")

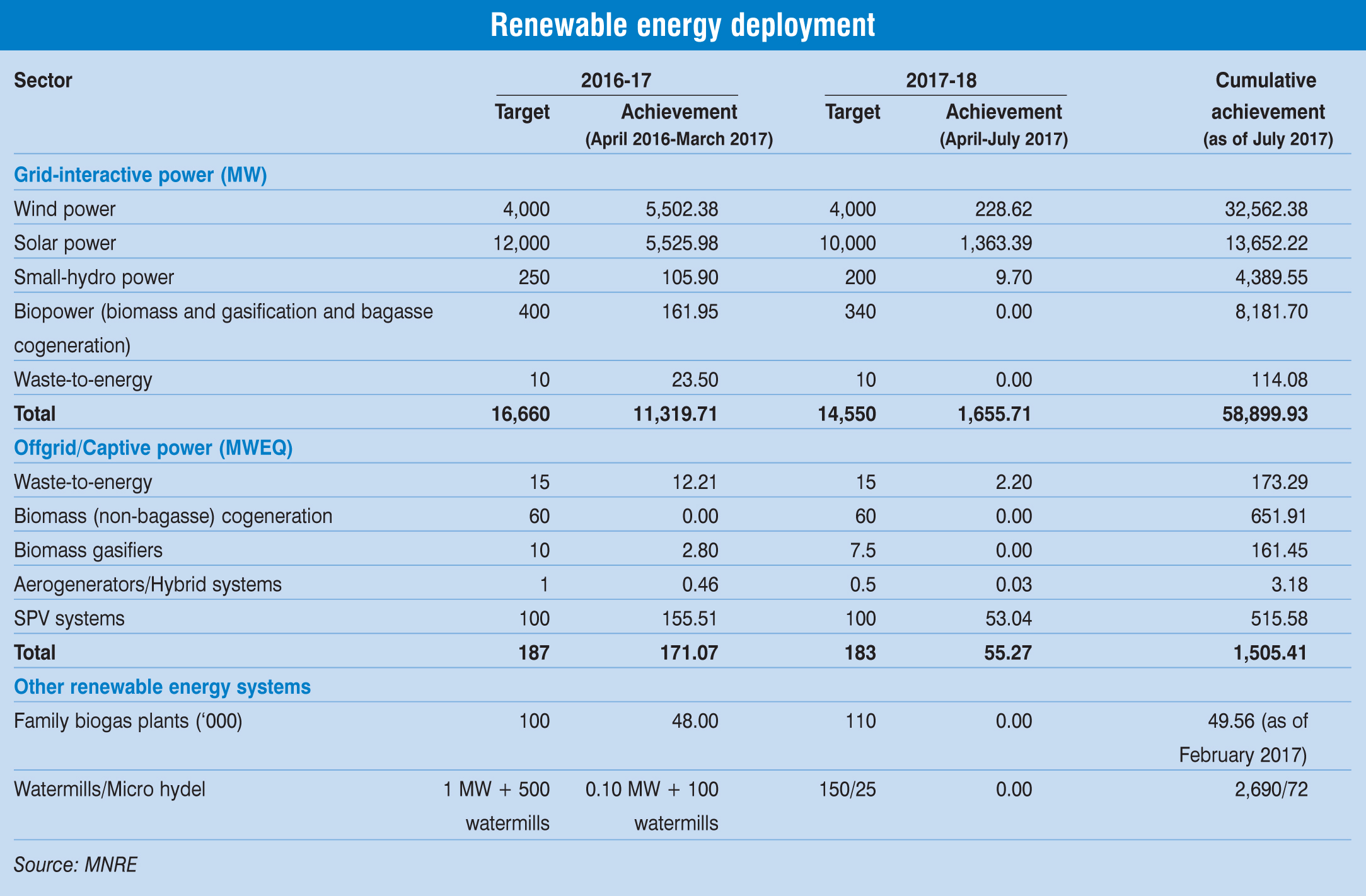

The renewable energy sector has grown significantly over the past year on the back of multiple regulatory changes, capacity additions and declining tariffs. As of July 2017, the total renewable energy capacity was 58.9 GW, surpassing that of hydropower which cumulatively stood at 44.6 GW. The share of renewable energy in the overall installed capacity also rose from about 14 per cent in March 2016 to 16 per cent in April 2017, and further to 17.8 per cent in July 2017. This rapid growth was enabled by the alignment of policies with the changing business environment. Moreover, the government’s constant pursuit to resolve the inherent restraining factors such as discom payments, grid connectivity challenges and power offtake issues have lowered the risks and improved investor interest in the sector, resulting in record capacity additions.

