While coal continues to remain the mainstay of power generation in the country, liquid fuels account for a small yet significant proportion of the power generated. Amongst these, diesel is the most preferred option owing to its high energy density and relative ease of availability. Diesel generator (DG) sets continue to dominate the backup power solutions market due to their fuel efficiency and lower capex. However, the fuel costs are relatively high in this case. Although DG sets in the country are run primarily on high speed diesel (HSD), a range of other fuels can also be used for the purpose. These include light diesel oil (LDO), low sulphur heavy stock (LSHS) and furnace oil (FO).

Demand dynamics

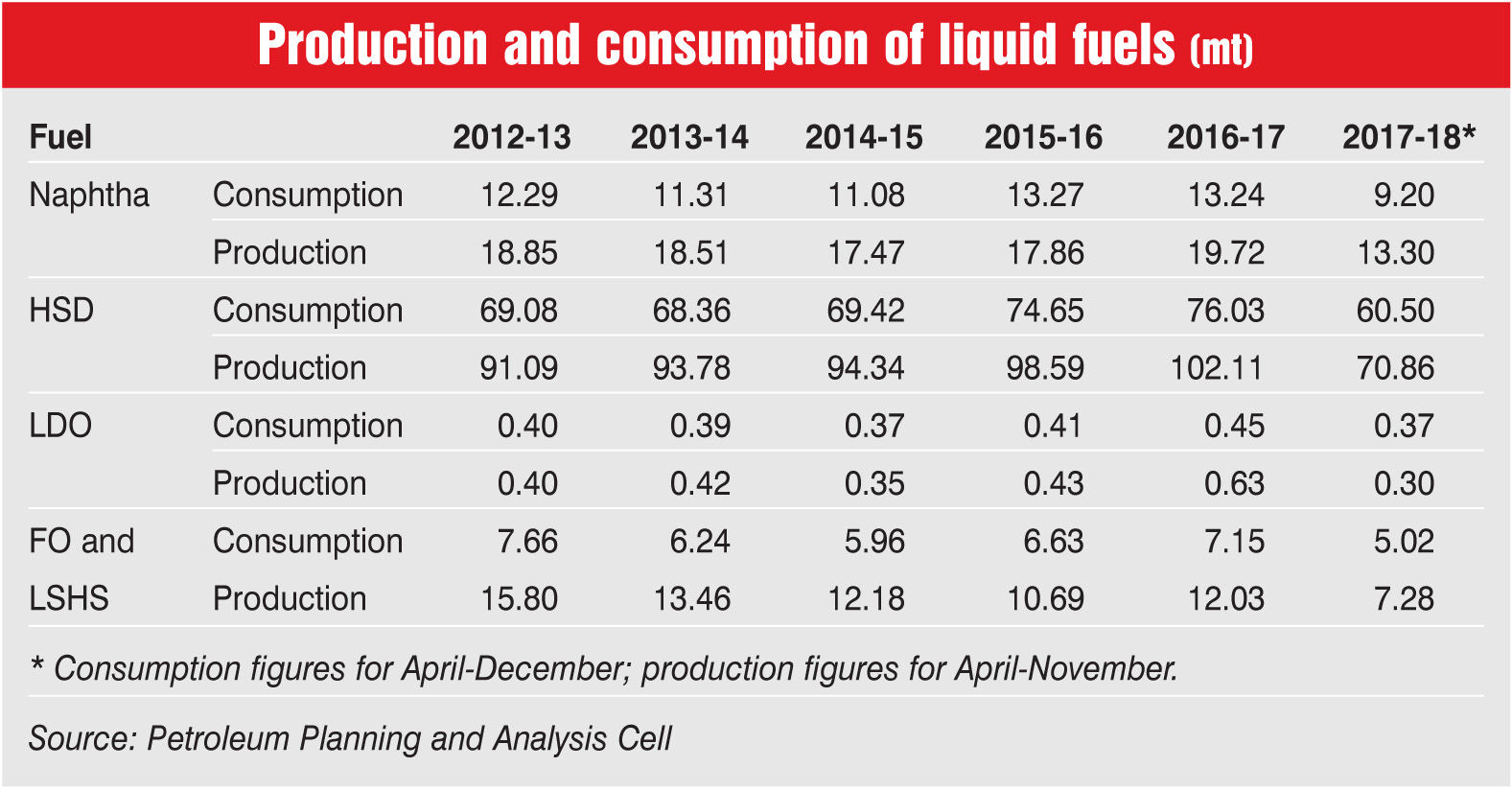

As per the Petroleum Planning and Analysis Cell, HSD consumption has displayed an upward trajectory with a compound annual growth rate (CAGR) of 2.42 per cent between 2012-13 and 2016-17. HSD consumption increased from 69.08 million tonnes (mt) in 2012-13 to 76.03 mt in 2016-17. Meanwhile, LDO consumption grew at a CAGR of 2.93 per cent to reach 0.45 mt in 2016-17. The primary use of LDO in the industry is for fuelling the boilers in power plants. Thus, it has relatively low demand compared to HSD, which is also used by the automotive sector. Naphtha is another important fuel because it serves as an alternative to liquefied natural gas in gas-based power plants. The consumption pattern of naphtha has been relatively asymmetric. In 2012-13, the country consumed 12.29 mt of naphtha, which declined to 11.08 mt by the end of 2014-15. In 2015-16, there was a 19.76 per cent increase in the consumption of the fuel, taking it to 13.27 mt. Subsequently in 2016-17, the figure stood at 13.24 mt. The consumption of FO and LSHS stood at 7.15 mt as of March 2017.

During the period April-December 2017, HSD consumption recorded significant variability on a month-on-month basis. Consumption stood at 6.97 mt in April 2017 and dropped to 5.92 mt in August 2017. Demand recovered somewhat in September 2017 and by December, the aggregate consumption stood at 60.5 mt. LDO consumption levels continued to be the lowest, with 0.37 mt being consumed till December 2017. Meanwhile, naphtha, and FO and LSHS recorded consumption levels of 9.2 mt and 5.02 mt respectively.

