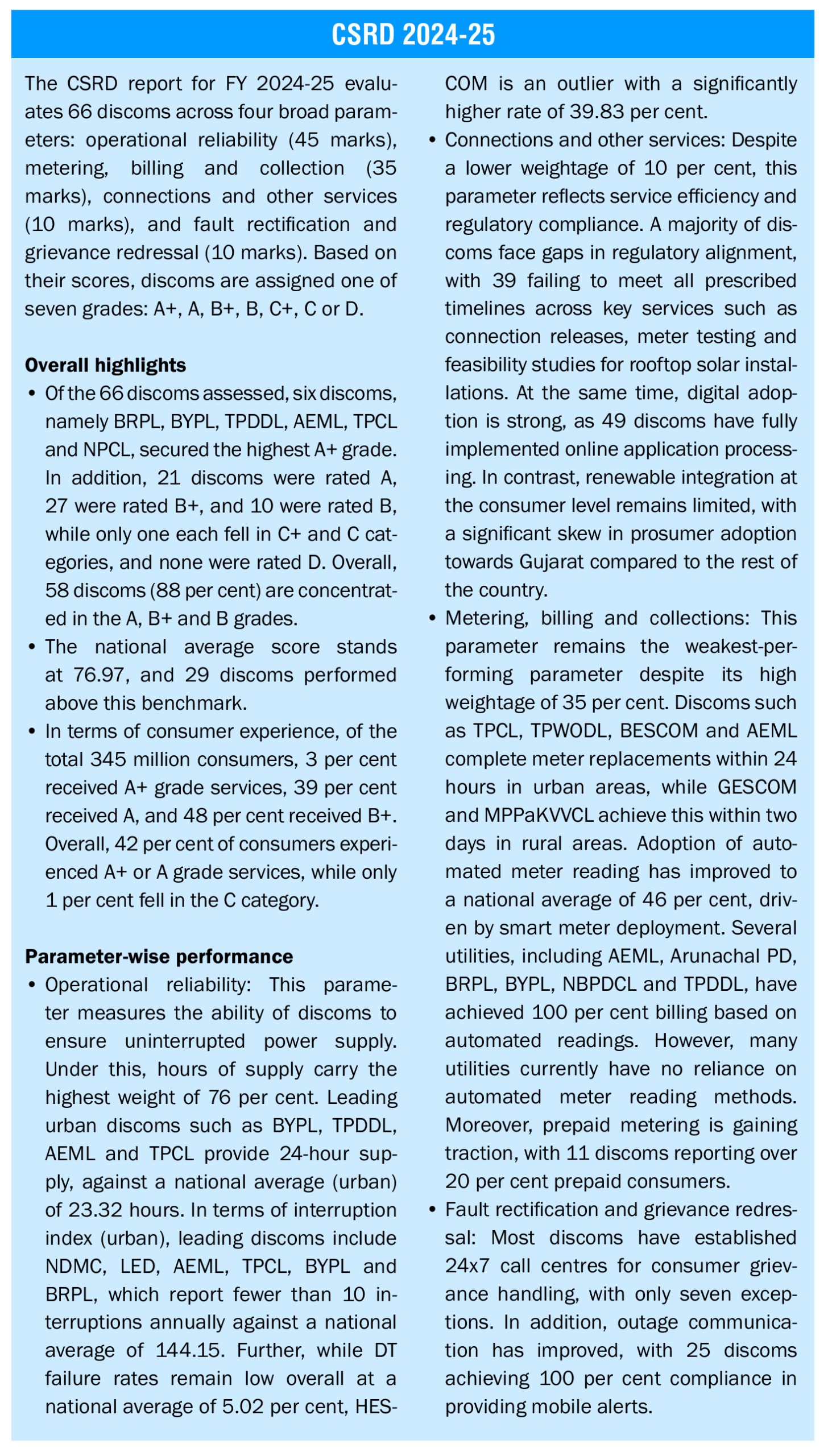

Over the past few decades, the government has introduced targeted measures to strengthen the performance of discoms, including investments in network augmentation, smart metering, automation and digital systems. A key milestone was achieved in 2024-25, when discoms reported their first-ever all-India profit after tax of Rs 27.01 billion, marking a historic turnaround from a loss of Rs 270.22 billion in 2023-24.

