Can the revised environmental norms for thermal power plants be a catalyst for the growth of the equipment industry? Industry observers say the answer is yes.

The power equipment industry has been hit hard in the past few years on account of order inflows drying up, delays in project execution, margin pressures and an oversupply scenario. The average power project awards have been less than 9 GW, against the annual rate of 25-30 GW during the period 2007-10. As recently as 2015, there was little evidence to suggest that the slowdown in the industry could be reversed. But the outlook has since changed significantly. In end-2015, in order to comply with the Conference of the Parties (COP21) commitments, the environment ministry issued new norms to restrict the emissions of nitrogen oxide (NOx), sulphur dioxide (SO2) and particulate matter (PM) from thermal power plants (TPPs). Compliance with the norms by existing and upcoming projects would require significant equipment upgrades and a large number of emission control systems. This provides a huge business opportunity and stimulus for the equipment industry’s recovery, say observers.

“We see a total potential of 160-170 GW for the emission control market. We foresee significant business opportunities in segments such as flue gas desulphurisation (FGD) retrofitting, boiler modifications and retrofitting of electrostatic precipitators (ESPs), along with commercialisation of selective catalytic reduction (SCR)/selective non-catalytic reduction (SNCR) technology,” says Akhil Joshi, director, power, Bharat Heavy Electricals Limited (BHEL), India’s largest equipment company.

Since the announcement of the norms, the market has already begun to see a flurry of activity with tenders being issued by various utilities.

“Major players like NTPC are coming up with bulk tenders for FGD. We expect state utilities to follow on similar lines in the bulk ordering of FGD through domestic competitive bidding, allowing technology transfer,” says Shailendra Roy, chief executive officer (CEO) and managing director (MD) of private equipment major Larsen & Toubro (L&T) Power and whole-time director, L&T.

Further, steps being taken at the policy and regulatory level for the implementation of the new norms in recent months have boosted confidence in the industry. Key among these has been the release of a phased implementation plan by the Central Electricity Authority (CEA), as per which a region-wise implementation strategy to install FGD systems in about 122 GW of capacity by 2022 has been announced (72 GW of projects that do not have space to install FGDs will be phased out).

“While the plan was being structured, there have been tenders for the installation of FGD and consultancy tenders for carrying out the feasibility of installing air pollution control equipment. With the implementation plan in place, we can expect a lot of tenders with respect to FGD within the next three to four years,” says Dr Klaus Baernthaler, director, product and business development of Austria-headquartered private equipment player Andritz AG. Another confidence-building factor for the equipment industry has been the growing readiness of independent power producers (IPPs) to meet the new norms. Initial apprehensions about the two-year time frame for the implementation of norms being too aggressive have now reduced substantially.“The CEA has sought details of preparedness and action plans for meeting the revised norms from all TPPs. All IPPs are fully on board to implement the norms,” says Ashok Sethi, chief operating officer (COO) and executive director (ED), Tata Power.

Ashok Khurana, director general, Association of Power Producers (APP), agrees, “APP is fully geared up to meet the timelines for the implementation of the new environmental norms.” He adds a note of caution though the possibility of delays cannot be ruled out because of regulatory and financial issues.

