By Dr U.R. Prasad, Deputy Chief (Economics), Central Electricity Regulatory Commission

By Dr U.R. Prasad, Deputy Chief (Economics), Central Electricity Regulatory Commission

The Electricity Act, 2003, the National Electricity Policy, 2005 and the Tariff Policy, 2006 provide the structure and the principles to be followed for the determination of electricity tariffs. Despite considerable progress in the implementation of the Electricity Act and associated policies over the past decade, most distribution companies continue to post significant losses. One of the main reasons for the losses is the expense of providing below-cost power to key consumer groups such as agricultural and domestic consumers.

A look at the key trends in retail electricity prices in India during the period 2004-05 to 2015-16, and an analysis of the electricity prices for various consumer categories in India with reference to global tariffs…

Trends in retail electricity prices

As is evident from Fig. 1, there was an increasing trend in both the average cost of supply and average revenue during the period 2004-05 to 2015-16. The average cost of supply increased from Rs 2.54 per kWh to Rs 5.43 per kWh, whereas the average revenue increased from Rs 2.09 per kWh to Rs 4.23 per kWh. Meanwhile, the revenue gap – the difference between the average cost of supply and average revenue – increased from Re 0.45 per kWh to Rs 1.20 per kWh. It is also observed that the rate of increase in average revenue (7.42 per cent) was lower than the rate of increase in the average cost of supply (8.3 per cent); therefore, the revenue gap widened during the period. The revenue gap was generally met through government subsidy. As per Fig. 1, revenue as a percentage of cost was in the range of 82-86 per cent during 2004-05 to 2007-08; however, it was less than 80 per cent during 2008-09 to 2015-16. This indicates that the recovery of revenue was lower in the later period, which is not good for the health of distribution companies as they therefore need to rely more and more on subsidies from the government.

