By Dr Rajib Mishra, Executive Director (D), IRADe; Dr Navpreet Saini, Senior Research Analyst, IRADe

By Dr Rajib Mishra, Executive Director (D), IRADe; Dr Navpreet Saini, Senior Research Analyst, IRADe

India’s long-term development ambitions are reshaping the country’s industrial landscape. Targets such as achieving a $5 trillion economy, becoming the world’s third-largest economy, reaching net-zero emissions by 2070 and transitioning into a developed nation by 2047 will require massive investments in infrastructure, manufacturing, energy systems and advanced technologies. Metals such as steel and aluminium will be at the heart of this transformation. In this context, aluminium occupies a uniquely strategic position due to its lightweight nature, durability, corrosion resistance, versatility and high recyclability.

As India expands its cities, transport networks, power infrastructure and manufacturing base, aluminium will increasingly substitute heavier and less efficient materials. At the same time, the global shift towards clean energy and low-carbon technologies is further amplifying aluminium demand. Whether in renewable energy systems, electric vehicles, power transmission, or modern construction, aluminium is becoming indispensable to the country’s economic and energy transition.

Green aluminium is achieved by producing aluminium with clean electricity (hydro, solar, wind or nuclear), more efficient smelting technologies, maximising recycling and reducing emissions across mining, refining and manufacturing, while accurately measuring and certifying its carbon footprint. This approach drastically cuts pollution, complies with tightening global climate regulations, avoids future carbon taxes such as carbon border adjustment mechanism (CBAM). Further, this approach helps companies meet their net-zero and environmental, social and governance (ESG) commitments without compromising aluminium’s strength, light weight, or versatility, making green aluminium the emerging global standard for industry and infrastructure.

Globally, green aluminium is preferred because governments, industries and consumers are increasingly demanding materials with low embedded carbon to meet climate targets and trade regulations. With the introduction of carbon border taxes, stricter ESG norms and net-zero commitments by major global companies, high-carbon aluminium is becoming costly and risky, while green aluminium enjoys easier market access, lower compliance costs and stronger demand from sectors such as automobiles, renewable energy, construction and electronics. As a result, green aluminium is no longer a niche product but is rapidly becoming the default choice in international markets.

Demand dynamics: Infrastructure, energy transition and consumption gap

Large investments in urban infrastructure, transport systems, housing and industrial corridors have translated into sustained growth in aluminium consumption. This demand-side momentum is reflected in India’s production trends. Alumina production increased from 3,610 thousand tonnes in 2012–13 to 7,230 thousand tonnes in 2021–22, registering a compound annual growth rate (CAGR) of about 7 per cent. Aluminium production grew even faster – from 1,720 thousand tonnes to 4,017 thousand tonnes during the same period – at a CAGR of approximately 9 per cent.

Despite this growth, India’s aluminium consumption remains well below global benchmarks. Aluminium is the second most used metal in the world, with global consumption estimated at about 88 million tonnes in 2021 and projected to reach nearly 120 million tonnes by 2030. However, India’s per capita aluminium consumption stands at only about 2.7 kg, compared to a global average of roughly 11 kg per capita. This wide gap highlights the significant untapped potential for aluminium demand in India as incomes rise and modern infrastructure becomes more widespread.

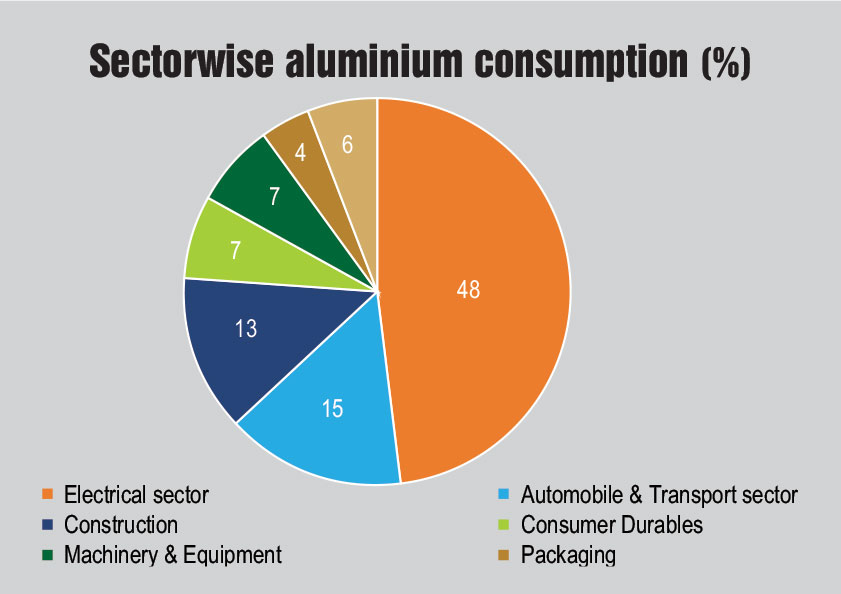

Sector-wise, aluminium consumption in India is dominated by the electrical sector, which accounts for nearly 48 per cent of the total use. The automobile and transport sector accounts for around 15 per cent of the consumption, followed by construction (13 per cent), consumer durables (7 per cent), machinery and equipment (7 per cent), packaging (4 per cent) and other uses (6 per cent). In the automotive sector, aluminium can reduce vehicle weight by up to 40 per cent compared to steel, significantly improving fuel efficiency and extending the driving range of electric vehicles.

