Being the last leg in the electricity supply chain, the power distribution sector plays a critical role in determining the overall health of the power sector. Since the performance of distribution utilities ultimately affects the sustainability of the entire value chain, the segment has remained at the centre of power sector reforms. For decades, however, the sector has struggled with challenges such as high aggregate technical and commercial (AT&C) losses, tariff distortions and delays in subsidy disbursements. Meanwhile, the evolving energy landscape, marked by rising electricity demand, greater renewable energy integration and the electrification of end-use sectors, is reshaping the role of distribution utilities. In response, policy efforts have increasingly focused on improving cost recovery, enhancing operational efficiency and strengthening accountability. At the same time, distribution utilities are adopting advanced technologies to build smarter, more efficient and resilient networks.

State of the sector

State of the sector

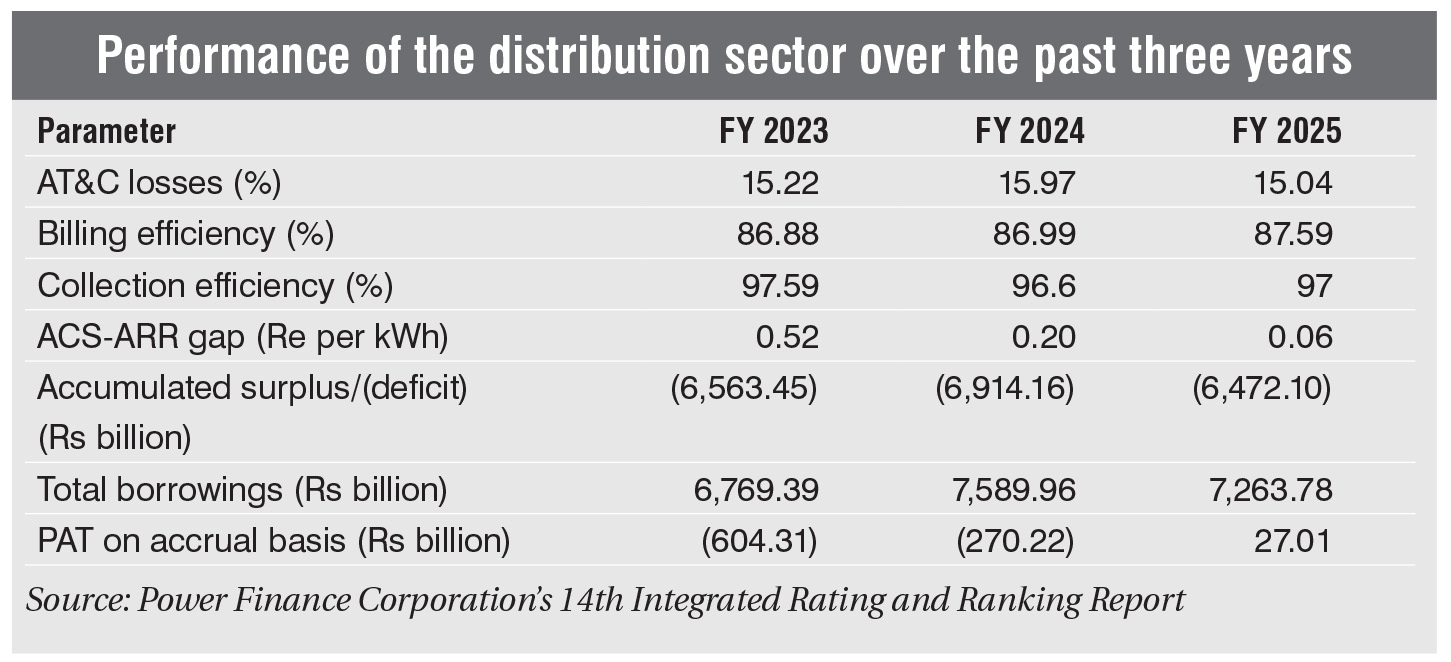

The distribution sector reached an important milestone in 2024-25. For the first time since the unbundling and corporatisation of the state electricity boards, distribution utilities collectively reported a positive profit after tax (PAT) of Rs 27.01 billion on an accrual basis at the all-India level, compared to a loss of Rs 270.22 billion in 2023-24.

This turnaround has been driven by a series of government interventions, particularly the Revamped Distribution Sector Scheme (RDSS). Notably, the budget estimate for the RDSS has been increased to Rs 180 billion for FY 2027 compared to the revised estimate of Rs 156.71 billion for FY 2026. Continued support remains critical as discoms still face significant financial stress. At the end of FY 2025, their accumulated losses stood at Rs 6.47 trillion, while total borrowings were Rs 7.26 trillion.

