India’s power sector is undergoing a rapid transformation, driven by rising electricity demand, economic growth and a shift towards cleaner energy sources. In this landscape, balancing sustainability with reliable and affordable power supply has become a key policy priority.

Accordingly, the Central Electricity Authority (CEA) has released the National Generation Adequacy Plan for 2026-27 to 2035-36 as a strategic framework for long-term capacity planning. The study evaluates the generation capacity required to meet the projected demand over the next decade while ensuring cost efficiency and system reliability.

Study methodology

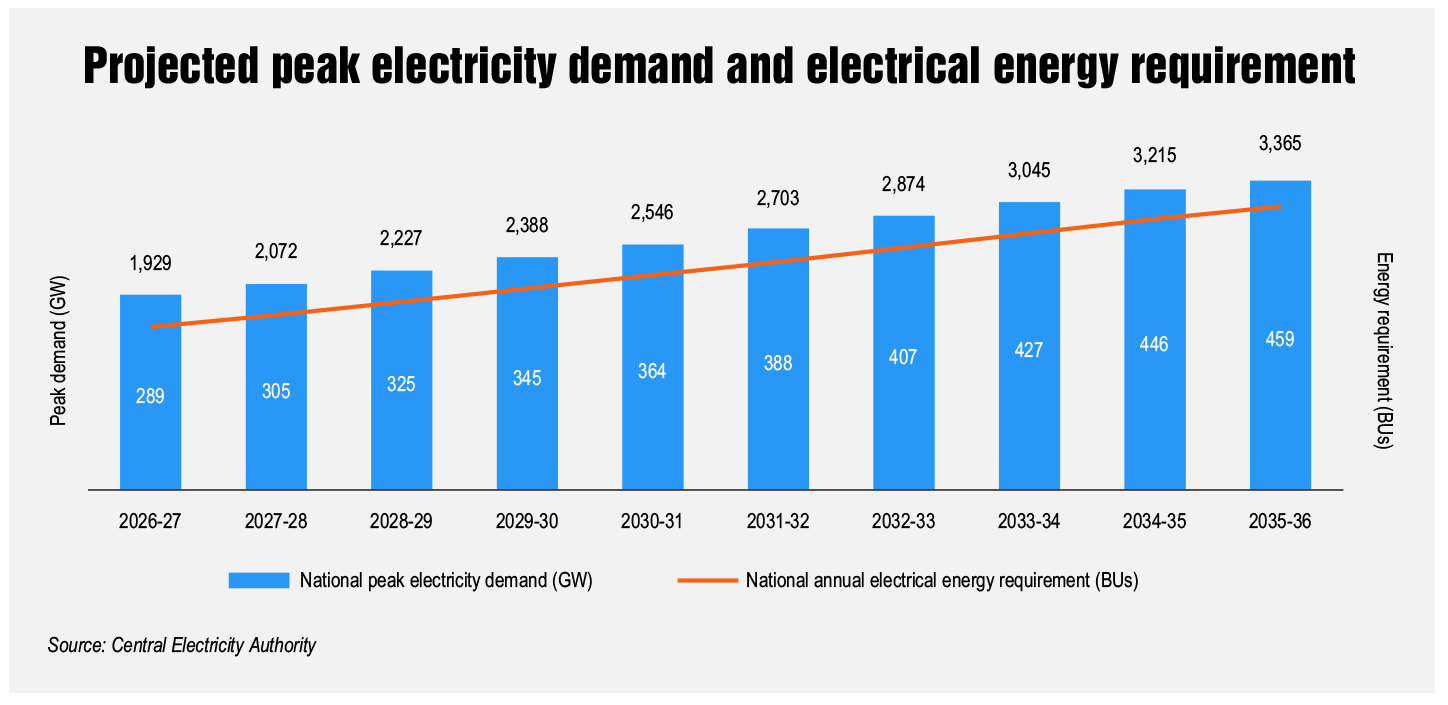

The study begins with a detailed analysis of electricity demand patterns, including temporal variations, demand complementarity across states and generation despatch trends based on recent operational data. A key input in the study is the projection of future electricity demand. The demand projections, as per the mid-term review of the 20th Electric Power Survey (EPS) by the CEA, indicate that peak electricity demand will grow at a compound annual growth rate (CAGR) of 5.58 per cent between 2024-25 and 2035-36, while the total energy requirement is expected to grow at a CAGR of 6.41 per cent. By 2035-36, peak demand is projected to reach 459 GW, with total energy requirement rising to 3,365 BUs. These projections account for emerging demand drivers such as electric vehicles and India’s target of 5 million metric tonnes of green hydrogen production by 2030.

Further, the study evaluates the existing installed capacity and recent additions. In addition, existing, under-construction and planned capacity is treated as firm input to ensure realistic planning. The analysis also considers the contribution of various sources during peak demand periods based on actual hourly generation data for 2024-25. These inputs are used in generation expansion planning models to determine the most cost-effective capacity mix.