A total of 11.3 GW of capacity was added during the period April 2016 to March 2017. Of this, solar power accounted for 5,525.98 MW while wind accounted for 5,502.38 MW. Small-hydro power (SHP) added 105.9 MW, waste-to-energy installed capacity increased by 23.5 MW, and biopower added 161.95 MW to the capacity that cumulatively stood at 57,260.23 MW in March 2017.

The sector witnessed regulatory changes such as the move from feed-in tariffs (FiT) to the competitive bidding regime for allocation of projects and determination of tariffs for the wind power segment. While there was a sustained fall in capital cost, a rise in ease of doing business was noticed at both the state and central levels. These, along with other factors, have resulted in the steep fall in tariffs to Rs 2.44 per kWh and Rs 3.46 per kWh for the solar and wind power segments respectively. The decrease in tariffs has not only made renewable energy more affordable but also reduced offtaker risk.

Under competitive bidding, tariffs are market determined, which will help the sector move towards self-sustainability. To this end, the government has removed generation-based incentives (GBIs) and reduced the accelerated depreciation (AD) rates by half, from 80 per cent to 40 per cent, with effect from April 1, 2017.

In the wake of an expected influx of investments in the Indian renewable energy segment, new sources of financing are emerging such as green bonds, international financing and low-cost lending, making it easier for developers to raise capital. In the first seven months of 2017, India’s green bond issuance reached $2.1 billion.

Solar energy

The solar power segment in India has come of age in the past few years, driven by the government’s efforts of moving from conventional to alternative forms of energy for power generation. It has witnessed 67.2 per cent growth compounded annually since 2011-12. In 2016-17, the segment grew by about 81.7 per cent year on year over 2015-16. Most of the capacity was added in the last quarter of the year (January-March 2017) due to the rush to avail of AD benefits and GBI’s that were discontinued in April 2017. As of July 2017, the installed solar capacity was 13,652.22 MW, with an addition of only 1,363.39 MW from April to July 2017.

Solar photovoltaic project cost has witnessed a sharp decline of 46 per cent in the past five years. While the capital cost stood at Rs 98.7 million per MW in 2012-13, the Central Electricity Regulatory Commission (CERC) determined the cost at Rs 53 million per MW in 2016-17. However, with the capital cost becoming increasingly project and location specific and the sector’s complete shift to competitive bidding, the CERC has stopped providing a capital cost benchmark from 2017-18. Moreover, in the last 12 months, module prices have witnessed a decline of around 16 per cent. With the slowdown in Chinese demand and an oversupply situation in the near term, module prices could drop further, which is expected to result in further reduction in capital costs.

The solar power tariff hit the Rs 2.44 per kWh benchmark in the auction for 500 MW of capacity at Bhadla Solar Park Phase III in May 2017. The Rs 2.44 per kWh bid achieved on May 11, 2017 was 7 per cent lower than the previous low of Rs 2.62 per unit achieved on May 9, 2017, during the auction for 250 MW at Bhadla Solar Park Phase IV. There are two key factors that led to the decline in tariffs discovered in the consecutive tenders. The competition for new projects in the Indian solar power space is getting fiercer as the global solar equipment market is facing a glut, resulting in price erosion. Moreover, the domestic supply of new projects being tendered by the government is falling short of the demand from developers. Further, the entry of foreign firms and a number of domestic players with access to a large pool of low cost funds has enabled them to quote low bids in their attempts to win projects at the cost of their margins.

New guidelines for the tariff-based competitive bidding process for solar power plants were released by the Ministry of Power in August 2017. These are applicable to projects greater than 5 MW for supplying power directly or indirectly to discoms. A key highlight of the guidelines is the proposal to issue standard bid documents, power purchase agreements (PPAs) and other supporting documents. In addition, compensation for offtake constraints (50 per cent of the revenue loss due to backdown of a power plant will be met by the discom), termination compensation, lender substitution rights and a payment security mechanism have been introduced to safeguard developer interests and encourage more installations. With these guidelines in place, upcoming auctions are expected to be conducted in a more organised manner while issues such as curtailment due to lack of grid availability and the resultant backing down of must-run solar power plants are likely to be resolved sooner as the discoms stand to be heavily penalised.

