As part of the thrust towards India’s 2070 net zero target, NITI Aayog has released a series of reports on scenarios towards Viksit Bharat and net zero for various sectors, including power. The report on sectoral insights for the power sector identifies the policy, technological and infrastructure measures required to meet the net zero objective, while maintaining grid reliability, system adequacy and affordability.

Prepared with inputs from an interministerial working group, the study applies a scenario-based modelling framework to assess alternative energy transition pathways up to 2070. It evaluates two scenarios – the current policy scenario (CPS), which extends existing policy trends, and the ambitious net zero scenario (NZS), which aligns with India’s 2070 net zero target. Based on this analysis, the report examines the evolving roles of renewable energy, energy storage, nuclear power, coal-based generation and transmission infrastructure in supporting this transition. Here are the key takeaways from “Scenarios Towards Viksit Bharat and Net Zero – Sectoral Insights: Power”…

Scenario-based modelling

To assess long-term transition pathways, NITI Aayog developed an integrated energy–economy framework that projects sectoral activity and translates it into energy demand and total electricity requirements. The projected electricity demand is then used to estimate capacity expansion, generation mix and emission outcomes under two scenarios. The CPS assumes the continuation of existing policies and historical trends, resulting in the gradual uptake of low-carbon technologies. In contrast, the NZS assumes stronger policy support, faster electrification, higher energy efficiency and large-scale deployment of clean energy solutions. The key modelling results are outlined below.

