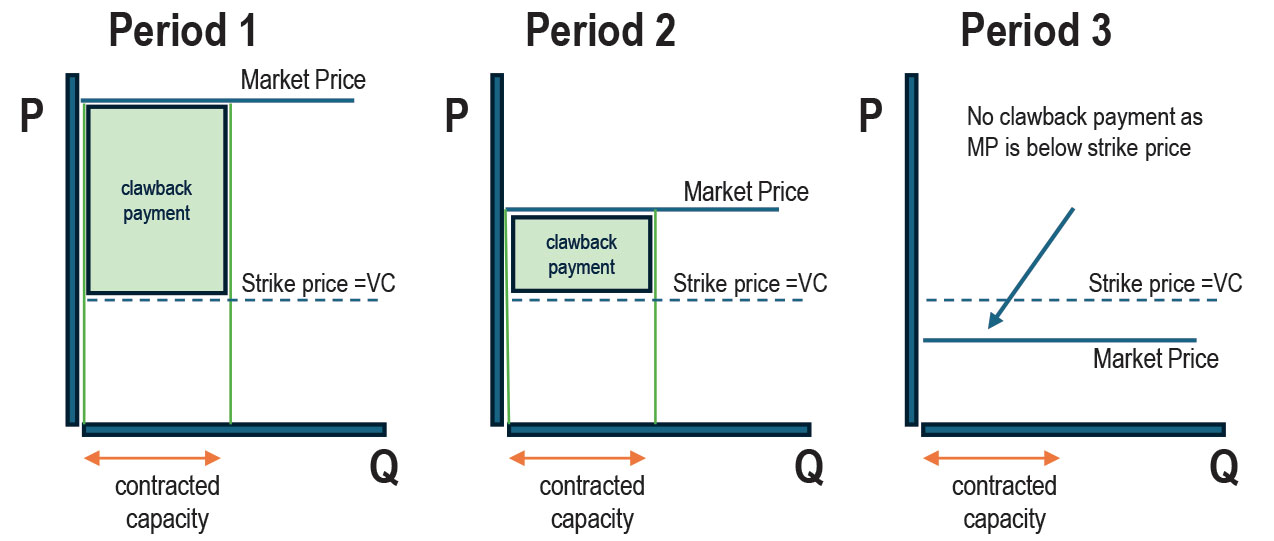

We illustrate below the financial settlement under an FSC using the example of a call option for a thermal plant, where the buyer pays the seller a call option premium that covers the generator’s fixed costs. A strike price is set by the procuring entity, say indexed to an estimate of the generator’s variable cost (VC), shown constant in the figure below for simplicity. When the market price exceeds the strike price – and therefore the variable cost of the generator – the call option is exercised, and the generator must pay the buyer a “clawback payment”, the difference between the market price and the strike price. The diagram shows the operation of the call option in three illustrative time periods with different market prices: high, medium and low.

If the generator produces and sells into the market, it receives the market price and can use this to cover its financial obligation and its variable costs. The generator’s net revenue after this is the call option premium, and it recovers its fixed costs. The buyer pays the market price and the call option premium, but will receive from the generator the difference between the market price and the strike price in a clawback payment. The buyer thus pays out the call option premium, and thanks to the clawback payment, can buy energy in the market for no more than the strike price.

The FSCs provide stronger incentives for generators to operate, especially during scarcity hours, to capture the higher market prices and finance the obligation to return the difference between the market price and the strike price to the buyer. If the generator does not run – and so does not receive the benefit of the higher market prices – it must use its own cash reserves to finance the call option obligation when exercised. The incentives the FSC provides to operate during scarcity hours are comparable to those of a merchant generator, due to the market-based nature of the revenues.

Finally, given that FSCs incentivise contracted generators to be available during scarcity, the typical concern that a generator may exercise market power through economic or physical withholding is eliminated.