Production levels

Production levels

The production trends of these fuels have been in tandem with the consumption patterns. HSD production has been surging, growing at a CAGR of 2.9 per cent, from 91.09 mt in 2012-13 to 102.11 mt in 2016-17. All other fuels have followed alternating trends, with occasional peaks and troughs in production quantities. Naphtha production grew at a CAGR of 1.14 per cent to reach 19.72 mt in 2016-17.

LDO production recorded the highest CAGR of 12.01 per cent, increasing from 0.4 mt in 2012-13 to 0.63 mt in 2016-17. An interesting insight provided by the data is that the LDO consumption-production gap has been negligible as compared to other fuels. While HSD and naphtha have been consistently overproduced, LDO has managed to maintain demand-supply parity. The production of LSHS has witnessed a decline of 78.94 per cent, from 1.29 mt in 2012-13 to 0.27 mt in 2016-17. Another clear inference is that all the fuels suffered a slowdown between 2012 and 2014. This was primarily on account of the weak macroeconomic scenario in the country.

During April-November 2017, India produced 13.3 mt of naphtha and 70.86 mt of HSD. FO and LSHS production stood at 7.28 mt, whereas LDO production was 0.3 mt. Overall, crude oil production has been surging. It increased by 12.11 per cent, from 218.85 mt in 2012-13 to 245.36 mt in 2016-17.

Future outlook

In the backdrop of a new tax regime and the demonetisation drive, economic activity in the country is recovering gradually from the regulation-induced slowdown. As per the US Energy Information Administration, India and China are expected to be the largest contributors to the growth in the consumption of petroleum and other liquid fuels in 2018 and 2019. India is expected to experience stronger growth in 2018 and 2019, with a consumption growth forecast of about 0.3 million barrels per day, each year.