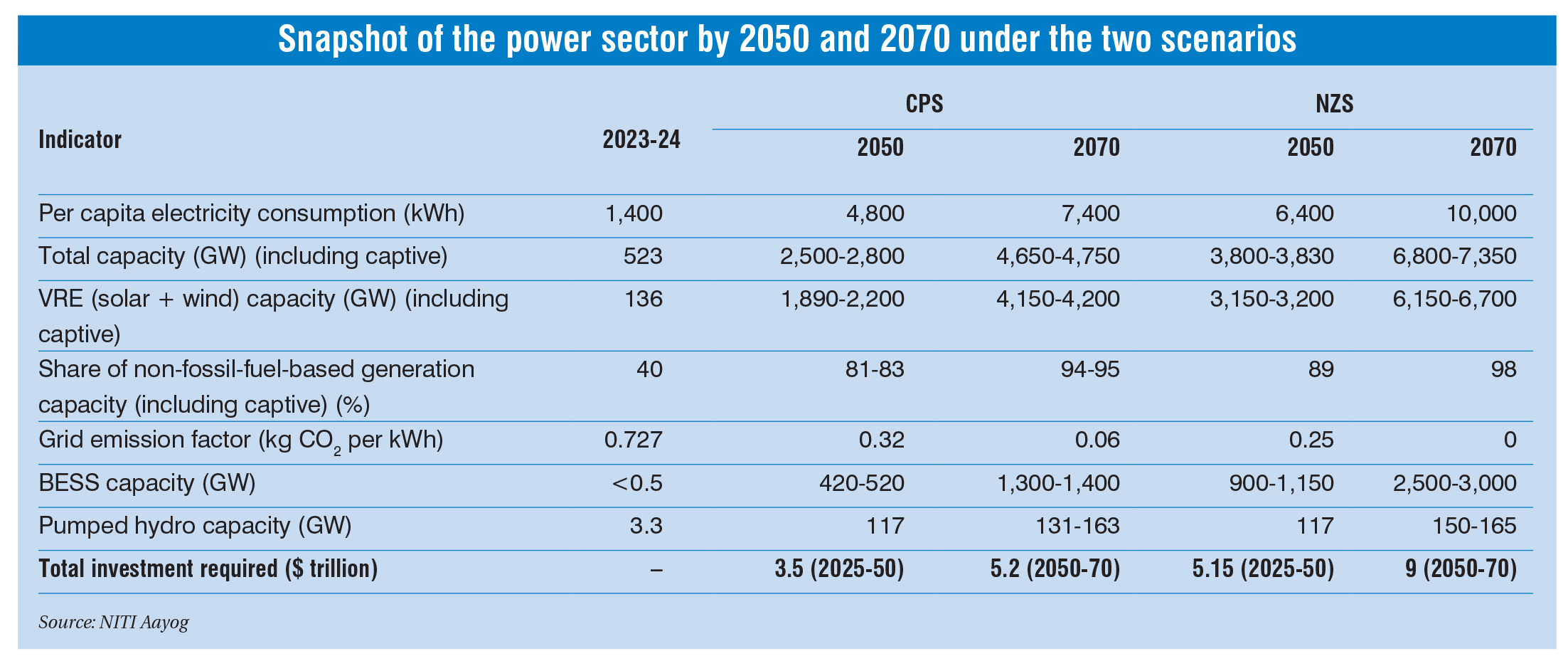

Electrification-led demand surge: Under both scenarios, rapid electrification across end-use sectors drives the transition. The share of electricity in the final energy consumption is projected to rise from about 21 per cent in 2025 to nearly 40 per cent under CPS and 60 per cent under NZS by 2070. This increase is supported by electric mobility, industrial electrification, green hydrogen production and rising cooling demand. As a result, the per capita electricity consumption rises significantly, reaching around 4,800 kWh under CPS and 6,400 kWh under NZS by 2050, and further increasing to approximately 7,400 kWh and 10,000 kWh, respectively, by 2070.

Capacity expansion and generation mix: To meet the rising demand, the total installed capacity is projected to increase from 535 GW in 2024-25 to about 4,650 GW-4,750 GW under CPS and 6,800 GW-7,350 GW under NZS by 2070. Across both pathways, a strong shift towards variable renewable energy (VRE) is anticipated, with the combined share of solar and wind capacity rising from 26 per cent in 2023-24 to around 88 per cent under CPS and 91 per cent under NZS.

In parallel, battery energy storage systems (BESSs) are projected to scale up from less than 50 GW in 2030 to about 1,300 GW-1,400 GW under CPS and 2,500 GW-3,000 GW under NZS by 2070. Pumped storage capacity is also expected to reach roughly 110 GW under CPS and 150 GW-165 GW under NZS by 2070. Coal is projected to continue to play a role in the near to medium term, particularly for grid stability. It is projected to peak earlier under NZS as long-duration storage and clean alternatives become more competitive. Nuclear capacity is projected to reach 87 GW-135 GW by 2070 under CPS. Under NZS, the 100 GW nuclear mission target is expected to be achieved by 2047, with capacity rising further to around 295 GW-320 GW by 2070. Additionally, natural gas will play a limited long-term role in both scenarios, with most existing plants likely to be phased out by 2050.

In terms of generation, electricity output increases substantially in both scenarios. By 2070, renewables are projected to account for more than 80 per cent of the total generation. The share of nuclear power rises to 13-14 per cent under NZS and 5-8 per cent under CPS, while coal’s contribution declines significantly. However, plant load factors during the intermediate period remain around 62-65 per cent, reflecting continued utilisation for grid stability.

Grid emission factor: These structural changes in the generation mix are to reduce carbon intensity significantly. The grid emission factor, estimated at 0.71 kg CO2 per kWh in 2025, declines to about 0.328 kg CO2 per kWh by 2050 under CPS. Under NZS, the emission intensity falls by a sharp 65 per cent over the same period, driven by accelerated renewables deployment, storage integration and phased coal retirements.

Resource footprint: The projected capacity expansion has land and water implications. Based on assumed land requirements per MW and the projected capacity mix, land use is expected to increase steadily under both scenarios, reaching around 7.5 per cent of the national wasteland under CPS and 11 per cent under NZS by 2070. Water demand is projected to rise initially, before moderating as thermal generation declines. However, higher nuclear capacity and green hydrogen production under NZS may result in slightly higher water use compared to CPS.