Projected generation mix

To meet the growing electricity demand, India’s installed power generation capacity is projected to expand significantly from around 520 GW (as of January 2026) to approximately 1,121 GW by 2035-36. The expansion pathway is based on a least-cost planning approach that minimises both investment and operational costs while ensuring that technical constraints of different generation technologies are met. The plan is also aligned with national policy goals, including the target of achieving 500 GW of non-fossil-fuel-based capacity by 2030.

Over the planning horizon, a significant structural shift in installed capacity is observed. Solar power is expected to witness the most substantial growth, increasing from around 141 GW in 2025-26 (as on January 31, 2026) to approximately 509 GW by 2035-36. This makes solar the largest contributor to installed capacity, accounting for nearly 45 per cent of the total. The expansion is driven by its cost competitiveness and scalability, with annual additions estimated at around 30-40 GW over the next decade (excluding rooftop solar installations).

Over the planning horizon, a significant structural shift in installed capacity is observed. Solar power is expected to witness the most substantial growth, increasing from around 141 GW in 2025-26 (as on January 31, 2026) to approximately 509 GW by 2035-36. This makes solar the largest contributor to installed capacity, accounting for nearly 45 per cent of the total. The expansion is driven by its cost competitiveness and scalability, with annual additions estimated at around 30-40 GW over the next decade (excluding rooftop solar installations).

Wind capacity is projected to increase from about 55 GW to around 155 GW, contributing roughly 14 per cent to total capacity. Large hydro is expected to grow from about 51 GW to nearly 78 GW, providing an important source of flexible and peak-support power. Nuclear capacity is also projected to expand from around 8.8 GW to about 22 GW by 2035-36, with a longer-term vision of reaching 100 GW by 2047 to support clean and firm power requirements. Other sources contribute relatively smaller shares, including around 20 GW of gas-based capacity, 16 GW of biomass and 6 GW of small hydro.

Notably, despite the strong push towards renewables, coal remains a critical component of the energy mix. Its installed capacity is projected to reach about 315 GW, or 28 per cent of the total capacity by 2035-36, making it the second largest source after solar. Overall, non-fossil-fuel-based capacity is expected to increase sharply from around 272 GW in 2025-26 (as on January 31, 2026) to around 786 GW by 2035-36. As a result, its share in total installed capacity will rise from about 52 per cent to nearly 70 per cent. In contrast, fossil-fuel-based capacity will grow modestly from around 248 GW to about 335 GW, leading to a decline in its share from 48 per cent to 30 per cent.

A similar trend can be observed in total electricity generation. The share of fossil-fuel-based generation is projected to decline from about 66 per cent in 2026-27 to around 51 per cent by 2035-36, while non-fossil generation increases from about 34 per cent to nearly 49 per cent. This indicates a gradual transition towards cleaner energy sources, while still maintaining a balanced mix to ensure system stability.

Storage requirements

Storage requirements

With rising renewable energy penetration, energy storage is emerging as a key enabler for grid stability and flexibility. The plan projects total energy storage requirements of 174 GW, comprising 80 GW of battery energy storage systems (BESS) and 94 GW of pumped storage plants (PSPs) by 2035-36. In line with the growing requirements of energy storage, the government has introduced several measures to accelerate deployment. These include 100 per cent waiver of interstate transmission system charges for PSPs awarded before June 30, 2028, as well as for co-located BESS projects commissioned by the same date; viability gap funding for the development of 43,000 MWh of BESS capacity; and streamlined environmental clearances for off-stream PSPs.

Challenges

A key challenge in India’s energy transition is its heavy reliance on imports for battery technologies. Currently, around 75-80 per cent of lithium-ion cells, constituting nearly 80 per cent of BESS costs, are imported, with global manufacturing concentrated in a few countries. This exposes India to supply chain risks, geopolitical uncertainties and price volatility. Similarly, critical minerals such as lithium, cobalt, nickel and graphite are largely imported due to limited domestic reserves and processing capacity, further increasing vulnerability.

Another concern is uncertainty in demand projections. The EPS review also presents an alternative low-growth scenario that accounts for recent trends of slower demand growth. Under this scenario, base case demand projections are shifted by one year across the entire study horizon, highlighting the risk of over-or under-investment in capacity planning. To ensure reliable supply, a planning reserve margin of 13-14 per cent has been ensured, providing a buffer against demand fluctuations, renewable variability and unexpected outages.

Conclusion and recommendations

India’s power sector is entering a critical phase, where rising electricity demand must be aligned with long-term decarbonisation goals. This transition will be driven by a sharp expansion of non-fossil capacity by 2035-36. Even so, coal will continue to play a crucial role as a flexible backbone for grid stability. At the same time, nuclear power is being scaled up under the Nuclear Energy Mission. A key focus area is the development of small modular reactors, with a target to operationalise at least five indigenously developed units by 2033.

As renewable penetration rises, energy storage will become indispensable. Recognising this, the CEA recently outlined a road map targeting nearly 100 GW of PSP capacity by 2035-36, supported by faster clearances, promotion of off-stream projects, budgetary support and private sector participation.

In parallel, strengthening transmission infrastructure, deploying smart grid technologies and enhancing forecasting capabilities will be essential to maintain grid stability. Importantly, given the evolving demand and technology trends, the plan will be reviewed annually to ensure a balanced approach to growth, reliability and sustainability.