Alongside improvements in profitability, key operational indicators also improved during the year. AT&C losses declined from 15.97 per cent in 2023-24 to 15.04 per cent in 2024-25. The average cost of supply-average revenue realised (ACS-ARR) gap also narrowed from Re 0.51 per kWh in 2022-23 to Re 0.20 per kWh in 2023-24 and further to Re 0.06 in 2024-25, indicating better cost recovery. Revenue realisation also improved during the year. Billing efficiency increased from 86.99 per cent to 87.59 per cent, and collection efficiency improved from 96.6 per cent to 97 per cent. Notably, 17 utilities achieved 100 per cent collection efficiency in 2024-25.

Further, the Electricity (Late Payment Surcharge) Rules, 2022 have improved payment discipline across the sector. Outstanding dues to gencos have declined from Rs 1,399.47 billion as of June 2022 to Rs 33.3 billion as of March 2026. Consequently, the average payment cycle of utilities has reduced from 132 days in 2023-24 to 113 days in 2024-25.

Meanwhile, the average daily power supply in FY 2025 increased to 22.6 hours in rural areas and 23.32 hours in urban areas. As per the Consumer Service Rating of Discoms Report 2024-25, the number of discoms in the top categories (A+, A and B+) nearly doubled in 2024-25 compared to 2022-23.

Policy measures

Policy measures

The government has introduced several measures to improve the financial and operational performance of utilities. The flagship initiative remains the RDSS, which focuses on smart metering and loss reduction. During the period FY 2022-FY2026 (up to February 9, 2026), Rs 457.36 billion had been allocated under the scheme, of which Rs 396.51 billion (87 per cent) has been utilised. Notably, fund utilisation reached 100 per cent in 2024-25. The scheme is expected to be extended up to FY 2028 to facilitate the completion of approved works.

In January 2026, the draft National Electricity Plan 2026 was notified, which outlines the roadmap for improving the sustainability of the distribution sector. The plan focuses on tariff rationalisation, power procurement optimisation and AT&C loss reduction. It also proposes wider deployment of prepaid smart meters, time-bound energy audits, robust accounting systems and network modernisation through geographic information system (GIS)-based asset mapping and automation.

Further, the draft Electricity (Amendment) Bill, released in October 2025, proposes the sharing of distribution networks to promote efficiency and competition. It seeks to enable the timely implementation of cost-reflective tariffs through greater regulatory oversight.

To improve financial sustainability, automatic monthly fuel and power purchase cost adjustment mechanisms have also been introduced. According to the Ministry of Power’s (MoP) Key Regulatory Parameters of Power Utilities Report, as of March 2026, regulators in 32 states and union territories have allowed automatic adjustment of these costs. Alongside this, timely subsidy payments by state governments and clearance of electricity dues by government departments are mandatory for states to avail of an additional borrowing space of 0.5 per cent of gross state domestic product.

Meanwhile, the Electricity Distribution (Accounts and Additional Disclosure) Rules, 2025 have introduced uniform accounting practices and enhanced transparency across utilities. In addition, the Electricity (Rights of Consumers) Rules, 2020 mandate 24×7 power supply for all consumers across urban and rural areas.

Loss reduction and smart metering

Under the RDSS, utilities are undertaking a range of loss reduction measures, including the replacement of old conductors, augmentation of substations and distribution transformers (DTs), segregation of feeders, and deployment of supervisory control and data acquisition and distribution management systems for real-time monitoring. As of June 25, 2026, the overall physical progress for loss reduction works under the RDSS is at 41.99 per cent.

Alongside network strengthening, a key area of intervention under the RDSS is the deployment of smart consumer meters, feeder meters and DT meters. Smart meters support automatic energy accounting, improved load forecasting, demand-side management and data-driven utility operations.

According to the RDSS portal, as of June 25, 2026, 53.04 million smart consumer meters have been installed and are communicating against a sanctioned target of 195.82 million. Maharashtra, Uttar Pradesh, Assam, Gujarat and Chhattisgarh have recorded the highest number of communicating smart meters so far. Progress in DT metering has lagged, with 1.75 million DT meters installed and communicating against a sanctioned target of 5.25 million. In contrast, 165,249 feeder meters have been installed and are communicating against a sanctioned target of 195,952.

Technology adoption

The distribution sector is undergoing rapid digitalisation to improve network visibility, asset management and operational efficiency. A key focus area is network operations and maintenance. Artificial intelligence (AI)-enabled predictive maintenance, internet of things (IoT) sensors, cloud-based dashboards and advanced analytics are improving asset health monitoring and risk management. At the same time, utilities are using AI for fault detection, load forecasting, transformer condition monitoring and theft analytics. IoT-enabled sensors and digital monitoring systems are increasingly being deployed to track asset condition and electrical parameters in real time. This enables faster restoration, better scheduling and lower technical losses.