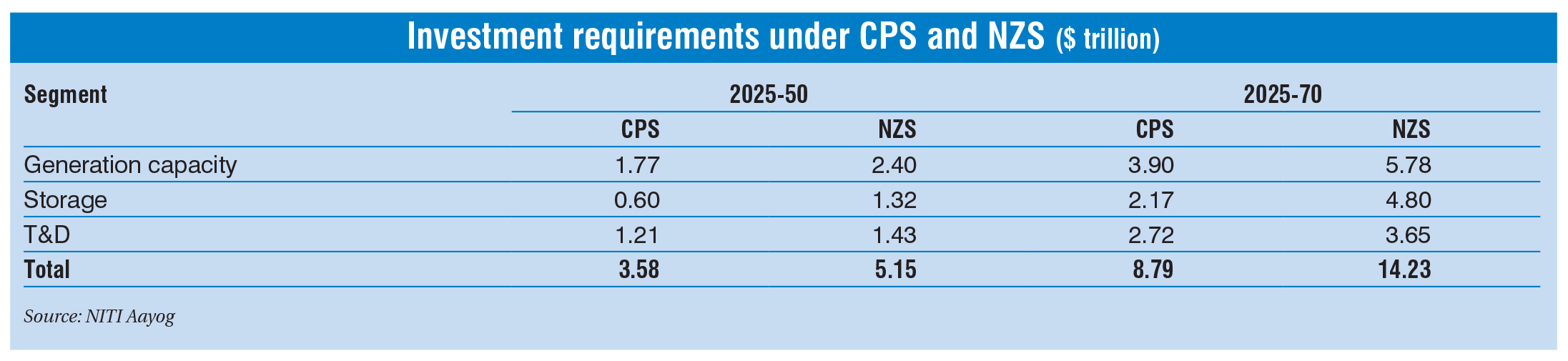

Investment requirement: Meeting the projected electricity demand requires substantial investment in generation, storage and transmission and distribution (T&D) infrastructure. The total investment is estimated at approximately $8.79 trillion under CPS, with 69 per cent allocated to capacity expansion (generation and storage) and 31 per cent to T&D. Under NZS, investment requirements increase to about $14.23 trillion, with 74 per cent directed towards capacity addition (generation and storage) and 26 per cent towards transmission, reflecting faster renewable deployment, large-scale storage integration, extensive electrification and grid modernisation.

Challenges and opportunities

Challenges and opportunities

As India advances towards a clean energy transition, the power sector faces interconnected technical, financial, regulatory and institutional challenges across the entire value chain.

In the near to medium term, coal will remain essential for maintaining system stability. However, coal plants based on ultra-supercritical and advanced ultra-supercritical coal plants entail high upfront capital costs. Over time, there is also a risk of assets becoming stranded, if newly built coal plants become underutilised before the end of their economic life. The growth of variable renewable energy also intensifies the need for supply-demand balancing. Today, coal and hydro plants largely provide this flexibility, but as coal’s share declines, scalable energy storage solutions such as pumped hydro and BESSs will become increasingly critical. Currently, these storage solutions exist far below the scale required for reliable grid operation.

T&D infrastructure is another key enabler of renewable integration. Existing systems can accommodate only limited renewable growth, beyond which substantial upgrades are needed. A major opportunity here is distributed generation such as rooftop solar, which reduces land constraints, lowers transmission losses and enables consumers to generate power closer to where it is consumed. Initiatives such as the green energy corridor scheme are also strengthening interstate and intra-state transmission lines to evacuate renewable energy. However, distribution upgrades such as smart meters and advanced monitoring remain slower due to high aggregate technical and commercial losses, which continue to strain discom finances and limit investment in modernisation.

Domestic manufacturing capacity also lags behind projected demand, with solar cells, modules, wind components, electrolysers and batteries insufficiently supplied. Research and development spending also remains modest, especially in the private sector, creating dependence on imported technologies for advanced storage, AI-enabled grids and green hydrogen. To promote local manufacturing, the government has rolled out measures such as the production-linked incentive scheme. The government also notified the Battery Waste Management Rules, 2022, to promote the recycling of solar panels and batteries. Recycling enterprises are also emerging, with several firms establishing facilities to recover materials such as silver, copper and silicon from end-of-life solar modules, helping reduce dependence on critical mineral imports.

Financing is another major bottleneck. Clean energy projects are capital-intensive and require large upfront investment. Borrowing costs in India remain high and projects reliant on imported equipment face foreign exchange risks. While instruments such as green bonds and sustainability-linked loans are attracting investor interest, the financing ecosystem must de-risk emerging technologies. Finally, policy and regulatory challenges influence the pace and stability of the transition. India has provided strong central policy direction, but implementation varies across states. Furthermore, fragmented regulatory responsibilities across institutions such as the Central Electricity Regulatory Commission, the Bureau of Energy Efficiency and state commissions also lead to overlapping mandates. As such, greater harmonisation, strong enforcement and long-term policy stability will be critical for maintaining investor confidence, while ensuring smooth sectoral transformation.