Power Line takes a closer look at the country’s emission control market…

Market size and opportunities

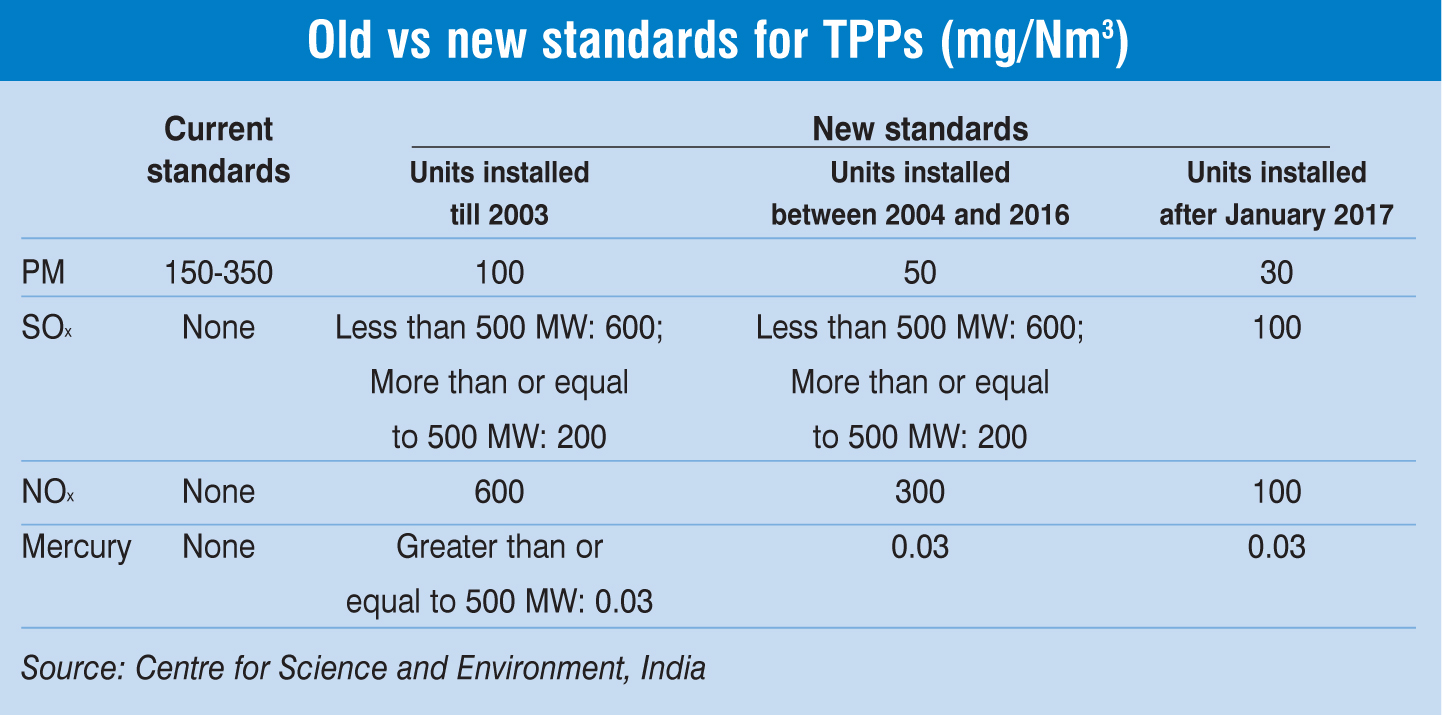

The revised norms have, for the first time, gone beyond PM norms to include SO2, nitrogen dioxide and mercury emission as well. Different techniques are available to control the emission of these pollutants.

FGDs

To meet the new pollution norms for SOx, the plants are required to retrofit or install FGD technology, which helps remove SO2 from exhaust flue gases of fossil-fuel power plants. “India used to claim that its coal was low sulphur and hence, FGD technology was not required. To meet the new norms, FGD will be required,” says a report by think tank Brookings Institution.

FGD is a mature technology globally for controlling SO2 emissions and has proved to be effective for a wide range of coal qualities and operating conditions. Some techniques for removing SO2 from flue gas include wet FGD, semi-dry, dry FGD, seawater FGD, circulating dry scrubber, and dry sorbent injection. The choice of FGD depends on various factors such as the scale of process, location of the project, sulphur content in the coal, and the availability and cost of reagents.

In India, industry observers say that seawater FGD installation will be more relevant for coastal plants. However, its use is likely to be limited given that there is less likelihood of more coastal plants coming up as the country reaches self-sufficiency in domestic coal.

Hence, wet limestone FGD process will find greater application in inland projects. Moreover, wet FGDs are proven for higher efficiency, lower operating costs and low auxiliary power consumption, leading to an overall lower lifecycle cost. Dry technologies will find their application in small-sized power plants, peak load boilers or industrial applications.

“We expect a market of 80-100 GW from existing plants and around 45 GW from under-construction plants over the next five to seven years for FGD,” says Roy. Of the 122 GW plants that have been identified by the CEA, he expects that 15-20 per cent would be phased out, since they are older than 20 years and would need significant increases in tariffs for FGD installation.