Wind energy

The wind power sector added 5.4 GW of capacity during 2016-17, growing by 59 per cent over the previous year. This can be largely attributed to the withdrawal of GBIs and decline of AD benefits from 80 per cent to 40 per cent with effect from April 2017. In 2016, the government also decided to migrate to the reverse auction process of project allotment from 2017 onwards. This prompted developers to commission as much capacity as possible at the existing FiTs. As of July 2017, 32,562.38 MW of wind power capacity has been installed in the country, with only 228.62 MW added in the April-July 2017 period.

The success of the 1 GW wind capacity auction, which saw tariffs falling to Rs 3.46 per kWh, seems to be having a positive ripple effect, with all states looking to migrate from an FiT regime to competitive bidding for project allocation. The past two months have seen the launch of four new tenders for wind power capacity, including a 1 GW tender by the Solar Energy Corporation of India (SECI). At a time when the wind power sector is hit by inordinate delays in the signing of PPAs and late payments, and discoms are shying away from procuring power generated by wind projects, the transition to a competitive bidding regime has been received well across the value chain.

During the year, Andhra Pradesh added the highest wind power capacity, followed by Gujarat, Karnataka, Madhya Pradesh and Rajasthan. It added over 2 GW of capacity during the year, more than the average capacity added annually across the country until a few years ago. Siemens Gamesa and Suzlon were at the forefront of the capacity additions across the country, adding 2,050 MW and 1,783 MW respectively.

Other segments

The SHP segment continues to grow sluggishly due to increasingly unfavourable project economics and stiff competition from the solar and wind power segments. Against the target of 250 MW for the year, the segment added only 105.9 MW during 2016-17 to bring its total capacity to 4,379.85 MW as of March 2017. A meagre 9.7 MW was added in the April-July 2017 period. The biopower segment witnessed slow growth in the past year due to logistical and economic issues. The segment added 161.95 MW against the target of 400 MW during 2016-17, while as of July 2017, no capacity addition was reported.

Issues and challenges

While the solar and wind power segments continue to struggle with legacy issues such as lack of land availability and grid integration due to the intermittent nature of solar and wind energy, newer challenges have emerged in the sector over the past year.

With tariffs falling to Rs 3.46 per kWh, the risk of PPAs being dishonoured by discoms looms large over existing and upcoming wind and solar projects. The state discoms of Andhra Pradesh, in June 2017, approached the state’s power regulator, seeking a renegotiation of the PPAs that were signed in 2015. According to the PPAs, tariffs of Rs 4.76 per kWh would be applicable for 2018-19. The discoms have sought lowering of this tariff to the vicinity of tariffs recently discovered in the first 1,000 MW auction by SECI. Developers are of the opinion that the cancellation or renegotiation of PPAs would hurt the renewable energy sector as the risk associated with the project would increase significantly. Further, this could lead to a situation where discoms force high-tariff projects to back down generation.

Developer margins have been diminishing as a direct consequence of falling tariffs, posing another significant challenge for the sector. In a bid to win projects during auctions, developers often quote steep tariffs that have an adverse effect on the project profit margins and the rate of return on investment. This leads to waning of interest among small/ medium developers, ultimately resulting in mergers and acquisitions by domestic and international players with deep pockets and high inherent financial strength for absorbing low returns.

Outlook and the way forward

Low cost of capital, reduced capital costs as well as greater scale of installations have resulted in competitive tariffs for both the wind and solar power segments, leading to improved investor interest. Investments in the Indian renewable energy segment grew from about $7 billion in 2015-16 to nearly $14 billion in 2016-17. As of March 2017, about 14 GW of capacity was under construction and another 6 GW was in the pipeline to be auctioned during the year. Moving forward, the share of renewable energy in the country’s energy mix will increase as the government looks to improve grid integration. The government is actively looking at the role of energy storage to reduce the uncertainty associated with renewable energy sources. Moreover, wind-solar hybrids, offshore wind power development, and repowering of wind turbines are increasingly gaining traction in order to create a greener economy and meet the country’s climate change mitigation targets.