For cables and conductors, digital asset registers and GIS-based network models are being integrated with outage and inspection data to identify ageing assets, bottlenecks and recurring fault locations. In addition, thermography and drone-based inspections are helping utilities detect hotspots, loose joints and sagging conductors at an early stage. Meanwhile, substations are evolving into intelligent and remotely operated facilities through fibre-based communication networks, digital protection systems and process bus technologies. Another technology beginning to gain traction is digital twin technology. It is already being used by discoms such as BSES Rajdhani Power Limited and Jaipur Vidyut Vitran Nigam Limited. Digital twins enable utilities to simulate network behaviour under different demand and operating conditions. This can improve network expansion and power procurement planning.

Further, the MoP has initiated the development of the India Energy Stack (IES), a digital public infrastructure aimed at enabling interoperable data exchange and addressing fragmented utility systems. Pilot projects are planned across utilities in Delhi, Gujarat, Andhra Pradesh, Uttar Pradesh and Mumbai during 2026-27. For this initiative, Rs 513 million has been allocated, of which Rs 38.8 million has been released so far.

Sectoral challenges

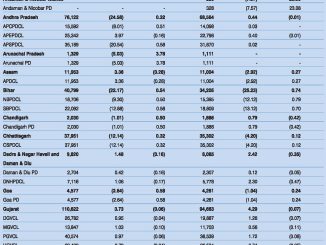

The distribution segment continues to face several financial and operational challenges. High AT&C losses, delayed subsidy payments and lack of cost-reflective tariffs due to regulatory disallowances continue to put pressure on utility finances. As of March 31, 2026, Meghalaya recorded the highest disallowances at about 59 per cent of the net annual revenue requirement, followed by Jammu & Kashmir (52 per cent), Andaman & Nicobar Islands (39 per cent) and Ladakh (27 per cent).

Tariff rationalisation also remains a work in progress. Based on 2026-27 tariff orders, only 15 states and union territories complied with the ±20 per cent cross-subsidy limit for low-tension industrial consumers, while only 13 complied in the high-tension industrial category, indicating continued deviation from cost-reflective tariffs.

In May 2026, the Central Electricity Authority (CEA) proposed a framework for rationalising consumer fixed charges and improving fixed cost recovery by discoms. According to the report, fixed costs, including transmission charges, employee salaries and infrastructure maintenance, account for 38-56 per cent of a utility’s annual revenue requirement. However, fixed charges contribute only 9-20 per cent of total revenue. To address this mismatch in fixed cost recovery, the CEA has proposed a gradual increase in the fixed charge component of retail tariffs over the next five years.

At the operational level, ageing infrastructure and inadequate network investments continue to strain distribution systems. Meanwhile, the rapid adoption of rooftop solar, electric vehicles and other distributed energy resources is making power flows bidirectional and demand patterns more uncertain, adding to network complexity. Utilities also continue to face issues related to power theft, billing inefficiencies, limited metering coverage and delays in adopting digital technologies. In addition, resistance to prepaid smart meters and delays in grant disbursement continue to affect sector performance.