There are, however, some key concerns pertaining to FGD installation. One of these is the quality of gypsum as there is a tremendous demand for it, given the country’s building material requirements. Further, there are problems with the disposal of gypsum, which is even more difficult than disposing of fly ash due to the demand for already scarce land. Availability of high purity (85 per cent or more) limestone, a key raw material required for FGD, will also be a challenge.

The other big issue is with regard to space availability for FGD systems, which have significant space requirements. For power projects that were installed after 2005, there is a space provision for future installation of FGDs. For others, the technical feasibility has to be examined.

DeNOx systems

The primary emission control technology for NOx mitigation includes the installation of low NOx burners or the use of ultra-low nitrogen content fuels. Low NOx burners help reduce NOx levels by lowering the flame temperature. The secondary emission control technology used in power plants to control NOx emissions includes SNCR and SCR techniques.

In the case of projects commissioned before 2017, experts say that it would be possible to achieve the NOx emissions level through modifications in the boiler combustion system, and the installation of low NOx burners would suffice for compliance. However, there is some uncertainty about the level of modification needed for NOx reduction for Indian coal, which is high in ash content.

In new plants, a combination of both boiler modification and use of NOx abatement systems like SCR or SNCR may be needed. For new plants, SCR is being mandated by owners as part of boilers. “Capacity aggregating over 130 GW would require such boiler modification or installation of SCR/SNCR or both to reduce NOx to comply with the revised emission norms,” explains Joshi.

Electrostatic precipitators

Another segment that will be important for the emission control market will be ESPs for PM control. Most of the country’s power plants have already installed ESPs. However, concerns over efficacy and operational performance issues mean that newer systems could be required for existing projects.

According to a study by the think tank, Centre for Science and Environment, the units commissioned between 1990 and 2008 (with a total capacity of 43 GW) may need to upgrade their ESPs to meet the PM norms of 100 and 50 milligrams per normal cubic metre (mg per Nm3), depending on the commissioning date. In some cases, it may involve adding fields in series or parallel or increasing the height of the ESPs. For around 109 GW of units installed after 2008, which were required to meet the PM norms of 50 mg per Nm3, a basic performance revamp may suffice. Units in the pipeline should be able to meet the 30 mg per Nm3 PM standard with a combination of ESP and FGD. Meanwhile, mercury emissions from power plants could be controlled by the systems provided for NOx and SOx (SCR and FGD) along with ESPs.

Supplier readiness

Domestic equipment industry players emhpasise that the existing manufacturing capacity is not a constraint for FGD or SCR systems and with their technical tie-ups with global solution providers, they are fully geared up to meet the power sector’s requirements.

For instance, BHEL has a technological tie-up with Mitsubishi Hitachi Power Systems (MHPS), Japan, for the designing of both wet limestone-based and sea water-based FGD systems. BHEL has executed FGD system orders for the 500 MW Trombay and the 3×250 MW Bongaigaon units, while it is currently executing an order for NTPC’s 2×660 MW Maitree supercritical project in Bangladesh.

For SCR systems, BHEL set up a first-of-its-kind demo plant at Tiruchi, back in 2010, where a BHEL-manufactured catalyst has been successfully tested. Recently, the company signed a test protocol (memorandum of agreement) with NTPC Limited for carrying out a slip stream pilot test of the BHEL-developed SCR at the 500 MW Simhadri project (Stage I, Unit 1). BHEL has also already received orders for carrying out necessary changes including boiler modification from AP Genco for the 1×800 MW Vijayawada plant, Andhra Pradesh Power Development Company Limited’s 1×800 MW Krishnapatnam project, Tamil Nadu Generation and Distribution Corporation’s 1×800 MW North Chennai Stage III project and 2×660 MW Uppur project as well as NTPC-SAIL Power Company Limited’s 1×250 MW Rourkela project.

L&T has a technology collaboration with Chiyoda, Japan for FGD solutions. It claims that its CT-121 FGD solution is a unique technology that uses a highly efficient Jet Bubbling Reactor, while ensuring that the plant remains compact and easy to maintain. L&T’s SCR offerings are through its joint venture (JV) company, L&T-MHPS Boilers Private Limited.

Meanwhile, the equipment market is seeing an influx of new players. Recently, power producer Jindal Steel and Power Limited (JSPL) announced the signing of a technical cooperation agreement with German emission control systems major VPC GmbH. Under this alliance, manufacturing lines will be set up in JSPL’s existing facilities at Raipur and Punjipatra for emission control systems. JSPL aims to start manufacturing and commercial dispatch of “Made in India” emission control systems by December 2017.