To assess sectoral progress and benchmark discom performance, the Ministry of Power has released two key reports: the fifth edition of the Consumer Service Rating of Discoms (CSRD) for 2024-25 and the second edition of the Distribution Utilities Ranking (DUR) for 2024-25. These reports provide a data-driven evaluation of utilities across critical performance and service parameters, helping identify gaps, promote best practices, and support more informed decision-making among utilities and policymakers.

Highlights of DUR 2024-25

The DUR 2024-25 evaluates utilities through a multi-dimensional framework covering institutional capability, financial sustainability, operational efficiency and service delivery outcomes. The rankings are derived from a weighted score based on six parameters. These include the established Annual Integrated Rating and Ranking (IR) and CSRD frameworks, each carrying a weightage of 35 per cent. Additionally, the ranking considers renewable purchase obligation (RPO) achievement (5 per cent), penetration of communicable system metering (CSM) (5 per cent), enablement of demand-side response (DSR) (5 per cent), and adherence to the resource adequacy (RA) framework (15 per cent).

A total of 66 utilities participated in the 2024-25 assessment. In this period again, the top three performers were Adani Electricity Mumbai Limited (AEML), Tata Power-Delhi Distribution Limited (TPDDL) and Noida Power Company Limited (NPCL), retaining their positions from the previous year.

To ensure a more meaningful comparison, the utilities are grouped into three categories: 41 discoms (except urban and special category states), 15 special category state utilities, and 10 urban utilities.

Among the overall top 10 utilities, urban utilities dominated with seven entries, while one was a special category state utility and two were from the broader distribution category. Notably, 7 of the 10 urban utilities featured in the overall top 10 list.

Discoms (except urban and special category state utilities)

Discoms (except urban and special category state utilities)

Out of 41 utilities in this category, 8 scored in the 75-100 range, 32 in the 40-75 range, and only 1 scored below 40. Gujarat’s Dakshin Gujarat Vij Company Limited emerged as the top-performing utility in this category and the highest-ranked public discom overall, with a score of 84.6. This was driven by high scores in IR (97.9), CSRD (82.1), and a perfect score in CSM. On the other hand, Jharkhand Bijli Vitran Nigam Limited ranked last both category-wise and overall, with a score of 30.

Odisha’s TP Northern Odisha Distribution Limited (TPNODL) and TP Central Odisha Distribution Limited secured ranks 2 and 4 respectively, driven by strong performance in IR and CSRD. However, weak scores in RPO compliance and CSM indicate gaps in renewable procurement and metering infrastructure.

Goa Power Department (PD) ranked 3rd in the category and 11th overall, reflecting consistent performance across parameters. However, its low DSR score (19) highlights the need to accelerate the implementation of time-of-day tariffs and associated metering.

Bihar’s North Bihar Power Distribution Company Limited secured the 5th position despite scoring zero in RPO, supported by strong performance in IR, CSRD, DSR and RA.

Haryana’s Dakshin Haryana Bijli Vitran Nigam Limited and Uttar Haryana Bijli Vitran Nigam Limited achieved perfect scores in both RPO and RA, enabling them to secure the 6th and 8th ranks respectively. However, weak DSR performance remains a key constraint.

At a parameter level, performance gaps are evident. Only eight utilities scored above 75 in RPO compliance and just seven in CSM, pointing to limited progress in renewable integration and feeder/distribution transformer (DT) metering. DSR remains the weakest area, with no utility achieving full marks and only six scoring above 75, reflecting limited adoption of time-of-day tariffs and enabling infrastructure.

In contrast, RA shows relatively stronger performance, with 21 utilities scoring above 75, indicating better alignment with planning and regulatory requirements compared to operational reforms.

The bottom 10 utilities recorded low scores due to weak performance across multiple parameters.