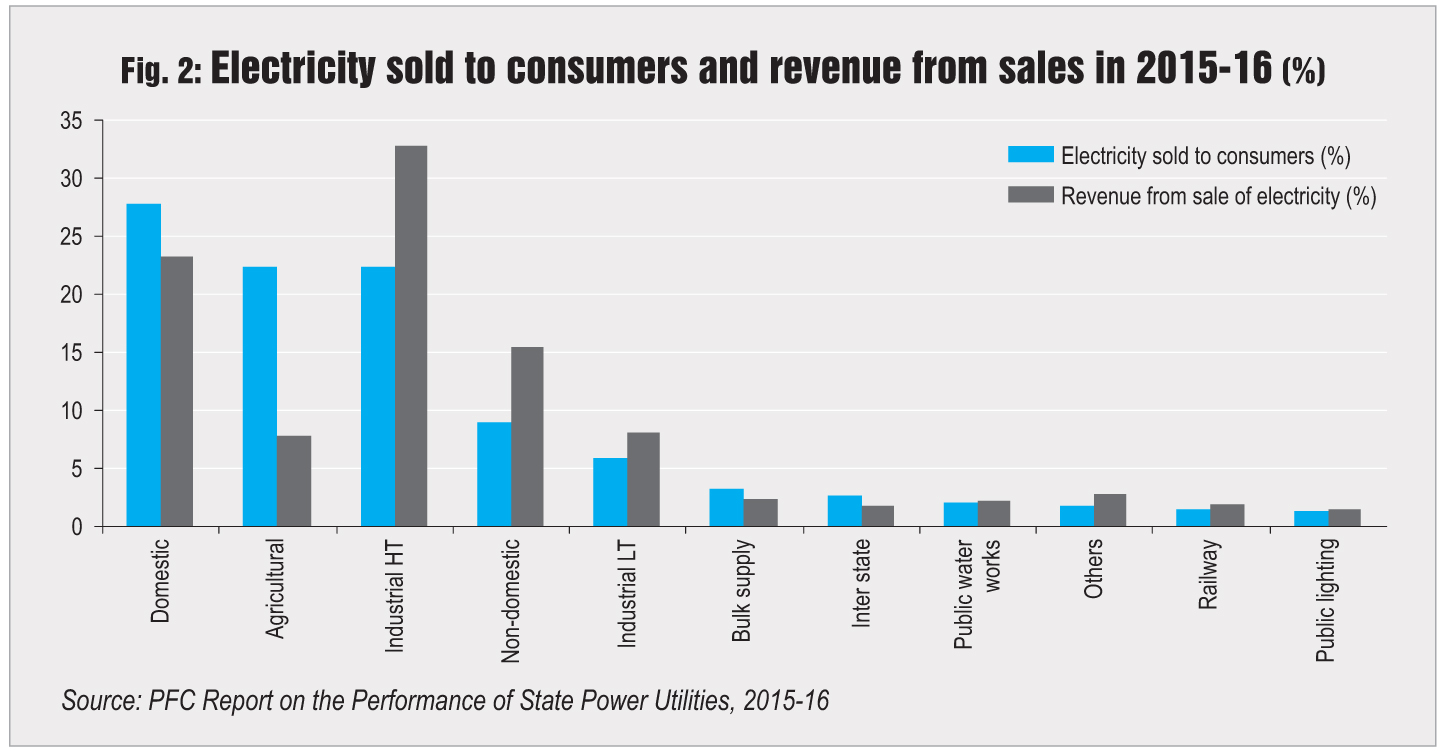

During 2015-16, 28 per cent of the electricity was sold to domestic consumers and 28 per cent to industrial consumers (22 per cent to high tension [HT] consumers and 6 per cent to low tension [LT] consumers). Revenue from the sale of electricity to industrial consumers was the highest at 41 per cent, of which 33 per cent was on account of industrial HT consumers and 8 per cent came from industrial LT consumers. During 2015-16, agricultural and domestic consumers together accounted for 50 per cent of the total electricity consumption. However, the revenue from these consumers was only 30 per cent of the total revenues. Meanwhile, industries (HT and LT) accounted for 28 per cent of the total consumption, whereas revenue from these consumers was 41 per cent. Commercial consumption was 9 per cent whereas the revenue from these consumers was 15 per cent.

Fig. 3 presents the trends in electricity prices for major consumer categories in India during 2004-05 to 2015-16. During this period, electricity prices for non-domestic (commercial) and industrial consumers (HT and LT) were above the average prices for all consumers, whereas the prices for domestic and agricultural consumers were below the average prices. Meanwhile, the rate of increase in prices for agricultural consumers (10.04 per cent) and domestic consumers (6.38 per cent) was higher than the average rate of increase in prices for all consumers (6.11 per cent), whereas the rate of increase in prices for industrial consumers (5.93 per cent for industrial LT) and non-domestic consumers (5.45 per cent) was lower than the average rate of increase. The rate of increase in prices for HT industrial consumers (6.28 per cent) was lower than the rate of increase in prices for agricultural and domestic consumers. Therefore, the rate of increase in prices for major consumer categories has been moving in the right direction.

During 2004-05 to 2015-16, electricity prices for various consumer categories varied inversely with the average cost of supply. The average cost of electricity supply for LT consumers is significantly higher than that for HT consumers. But the price charged to LT consumers is significantly lower than the price charged to HT consumers. In 2015-16, the average cost of electricity supply was Rs 4.96 per kWh, whereas the rate per unit of agricultural consumption was Rs 1.71, which implies a subsidy of Rs 3.25 for every unit of energy consumed by agricultural consumers. The low tariffs for agricultural consumers led to the misuse and wastage of electricity.

Domestic consumers have also been subsidised, although to a lesser extent. During the year, the rate per unit of domestic consumption was Rs 4.15, which implies a subsidy rate of 81 paise for every unit of energy consumed by domestic consumers. The heavy subsidisation of agricultural and domestic consumers has contributed to the high losses of the state distribution companies. To curtail these losses, industrial and commercial category electricity prices were much higher than the average cost of supply.