Key issues and concerns

An area of concern for the equipment industry is the excessive technical requirements stipulated in the technical specifications, which have a serious price impact. Further, utilities often delay the release of tender documents or signing of contracts, which is compensated by shrinking the project execution time. This makes it difficult for vendors to execute projects within time schedules, often leading to a compromise in the quality of equipment installed or safety at the plant site.

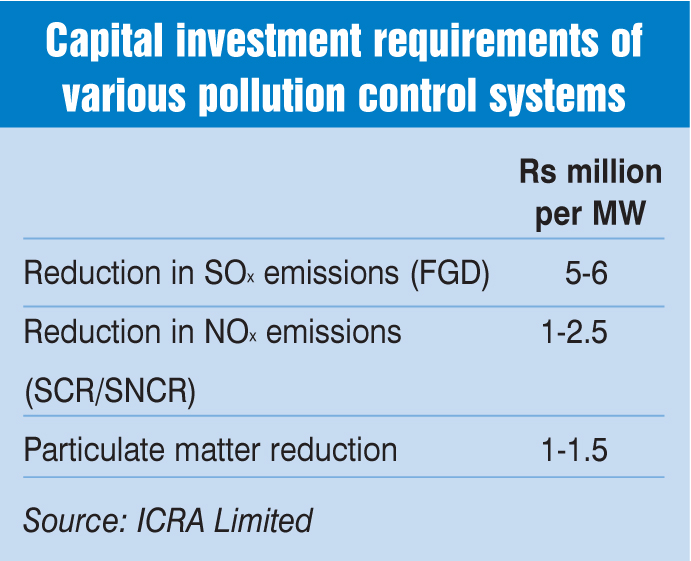

Meanwhile, on the developer side, a big concern that has been raised since the announcement of the norms has been with respect to costs. As per rating agency ICRA Limited, coal-based power projects will have to invest in additional equipment capital expenditure to comply with the revised emission norms. This expense could be in the range of

Rs 6 million to Rs 10 million per MW, based on the vintage of the plant. This aggregates a capex requirement of about Rs 1.2 trillion over the next two to three years, raising the generating cost of gencos by 13 paise to 22 paise per unit. Gencos face uncertainty on the recoverability of such costs from the financially fragile state-owned distribution utilities.

That said, power producers believe that costs could come down once market competition intensifies. “This is an opportunity for indigenous manufacturing and due to anticipated competition, we expect the costs to be optimum. As a utility, we would expect that the standardisation of specifications of different technologies by the government could further help in improving availability and optimising costs,” notes Sethi.

Another factor that would work in favour of bringing down costs, says Ravi Krishnan, MD, Krishnan & Associates, is the low price of emission control systems prevailing in the global market. “The world market for emission control technologies is quite weak currently, as many wind, solar and gas projects continue to dominate new power generation capacity growth. This means that there are at least 15-20 premier technology air quality control system providers offering services directly or indirectly through their JV partners in India. Costs have come down dramatically over the years.”

Industry recommendations

The challenges notwithstanding, the equipment industry is upbeat about the emerging opportunities. However, the industry stresses on the need for the central government to incentivise gencos to promote domestic competitive bidding for indigenous technology as well as manufacturing.

Stringent eligibility norms, so that only financially and technically capable vendors are engaged, are also part of the wish list of the equipment industry. Further, the promotion of emission control equipment under the Make in India initiative through tax incentives and extension of the “mega power policy” benefits to all FGD tenders is another key recommendation of the equipment industry.

Net, net, there is little doubt that the emission control market is set to take off in the next few years. Despite uncertainty over the effectiveness of the December 2017 deadline (news reports have indicated that the power ministry is coordinating with the environment ministry to consider an extension in order to avoid tariff shocks to end-consumers), the fact remains that India’s emission standards are only likely to get stricter in the next few years. India’s Intended Nationally Determined Contributions will ensure that the government walks the talk on its commitments. Focusing on a multi-stakeholder approach that addresses key concerns of appropriate recovery mechanisms for stressed IPP businesses will help ensure that the set targets are met sooner rather than later.