Financing is another major bottleneck. Clean energy projects are capital-intensive and require large upfront investment. Borrowing costs in India remain high and projects reliant on imported equipment face foreign exchange risks. While instruments such as green bonds and sustainability-linked loans are attracting investor interest, the financing ecosystem must de-risk emerging technologies. Finally, policy and regulatory challenges influence the pace and stability of the transition. India has provided strong central policy direction, but implementation varies across states. Furthermore, fragmented regulatory responsibilities across institutions such as the Central Electricity Regulatory Commission, the Bureau of Energy Efficiency and state commissions also lead to overlapping mandates. As such, greater harmonisation, strong enforcement and long-term policy stability will be critical for maintaining investor confidence, while ensuring smooth sectoral transformation.

Policy suggestions

To achieve the net zero target by 2070, the report proposes coordinated policy, technological and infrastructure measures across the power sector. Nuclear power is identified as a key pillar of deep decarbonisation, particularly for industrial users and large captive consumers. Replacing coal-based captive plants with small modular reactors can reduce emissions, while maintaining energy security. Scaling this transition will require the implementation of the SHANTI Act, with a target of expanding nuclear capacity to 100 GW by 2047 and 200 GW-300 GW by 2070. This must also be supported by dedicated budgetary allocations and access to green bond financing to improve project bankability.

At the same time, accelerated deployment of co-located solar-wind hybrid projects with integrated storage can improve land-use efficiency, reduce curtailment and ease transmission congestion. This will require early identification of high-potential hybrid zones, streamlined land aggregation and single-window clearances. In parallel, inefficient thermal plants, particularly those over 25 years old, should be retired in a phased manner and repurposed as clean energy hubs to utilise the existing infrastructure.

Further, distributed energy resources, especially decentralised solar, are critical for reducing transmission losses, easing land pressures and enhancing system resilience. Land-neutral solutions such as agrivoltaics, floating solar and rooftop systems should be supported through targeted viability gap funding (VGF). Moreover, as rooftop solar and behind-the-meter storage expand, peer-to-peer trading can enable local balancing and reduce stress on the grid. Additional VGF support is also required to scale emerging storage technologies, including pumped storage and hydrogen-based systems. These efforts should be complemented by market-based incentives such as time-of-day tariffs, ancillary services markets and capacity remuneration mechanisms.

Additionally, with rising renewable capacity, transmission expansion must be fast-tracked to align with the commissioning timelines of upcoming projects. To minimise delays, land acquisition must be streamlined through coordinated planning between central and state governments, identification and pre-approval of suitable land parcels, digitalisation of land records and setting up of single-window clearance mechanisms. Alongside, grid modernisation through real-time monitoring systems, automation of substations and centralised control via supervisory control and data acquisition systems will further strengthen efficiency. Advanced digital tools leveraging AI and machine learning must also be utilised to strengthen demand and generation forecasting.

On the distribution side, improving the financial health of discoms remains essential. The report recommends a one-time debt restructuring package, with central support linked to the implementation of credible structural reforms. Gradual tariff rationalisation towards cost-reflective levels as well as monetisation of non-core assets, such as leasing surplus land, can further improve financial sustainability. Finally, strengthening domestic manufacturing value chains, fostering a robust research and development ecosystem, and leveraging concessional and blended climate finance will be necessary to mobilise large-scale investment in low-carbon power infrastructure.

Conclusion

Over the past two decades, India’s power sector has undergone significant structural changes, characterised by universal household electrification, expansion of the national grid and rapid growth in renewable energy capacity. Looking ahead, electricity demand is projected to increase sharply, driven by urbanisation, industrial growth and deeper electrification across sectors. Meeting this demand while reducing emissions will require a continued shift towards renewables, supported by large-scale storage deployment, timely transmission expansion and appropriate market reforms. In the near to medium term, coal will remain important for grid stability, while nuclear power is expected to assume a larger role over the long term. At the same time, reforms in the distribution segment, focused on financial sustainability and operational efficiency, will be critical to managing the transition.