Example

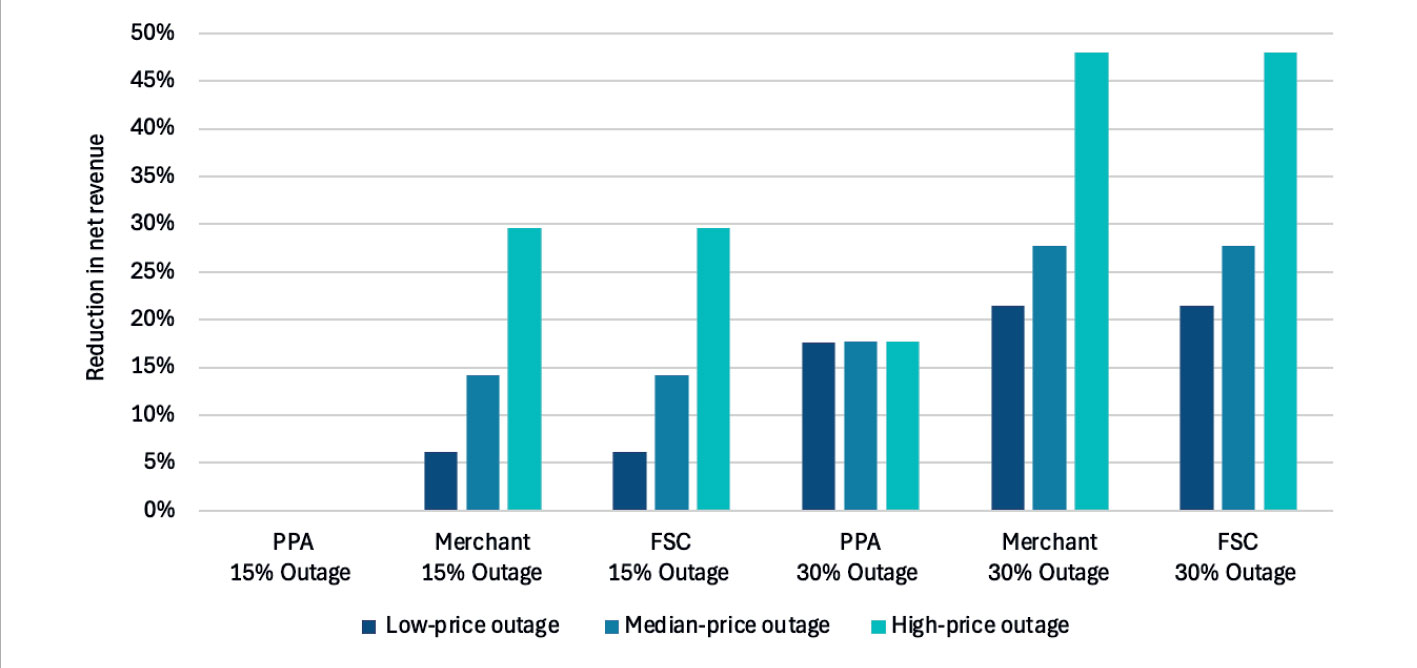

We illustrate these incentives under the three contract structures – merchant generators, traditional thermal PPAs and FSCs (a call option) – through a simple simulation exercise. Traditional PPAs typically require a normative availability of 85 per cent. Thus, the contracted plant may be allowed up to 15 per cent of non-availability without any reduction on the fixed payments (that is, the fixed component of the PPA, the equivalent of the call option premium in an FSC).

We simulate the financial impact for contiguous loss-of-generation events (outages) lasting 15 per cent and 30 per cent of the year, using historic market prices for 2023-24. Each of the outages is simulated for three possible market price windows – the lowest, middle and highest market prices (these do not link with the three periods shown in Figure 1).

The figure below shows, for each case, the net revenue reduction as a share of the total net revenue for the generator. It shows that the loss of net revenue under the FSC contract aligns with that of the merchant plant. For example, a 15 per cent outage when market prices are highest would result in the FSC plant (call option) losing around 30 per cent of its net revenue, comparable to a merchant plant. When the duration of the outage is 30 per cent, the net revenue reduction for the FSC is around 45 per cent, again comparable to the reduction for a merchant plant. In comparison, for the traditional PPA, there is no impact on net revenue at a 15 per cent outage duration. This is because fixed cost recovery is pegged to the normative plant availability of 85 per cent. Thus, the plant receives the same capacity payment even at 85 per cent availability, irrespective of its availability during scarcity hours. Although at a 30 per cent outage level, it faces an 18 per cent drop in the net revenues – this is still far less than the drop experienced by the merchant or FSC plants. The plant under the PPA is completely indifferent, whether the 30 per cent outage occurs during high-, median- or low-price hours.

The figure below shows, for each case, the net revenue reduction as a share of the total net revenue for the generator. It shows that the loss of net revenue under the FSC contract aligns with that of the merchant plant. For example, a 15 per cent outage when market prices are highest would result in the FSC plant (call option) losing around 30 per cent of its net revenue, comparable to a merchant plant. When the duration of the outage is 30 per cent, the net revenue reduction for the FSC is around 45 per cent, again comparable to the reduction for a merchant plant. In comparison, for the traditional PPA, there is no impact on net revenue at a 15 per cent outage duration. This is because fixed cost recovery is pegged to the normative plant availability of 85 per cent. Thus, the plant receives the same capacity payment even at 85 per cent availability, irrespective of its availability during scarcity hours. Although at a 30 per cent outage level, it faces an 18 per cent drop in the net revenues – this is still far less than the drop experienced by the merchant or FSC plants. The plant under the PPA is completely indifferent, whether the 30 per cent outage occurs during high-, median- or low-price hours.

Due diligence

While FSCs offer significant benefits, effective safeguards are essential to ensure smooth implementation. Selecting a reliable, liquid reference price is critical. With over a dozen possible benchmarks across exchanges, care is needed to ensure efficiency and relevance. Regulatory price caps could affect the uptake of FSCs, and specific rules may be needed in case of energy rationing. For renewable contracts for difference, using day-ahead prices may create distortions in behaviours in subsequent markets, which can be mitigated by linking the FSC to a benchmark plant rather than the generator’s own output.

Indexing the strike price to input costs helps hedge fuel price volatility for thermal plants. But discoms should guard against inflated input cost claims that could raise strike prices. Regulators may need to review contract prudence and resolve related disputes.

There may be concerns that resources will manipulate market prices under FSCs. However, FSCs generally reduce incentives to manipulate market prices, as any excess of market price over strike price is returned to buyers through the clawback mechanism. To avoid purely “paper” contracts, counterparties without physical assets should provide guarantees or be required to demonstrate a separate contract with a link to physical capability.

Clauses for repayment upon failure to build can reinforce discipline, as practiced in Britain’s capacity market.

A pilot phase — with limited participants and capacity caps — can help regulators identify risks and gaps. Discoms can strengthen valuation and risk-management capacity. Generators must manage the performance risk transferred to them — as the party best placed to manage this risk — from discoms under FSCs. Transparency requirements, such as regulatory disclosure of large FSC positions (subject to confidentiality), can further reduce manipulation risk.

Conclusion

As discoms and large consumers move forward with new long-term contracts with thermal IPPs, they can consider using FSCs rather than traditional physical PPAs. FSCs will improve reliability by providing incentives for generators to be available during scarcity hours, improve efficiency and lead to lower costs for consumers, while retaining revenue certainty for IPPs that align their operation with the needs of the system. Policymakers can support them by accommodating their implementation in regulatory arrangements.