Notably, there is significant intra-state variation in states such as Gujarat, Karnataka, Madhya Pradesh, Odisha and Uttar Pradesh, highlighting uneven implementation of reforms despite operating under a common policy framework.

Special category state utilities

Out of 15 utilities in this category, only Assam Power Distribution Company Limited (APDCL) scored in the 75-100 range, securing both the top category rank and an overall rank of 7. Its strong performance was driven by high scores across IR (81), CSRD (82.8), RA (98.4) and a perfect score in CSM. In contrast, 11 utilities fell in the 40-75 range, while 3 scored below 40. Lakshadweep Electricity Department (LED) was the worst-performing utility both category-wise and second worst overall, with a score of 32.6.

APDCL, Meghalaya Power Distribution Corporation Limited (MePDCL) and Uttarakhand Power Corporation Limited (UPCL) were the only utilities to achieve full scores in any parameter. However, both MePDCL and UPCL recorded very low scores in CSM (25 each) and DSR (4.5 each), highlighting uneven performance across parameters.

Jammu & Kashmir’s Kashmir Power Distribution Corporation Limited and Jammu Power Distribution Corporation Limited ranked among the bottom four both category-wise and overall, primarily due to weak DSR performance. Their non-participation in the IR assessment, along with LED, further pulled down their overall scores.

LED and Andaman & Nicobar PD underperformed across nearly all parameters, including zero scores in CSM, indicating an urgent need for operational reforms.

CSM performance remains a key concern across the category. Except for APDCL and Manipur State Power Distribution Company Limited, all utilities scored poorly, reflecting gaps in feeder and distribution transformer metering with automated remote reading. Notably, Nagaland PD, Arunachal PD, Andaman & Nicobar PD and LED scored zero in this parameter.

Similarly, DSR performance is weak across the board, with Ladakh PDD (77.2) being the only utility to achieve a relatively strong score.

Urban utilities

Urban utilities

Urban utilities demonstrate relatively strong performance compared to other categories. Of the 10 utilities, 7 scored in the 75-100 range and the remaining 3 in the 40-75 range, with none scoring below 40. AEML emerged as the top-performing utility both category-wise and overall, with a score of 92.5.

In contrast, Uttar Pradesh’s Kanpur Electricity Supply Company Limited (KESCO) ranked lowest with a score of 57.2, although this remains higher than the lowest scores in the other categories.

AEML, TPDDL and NPCL topped the rankings, with scores of 92.5, 87.6 and 86.7 respectively. AEML maintained consistently strong performance across parameters, scoring above 75 in all except DSR (58), indicating some scope for improvement. In general, DSR remains a weak area for urban utilities, with only Brihanmumbai Electric Supply and Transport, BSES Rajdhani Power Limited and Tata Power Company Limited (TPCL) scoring above 75.

Maharashtra’s TPCL performed strongly across parameters, scoring above 75 in all and achieving perfect scores in CSM and RA. However, its non-participation in IR pulled it down from a category rank of 9 to an overall rank of 40.

In terms of CSM, AEML, KESCO, Kerala’s Thrissur Corporation Electricity Department (TCED) and TPCL led the category with perfect scores, reflecting full deployment of metering infrastructure with automatic remote reading capabilities.

Despite strong overall performance, RPO compliance remains a persistent weakness across urban utilities. Even top performers recorded low scores, with KESCO scoring zero in this

parameter.

Additionally, KESCO’s poor performance in RPO (0) and DSR (5.4) dragged it to an overall rank of 45, despite strong scores in CSM and CSRD.

Conclusion

Overall, the reports highlight a clear performance gap across utility segments, with urban utilities performing relatively well, while special category state utilities and other discoms lag behind. Across most utilities, DSR, RPO compliance and system metering remain weak. In contrast, RA and digital initiatives, including online consumer services and automated meter reading, show relatively better performance. In the case of some utilities, non-participation in assessments like IR has also affected overall rankings. Further, considerable variation within states suggests that the issue lies more in uneven implementation than in policy design. Importantly, utilities that perform well across multiple parameters tend to lead, while those strong in only a few areas rank lower, underscoring the need for more balanced and consistent improvement going forward.