Global comparison

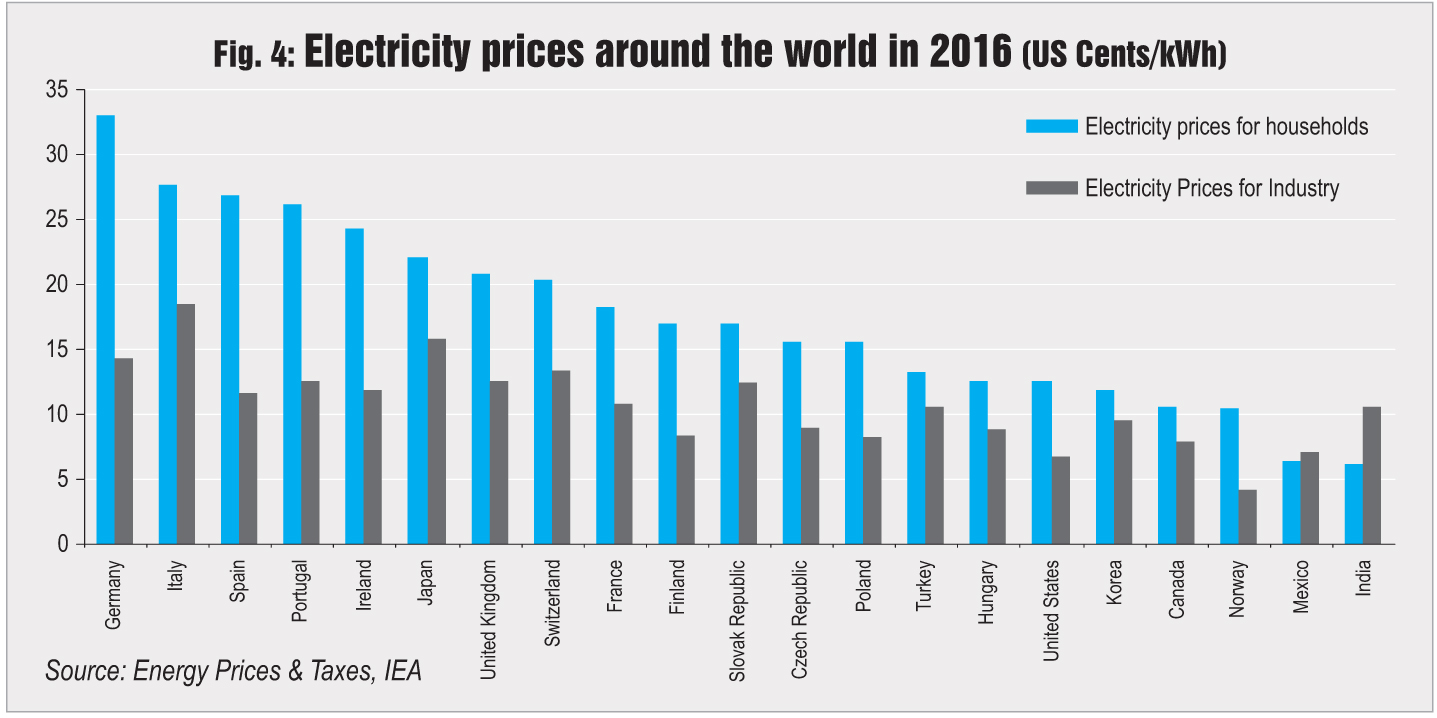

A comparison of electricity prices in India and in 20 other countries shows that retail electricity prices in India were the lowest in 2016. The electricity price for households in India was 6 US cents per kWh, which is three times lower than the average price in the other countries (18 cents per kWh).

In all countries except Mexico and India, electricity prices for household consumers were significantly higher than those for industrial consumers. In India, electricity prices for industrial consumers were equal to the average prices in other countries (11 cents per kWh). During the period 2005 to 2016, the rate of increase in electricity prices for households was 2.01 per cent in India, which was lower than the average rate of increase in the 20 countries (2.32 per cent). The rate of increase in electricity prices for industry in India (1.86 per cent) was also lower than the average rate of increase in all the 20 countries (2.33 per cent), which is a key positive.

Conclusion

It has been more than a decade now since the mandates of the Electricity Act, 2003 and associated policies have been in place. However, there is still no visible change in electricity prices in the direction that is required. The prices charged to various consumer categories vary inversely with the average cost of supply. The main reason for this uneconomical pricing has been that the tariffs for a particular category of consumers are determined based on social and political considerations rather than economic and efficiency considerations. A cost-reflective tariff structure needs to be adopted in India. The issue of access to electricity for people below the poverty line must be addressed through instruments of social policy, not by electricity pricing. If cross-subsidy is removed, Indian manufacturing can become more cost competitive with respect to global players, which can help bring more industries under the Make in India initiative.