At the same time, India’s growing reliance on aluminium imports to meet the domestic demand, particularly aluminium scrap, is a cause for concern. The heavy dependence on scrap reflects the expanding role of recycling in meeting the domestic demand, but it also indicates competitive pressure on domestic primary aluminium producers.

Production landscape: Resource strength and industry structure

India’s aluminium industry is anchored in its substantial natural resource base. The country possesses nearly 4 billion tonnes of bauxite reserves, providing a strong foundation for aluminium production. This abundance of domestic bauxite reduces raw material costs, ensures supply security and strengthens India’s competitive position in the global aluminium market.

Globally, alumina production stood at about 141 million tonnes in 2022, with China accounting for nearly 58 per cent of the output, followed by Australia, Brazil and India, which contributed around 5 per cent. Despite being among the leading producers, India remains far behind China in terms of alumina as well as aluminium production. Similarly, the aluminium production worldwide was approximately 67 million tonnes in the same year; again dominated by China with a 60 per cent share. India ranked among the top producers, accounting for about 3.5 per cent of the global aluminium output.

Domestically, India’s total installed aluminium production capacity was around 4.1 million tonnes per annum in 2022. The industry is largely controlled by four major producers – National Aluminium Company Limited (NALCO), Hindalco Industries Limited, Bharat Aluminium Company Limited (BALCO) and Vedanta Aluminium Limited. Among these, NALCO is the only public sector enterprise, while the remaining producers are privately owned. Despite NALCO’s presence, the public sector’s overall share in both alumina and aluminium production remains limited, with private players driving most of the capacity expansion and output growth.

Aluminium production involves two broad stages. The upstream stage includes bauxite mining and the refining of bauxite into alumina through the Bayer process. The downstream stage involves alumina to aluminium making through smelting process and processing the aluminium into semi-finished and finished products through casting, rolling, extrusion and fabrication. While recycling also plays an important role in the downstream segment, India’s expanding demand continues to rely heavily on primary aluminium production.

The supercritical challenge: Energy intensity, emissions and decarbonisation

The supercritical challenge: Energy intensity, emissions and decarbonisation

The most critical challenge facing India’s aluminium industry lies in its energy intensity and carbon footprint. Aluminium smelting, which converts alumina into aluminium metal through the Hall–Héroult electrolysis process, is the most electricity-intensive process in aluminium production. Producing 1 tonne of primary aluminium typically requires between 14,000 and 16,000 kWh of electricity. In India, this electricity is predominantly supplied by coal-based captive power plants, making aluminium production a major contributor to industrial carbon emissions.

Although downstream processes such as casting, rolling and extrusion also require energy, their consumption is significantly lower than that of primary smelting. Recycling aluminium is particularly energy-efficient, requiring only a fraction of the electricity needed for primary production.

The reliance on coal-based captive power poses risks beyond environmental concerns. Global markets are increasingly introducing carbon-related trade measures, most notably the European Union’s CBAM, which seeks to impose additional costs on carbon-intensive imports. For Indian aluminium producers, continued dependence on high-emission power sources could undermine export competitiveness and erode cost advantages derived from the domestic bauxite availability.

The way forward

As India moves towards its long-term economic and climate goals, a clear and coordinated pathway is needed to ensure that the aluminium sector remains both competitive and sustainable. First, decarbonising captive power generation must become a priority. Gradual integration of renewable energy—particularly solar and wind—through hybrid power systems, complemented by grid-based cleaner electricity, can significantly reduce the carbon intensity of aluminium smelting. Policy support for open access to renewable power and long-term power purchase agreements will be critical in this transition.

Second, improving energy efficiency across smelting and downstream operations can yield immediate gains. Adoption of advanced smelting technologies can reduce electricity consumption per tonne of the aluminium produced. Encouraging greater use of recycled aluminium, while strengthening domestic scrap collection and processing systems, can further lower energy demand and emissions.

Third, aligning industrial policy with emerging global carbon regulations is essential. Developing credible carbon accounting, product-level emissions disclosure and certification mechanisms for low-carbon or “green” aluminium will help Indian producers maintain access to international markets in the face of measures such as CBAM. Public sector enterprises such as NALCO can play a catalytic role by piloting low-carbon production pathways and setting benchmarks for the industry.

Finally, a stable and forward-looking policy framework is needed to balance growth with sustainability. Investment incentives, research and development support, can accelerate the transition of the aluminium sector. With the right mix of resources, technology and policy alignment, aluminium can become not just a pillar of India’s industrial growth, but also a symbol of its commitment to a low-carbon and self-reliant future.