The way forward

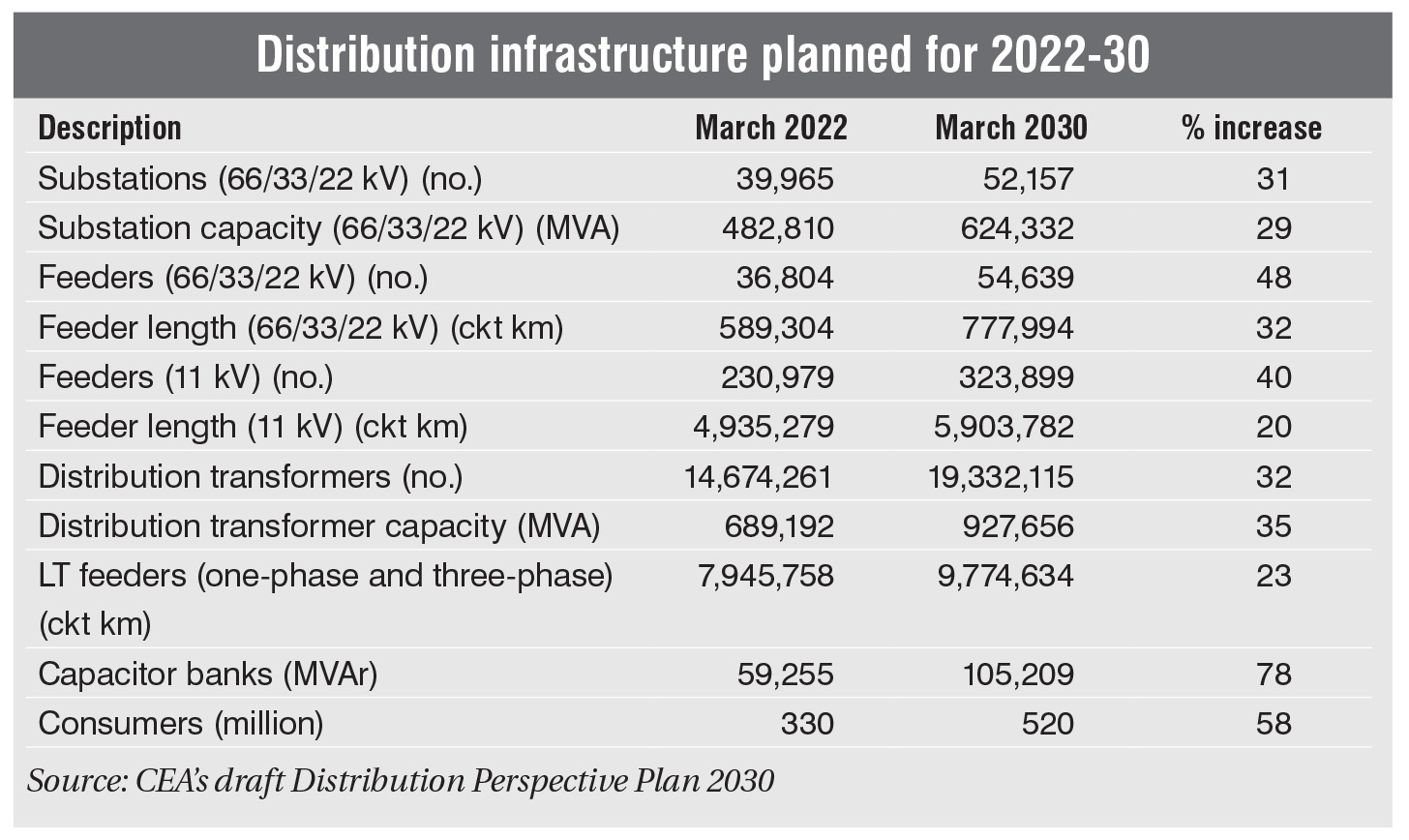

Addressing these issues will require substantial investment and targeted policy support. According to the CEA’s draft Distribution Perspective Plan 2030, about Rs 4.28 trillion will be required for distribution infrastructure upgrades during 2022-27. Of this, about Rs 1.89 trillion (44 per cent of the requirement) has been identified through the RDSS and other funding sources, indicating a significant investment gap.

In the coming years, reducing AT&C losses will remain the sector’s foremost priority. The sector aims to bring these losses down to single-digit levels in line with global benchmarks. Similarly, the ACS-ARR gap must turn negative to ensure the financial sustainability of discoms.

At the same time, utilities must make greater use of the vast volumes of data generated by smart meters. Leveraging this data for demand forecasting, consumer services, resource adequacy planning and power procurement optimisation can significantly improve operational efficiency. It is also essential for improving supply reliability, particularly as 27 discoms recorded DT failure rates at or above the national average of 5.02 per cent in 2024-25. Utilising this data will also require capacity building to equip utility personnel with the skills needed to harness it effectively. Meanwhile, greater adoption of AI and machine learning across utility operations is expected to improve demand forecasting, enhance grid visibility and strengthen decision-making. In addition, the India Energy Stack is expected to improve data flow across utility functions, provide better visibility of distributed energy resources and enable greater consumer participation.

As digitalisation deepens, demand-side programmes are also expected to gain momentum. Wider adoption of time-of-use tariffs can better align revenues with power procurement costs, encourage load shifting and reduce peak power purchase expenses. While some private discoms have already undertaken pilot projects, implementation across state-owned utilities remains at an early stage.

Importantly, another key priority for the sector is the development of more balanced risk-sharing mechanisms between generators and discoms. Traditionally, long-term power purchase agreements have placed most demand and price risks on discoms. However, with more mature electricity markets and increasing renewable energy integration, there is growing recognition that these risks should be more equitably shared to improve procurement efficiency and strengthen utility finances.

Overall, the sector has made measurable progress in improving its financial and operational performance. Sustaining these gains going forward will require timely tariff reforms, continued loss reduction, accelerated infrastructure modernisation and greater adoption of digital technologies across the sector.

Khushi Rohatgi